Quite a few mixed economic indicators right now:

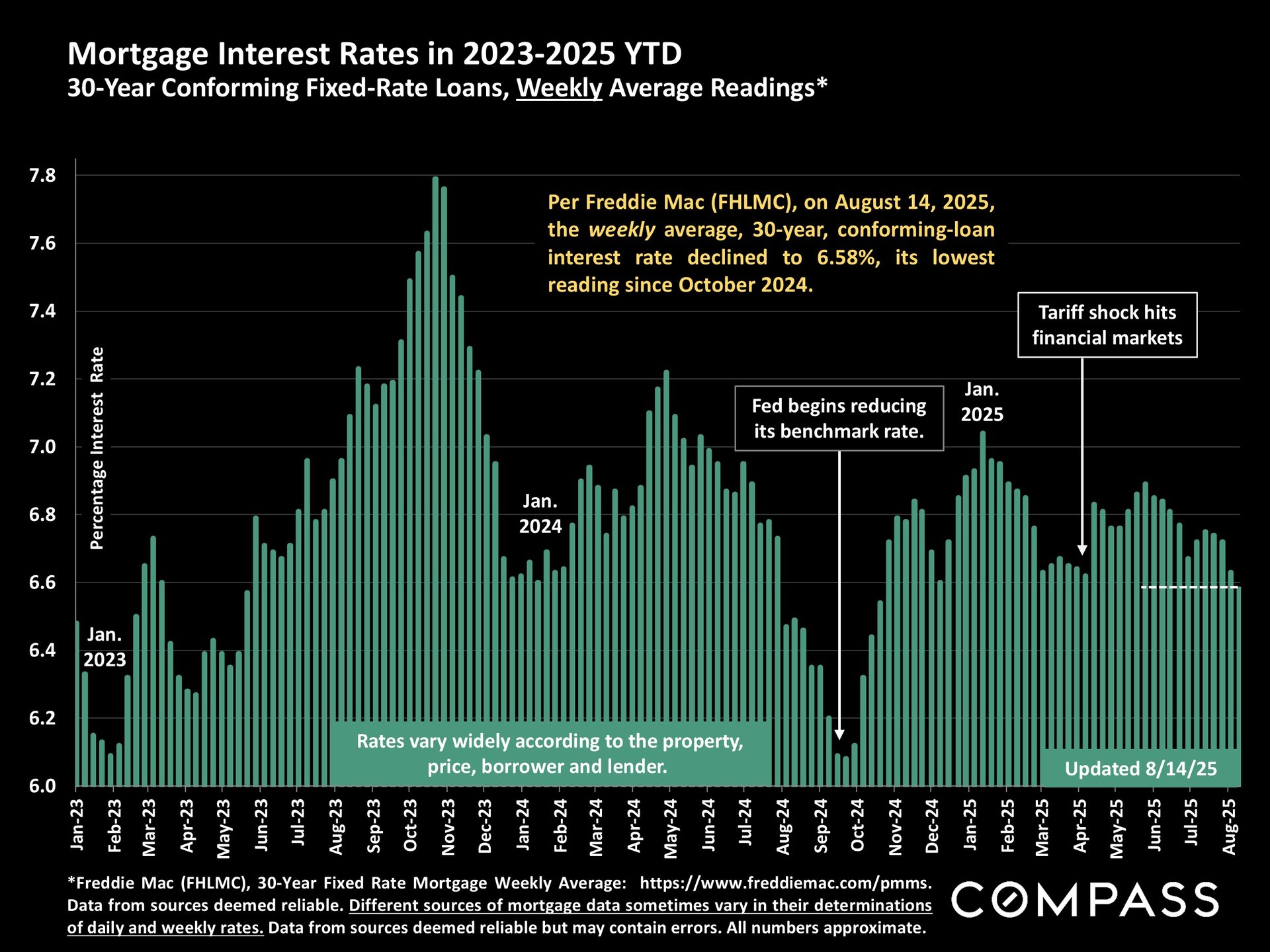

Interest rates hit their lowest point since last October. Many are singing, "happy days are here again," as has occurred many times (prematurely) over the past 3 years, but, as our chief economist, Mike Simonsen, has said, rates will probably need to get down closer to 6% to cause a significant boost in buyer demand - and perhaps that's where they are heading. But the picture regarding the course of inflation, as noted further down, remains deeply uncertain. I haven't seen anyone consistently and correctly predict interest rate changes in many years.

This analysis and data were compiled by our friend Patrick Carlisle at Compass.

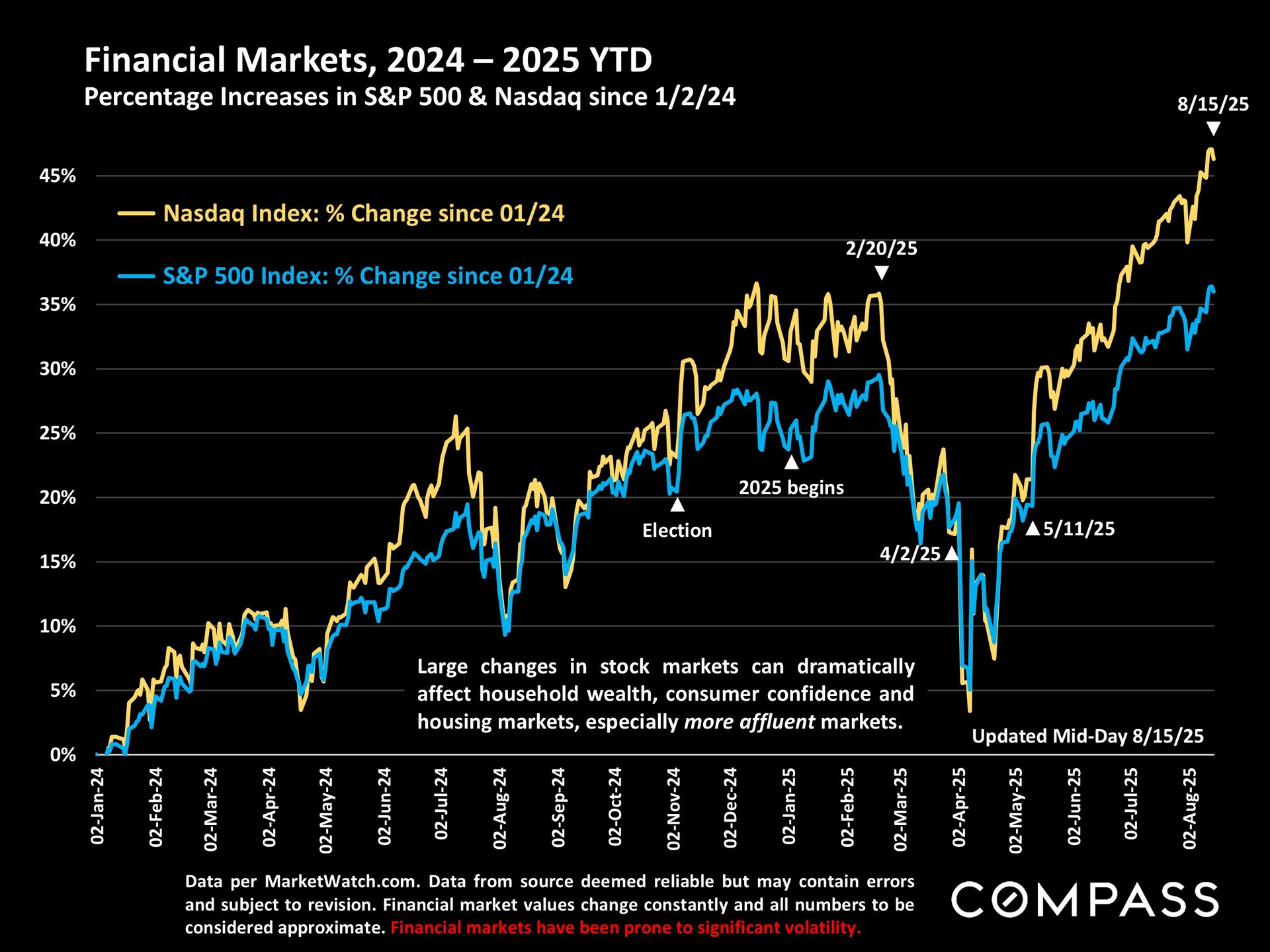

Stock markets continue to hit new highs: Generally speaking, bad news - such as the last miserable jobs report - is often considered good news by investors, because it might motivate the Fed to reduce rates, and any good news adds to optimism.

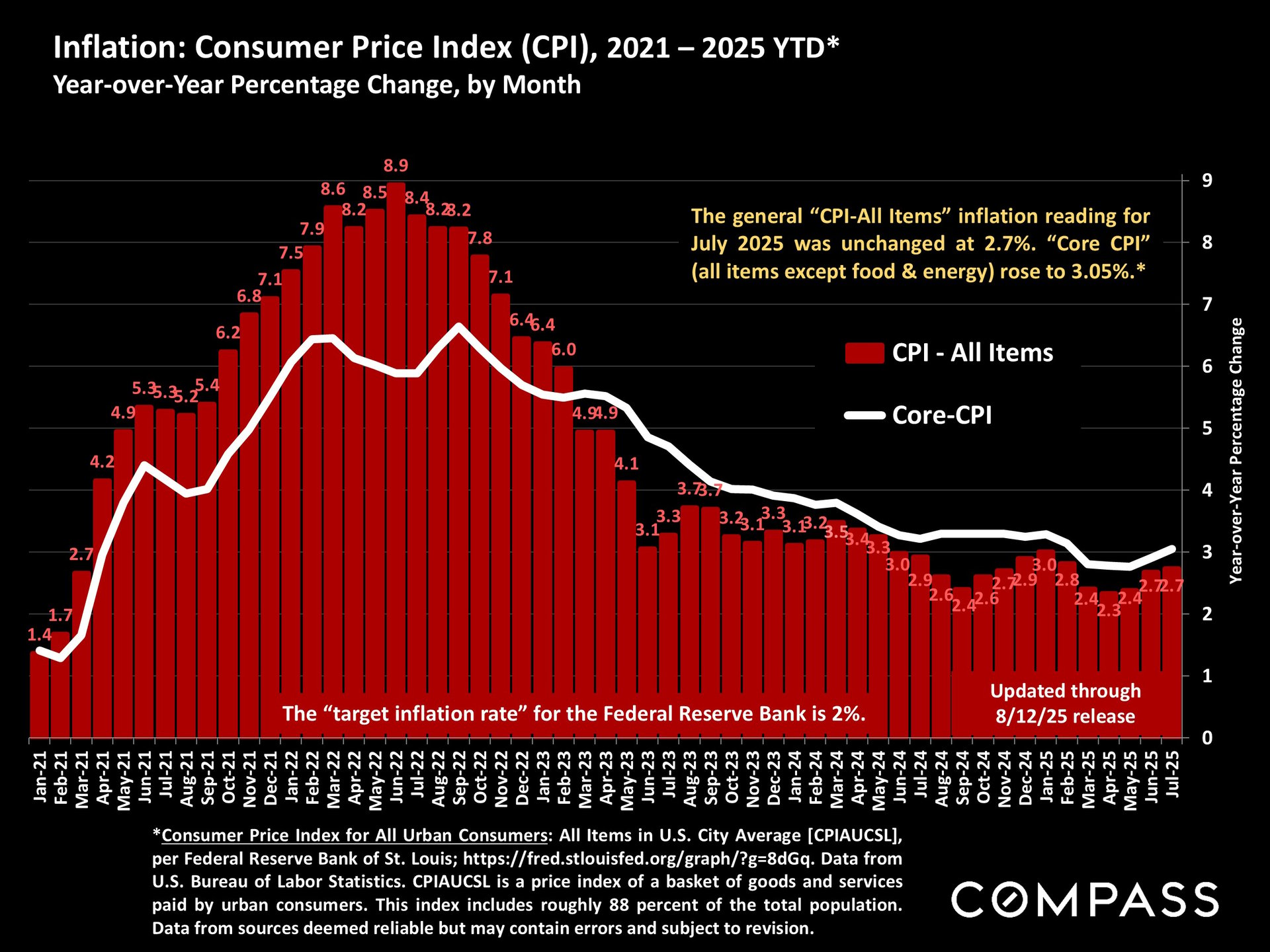

CPI inflation, all items, was essentially unchanged in the 8/12/25 release, but Core-CPI rose. And, in the "producer price index" report published yesterday, wholesale prices in July saw their largest monthly increase in over 3 years, which complicates the issue regarding the course of inflation and possible effects on the Fed and interest rates.

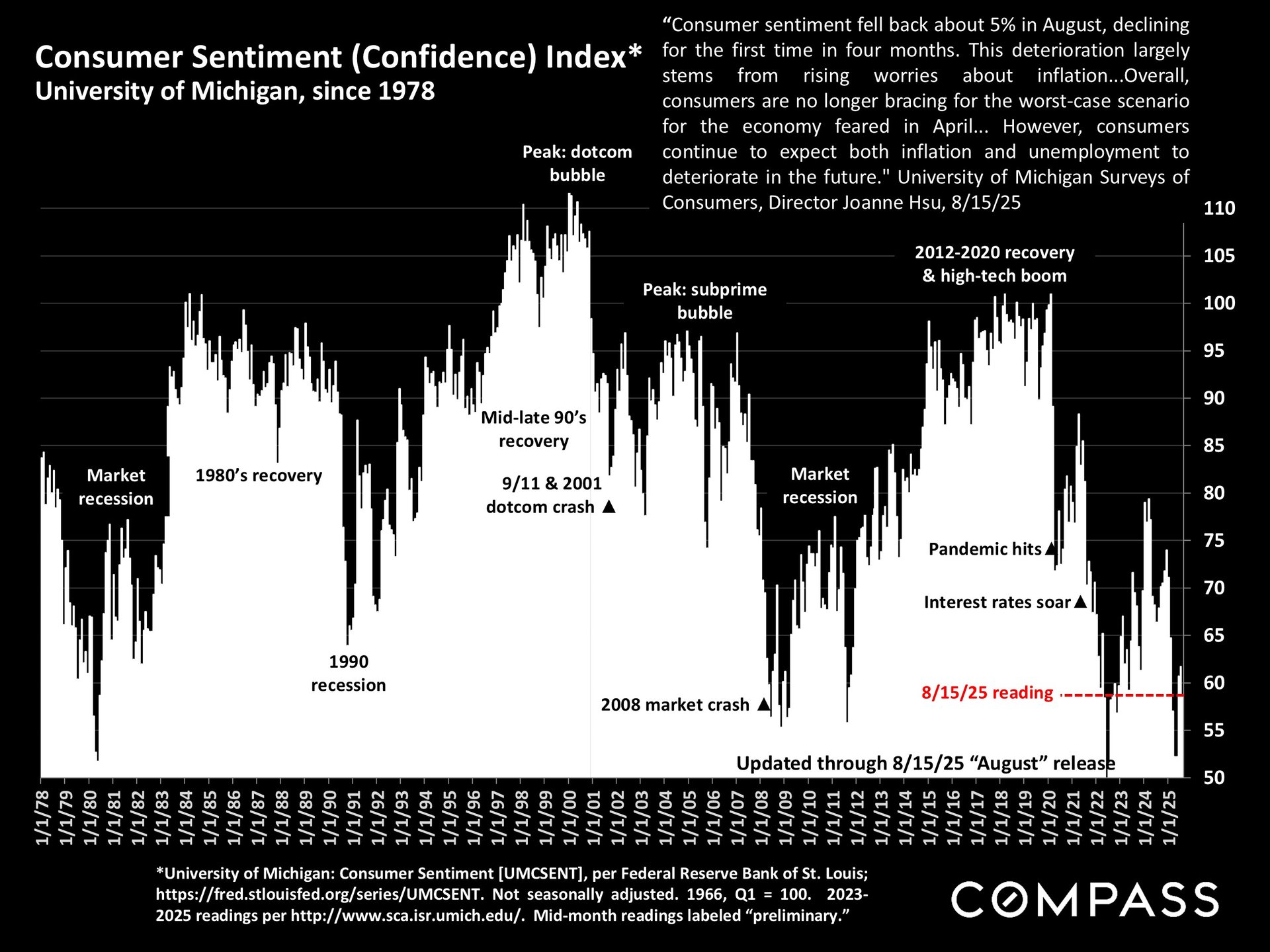

Consumer Confidence (Sentiment) in the preliminary August report released this morning declined. Generally speaking, the average consumer isn't buying into the heady optimism seen in stock markets: "Consumer sentiment fell back about 5% in August, declining for the first time in four months. This deterioration largely stems from rising worries about inflation...Overall, consumers are no longer bracing for the worst-case scenario for the economy feared in April when reciprocal tariffs were announced and then paused. However, consumers continue to expect both inflation and unemployment to deteriorate in the future...Year-ahead inflation expectations rose from 4.5% last month to 4.9% this month." University of Michigan Surveys of Consumers, 8/15/25

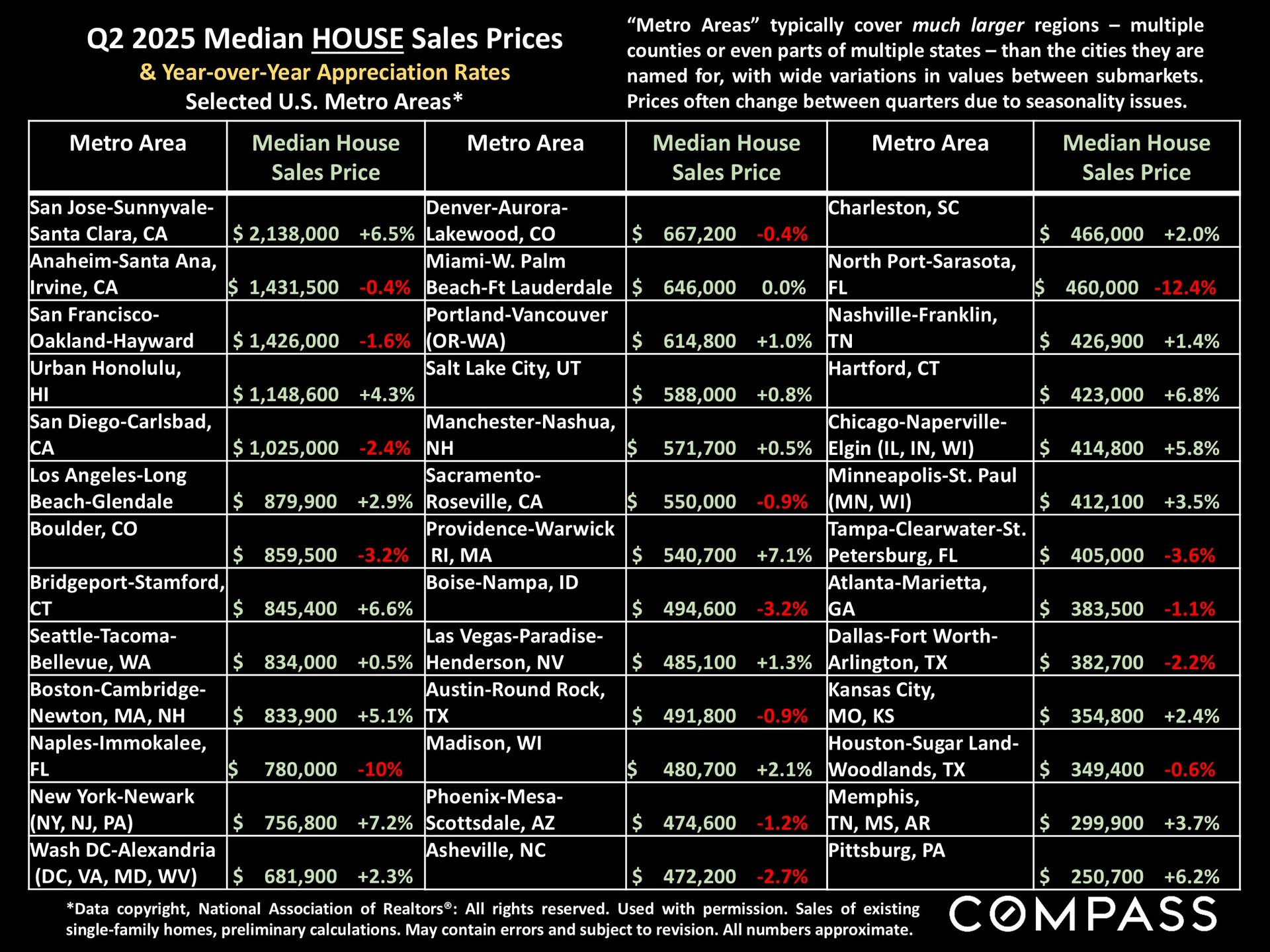

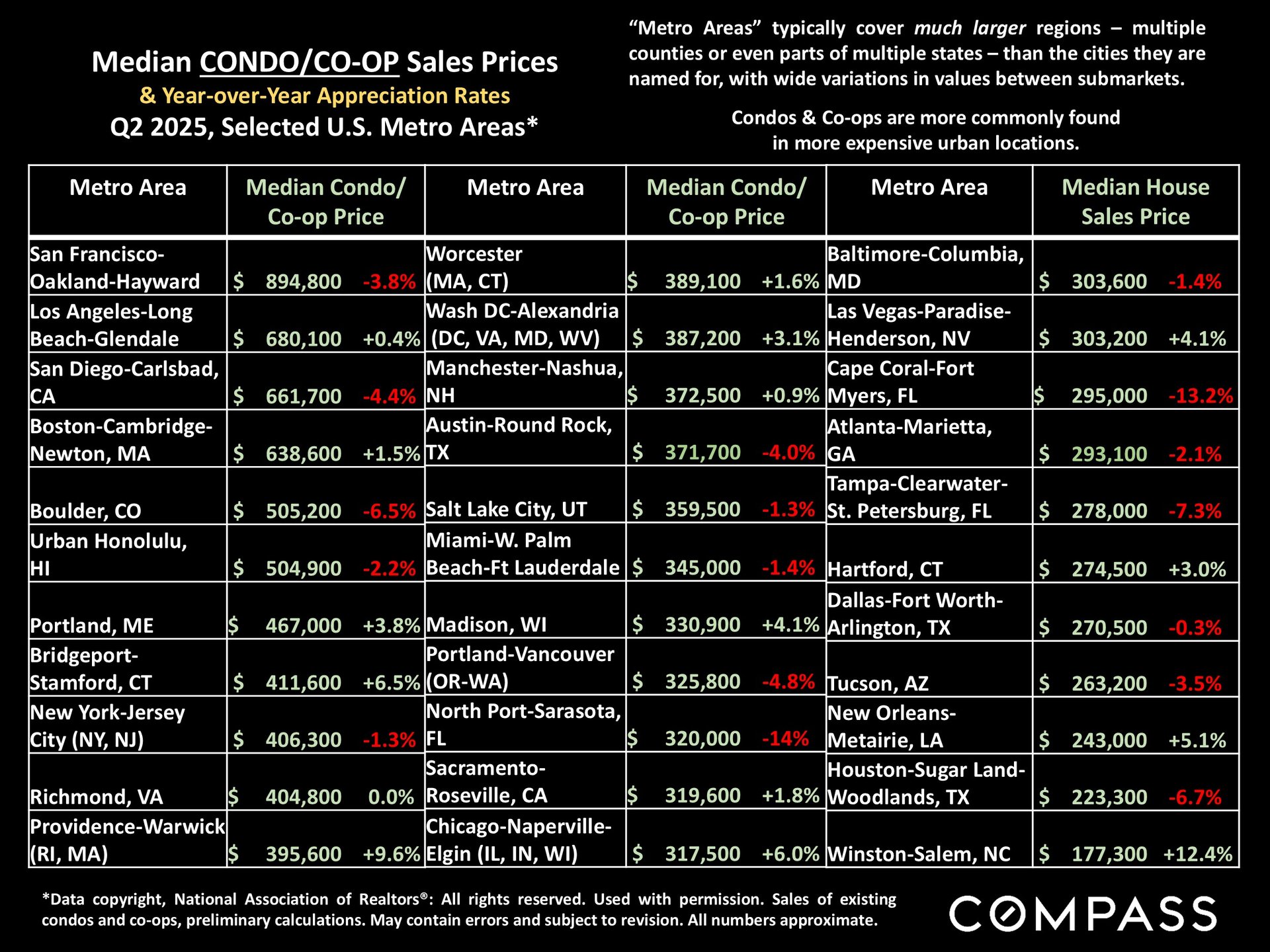

NAR just published its quarterly "metro-area" median sales price reports. Note that metro areas are typically large regions covering multiple counties and sometimes part of multiple states, so these are very broad statistics. As has been mentioned in many recent reports, some previously super-hot markets - such as in Florida, Texas, AZ, CO, ID and GA - are now seeing year-over-year declines in median sales prices, though results can vary between different markets within the same state (as in CA). The Northeast - with very low rates of new home construction - continues to see particularly strong appreciation rates.

Consumer Confidence (Sentiment) in the preliminary August report released this morning declined. Generally speaking, the average consumer isn't buying into the heady optimism seen in stock markets: "Consumer sentiment fell back about 5% in August, declining for the first time in four months. This deterioration largely stems from rising worries about inflation...Overall, consumers are no longer bracing for the worst-case scenario for the economy feared in April when reciprocal tariffs were announced and then paused. However, consumers continue to expect both inflation and unemployment to deteriorate in the future...Year-ahead inflation expectations rose from 4.5% last month to 4.9% this month." University of Michigan Surveys of Consumers, 8/15/25

NAR just published its quarterly "metro-area" median sales price reports. Note that metro areas are typically large regions covering multiple counties and sometimes part of multiple states, so these are very broad statistics. As has been mentioned in many recent reports, some previously super-hot markets - such as in Florida, Texas, AZ, CO, ID and GA - are now seeing year-over-year declines in median sales prices, though results can vary between different markets within the same state (as in CA). The Northeast - with very low rates of new home construction - continues to see particularly strong appreciation rates.

The Census just published an infographic comparing homeowner/renter demographic changes over 50 years, 2023 vs. 1973, which can be found here.

Don't forget to watch Mike Simonsen's latest Compass Intelligence report.