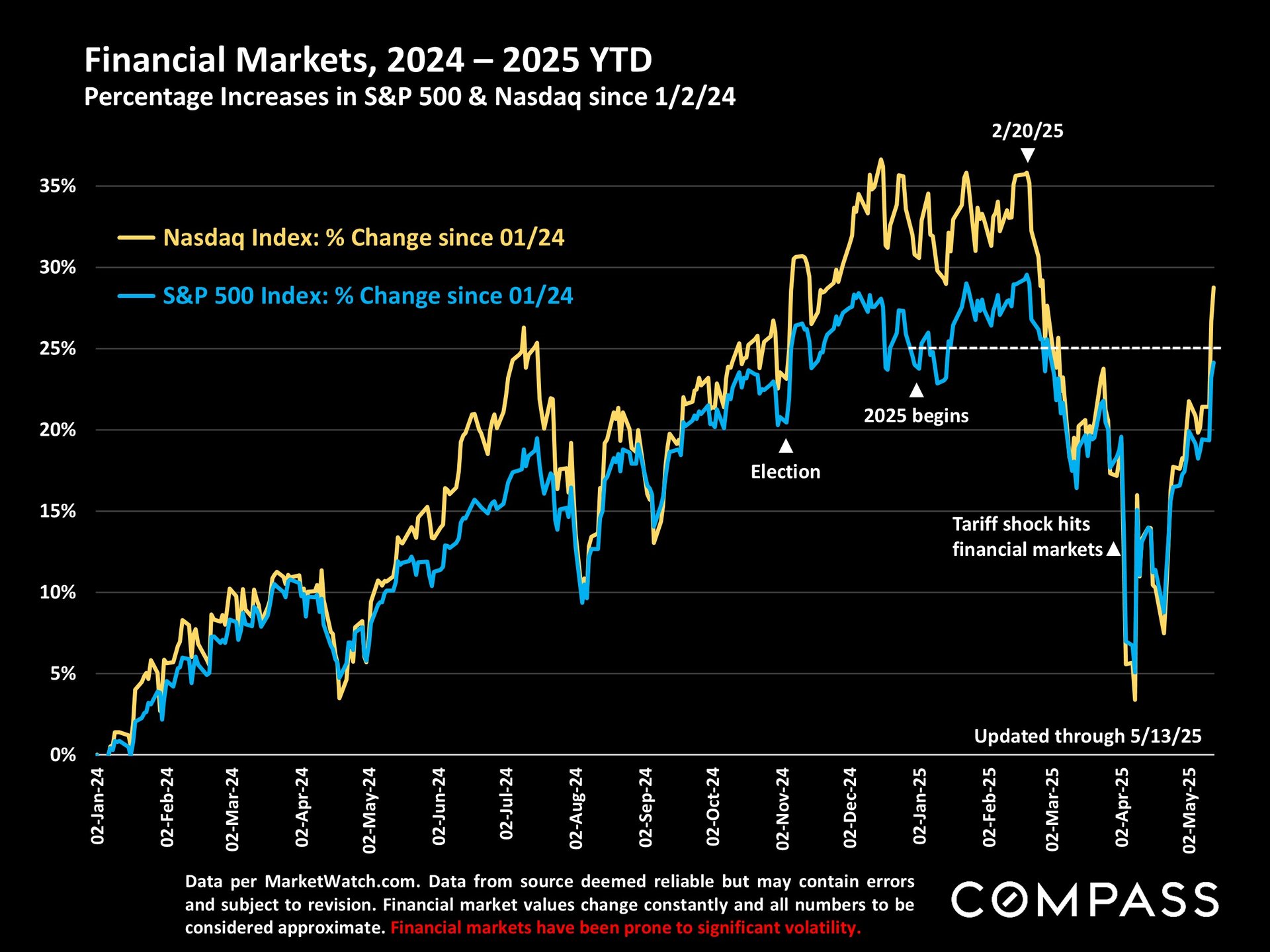

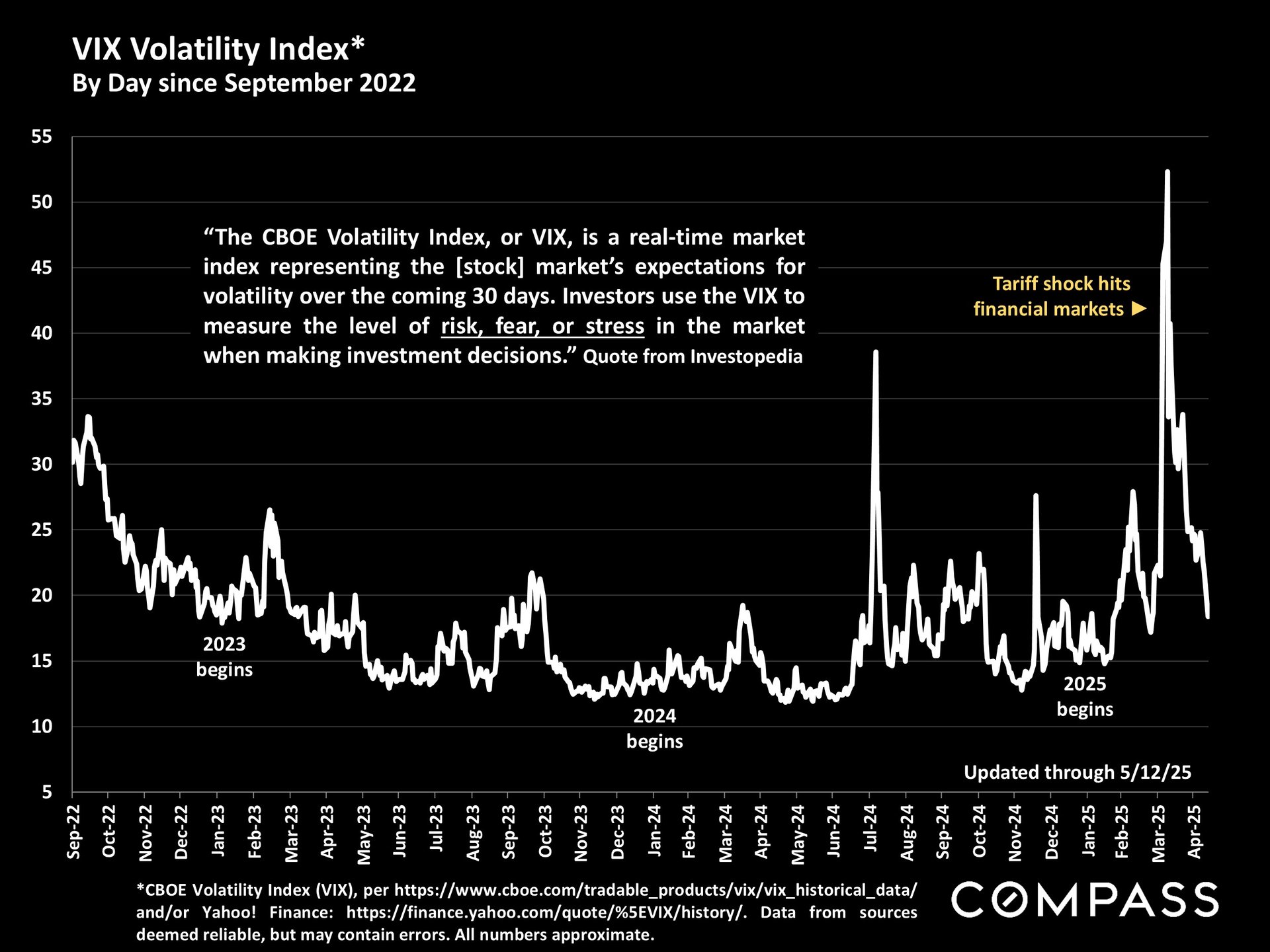

Stock markets have seen a spectacular recovery from the crash of early April. We'll have to see how this affects buyer and seller confidence regarding moving forward with life plans pertaining to housing. Clearly, some buyers and sellers were not affected by April's volatility in the first place, but some consumers may remain a bit shell-shocked as they try to make sense of recent events - until it seems more definite that the recent political/economic chaos has subsided for the longer term.

This analysis and data were compiled by our friend Patrick Carlisle at Compass.

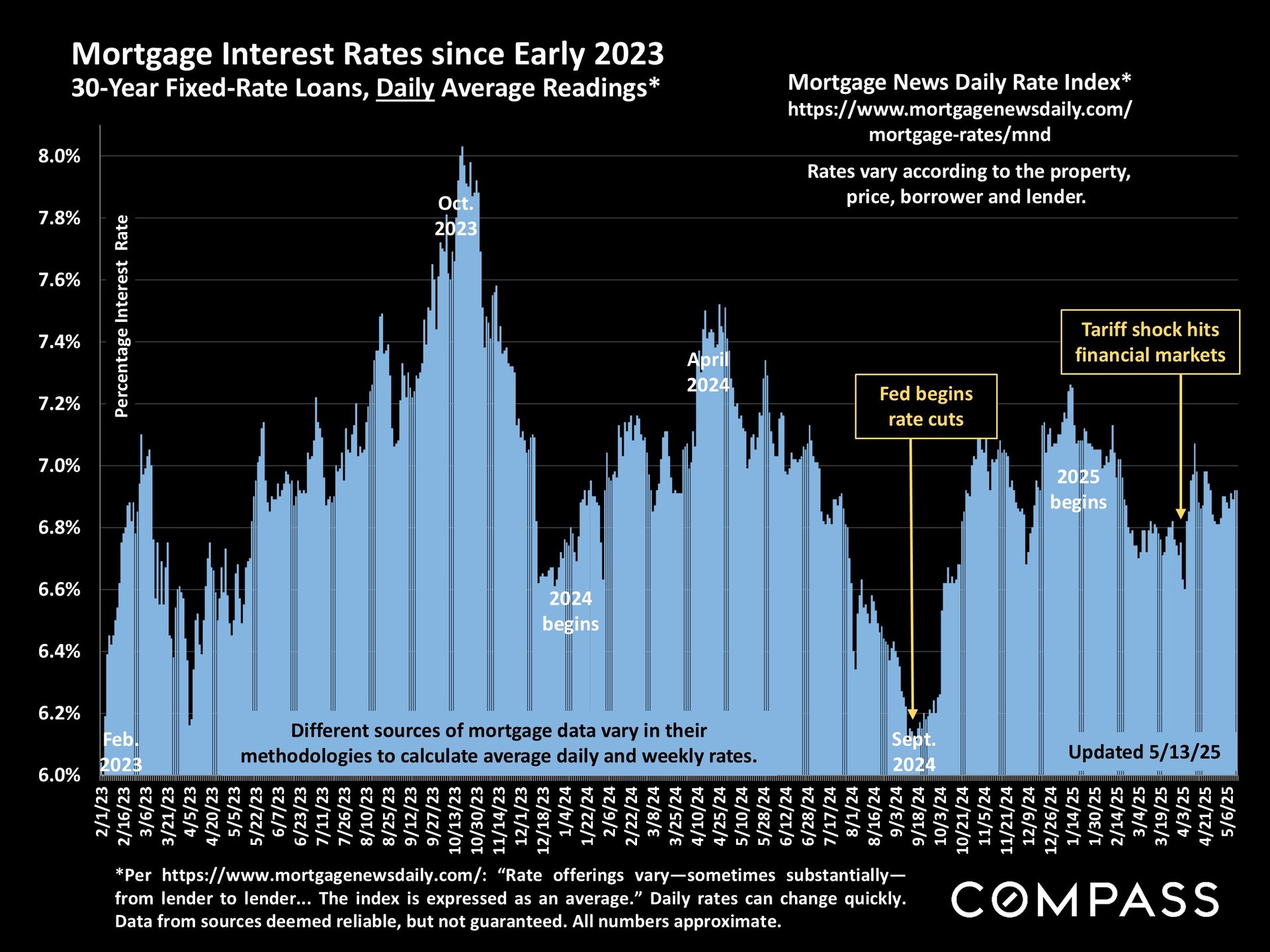

Interest rates have remained relatively high, at relatively close to 7%.

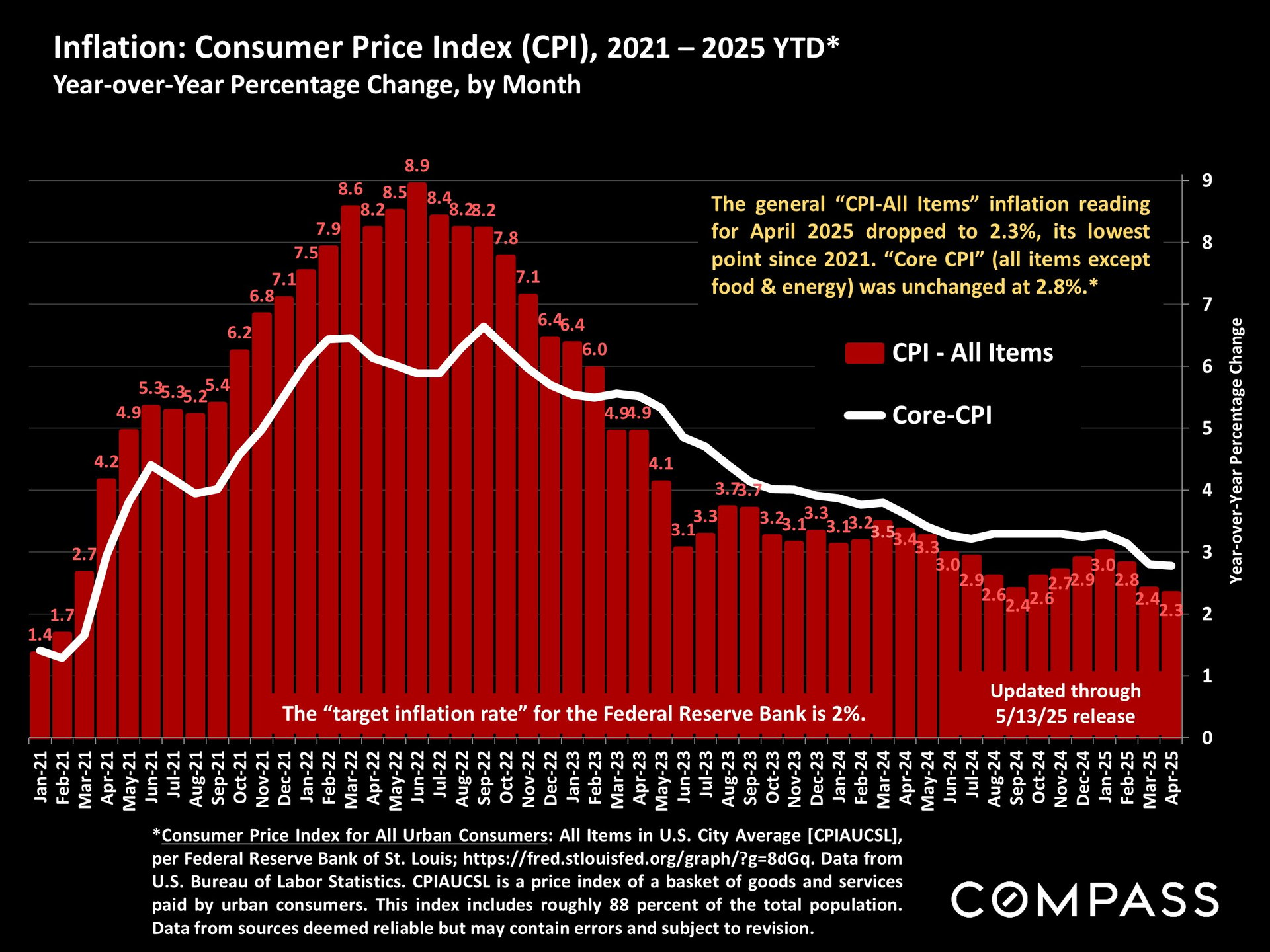

The April inflation reading came in at 2.3%, its lowest since 2021. ("Core" inflation remained unchanged at 2.8%.) It's uncertain how the ever-changing tariff situation may affect inflation going forward.

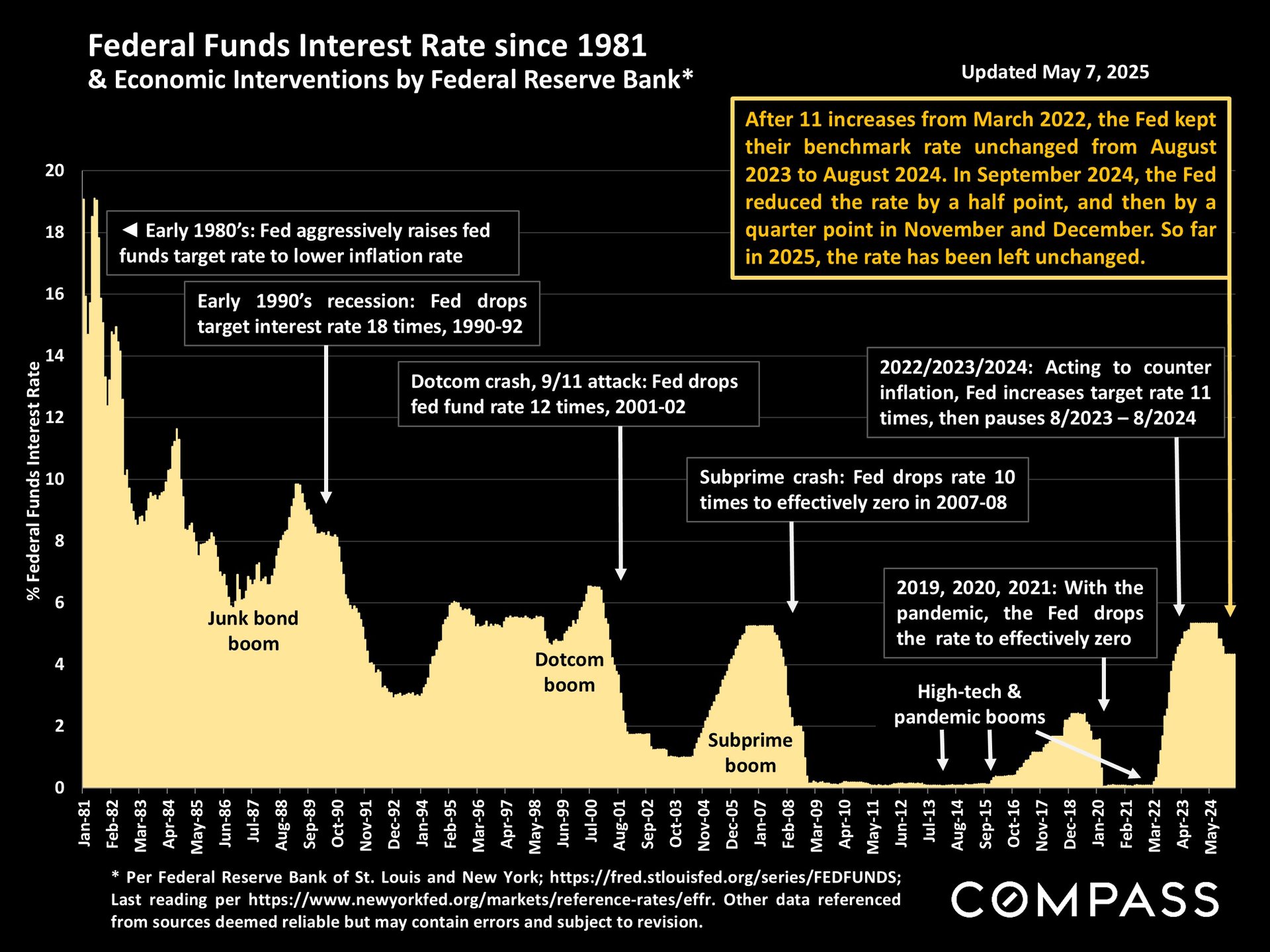

The Fed left its benchmark rate unchanged at its latest meeting on May 7th.

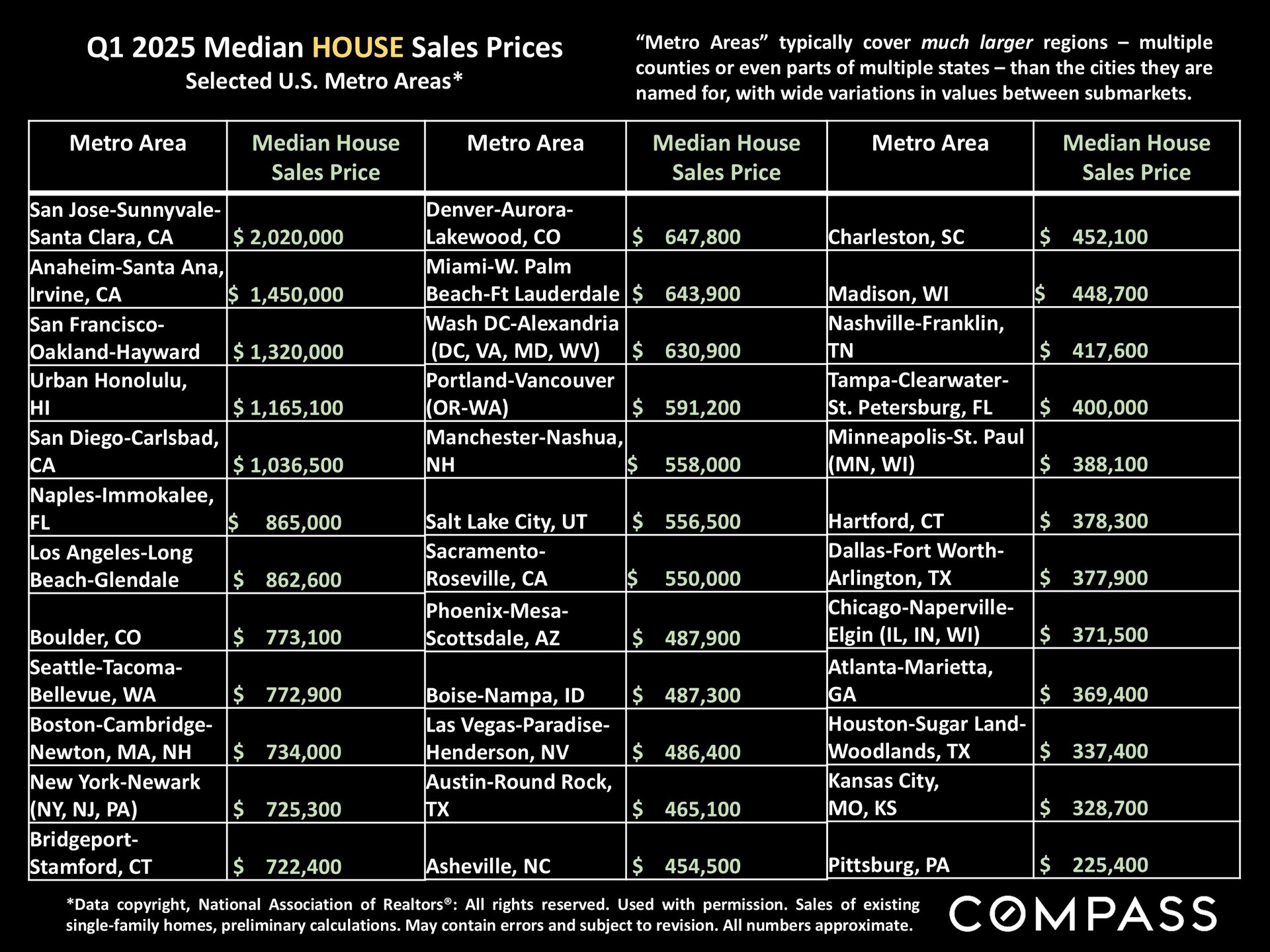

A comparison of median existing-house sales prices for selected major metro areas in Q1 2025. Note that metro areas are typically multi-county regions designated by the federal government: For example, the San Francisco "metro area" includes 4 other nearby counties with a wide range of home values. The Santa Clara metro area - with by far the highest median house price in the country - consists of Santa Clara and San Benito Counties (totally dominated by the enormously greater market of Santa Clara).

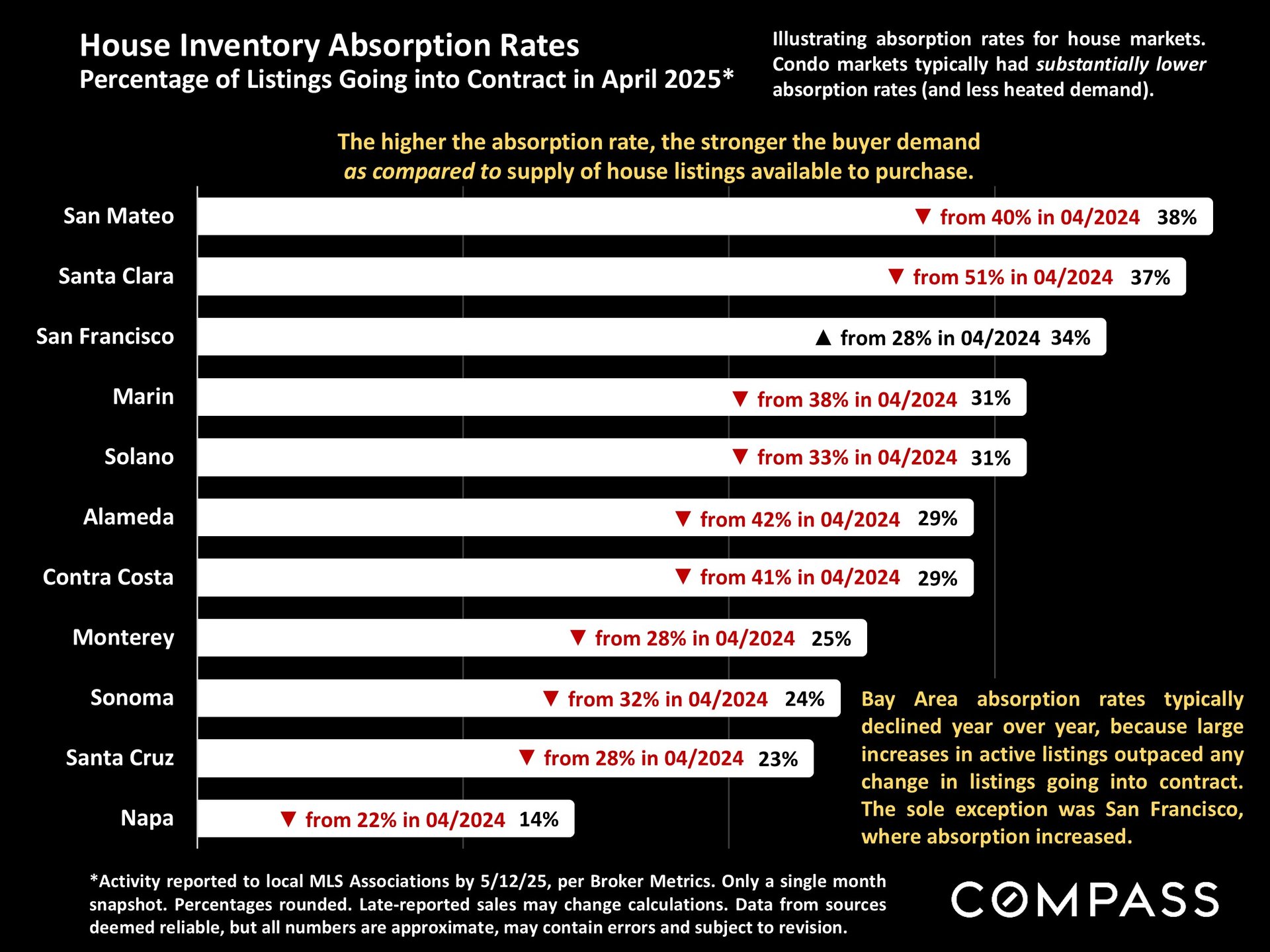

Bay Area April 2025 absorption rates - for houses (updated 5/12/25): Counties were affected to varying degrees by the political/economic chaos in April (which now seems to be moderating). Due to the AI boom, San Mateo & Santa Clara Counties continued to see the highest demand in the Bay Area, followed by SF. All counties saw declines in absorption rates, sometimes very significant declines, except for San Francisco, which saw a year over year increase. SF also saw by far the smallest increase in the number of active listings year over year, and the large to very large increases in listings played a substantial role in the decline in absorption rates in other counties. Condo markets across the Bay Area generally saw much lower absorption rates: For example, the SF condo market had a 20% absorption rate compared to the 34% rate for houses.

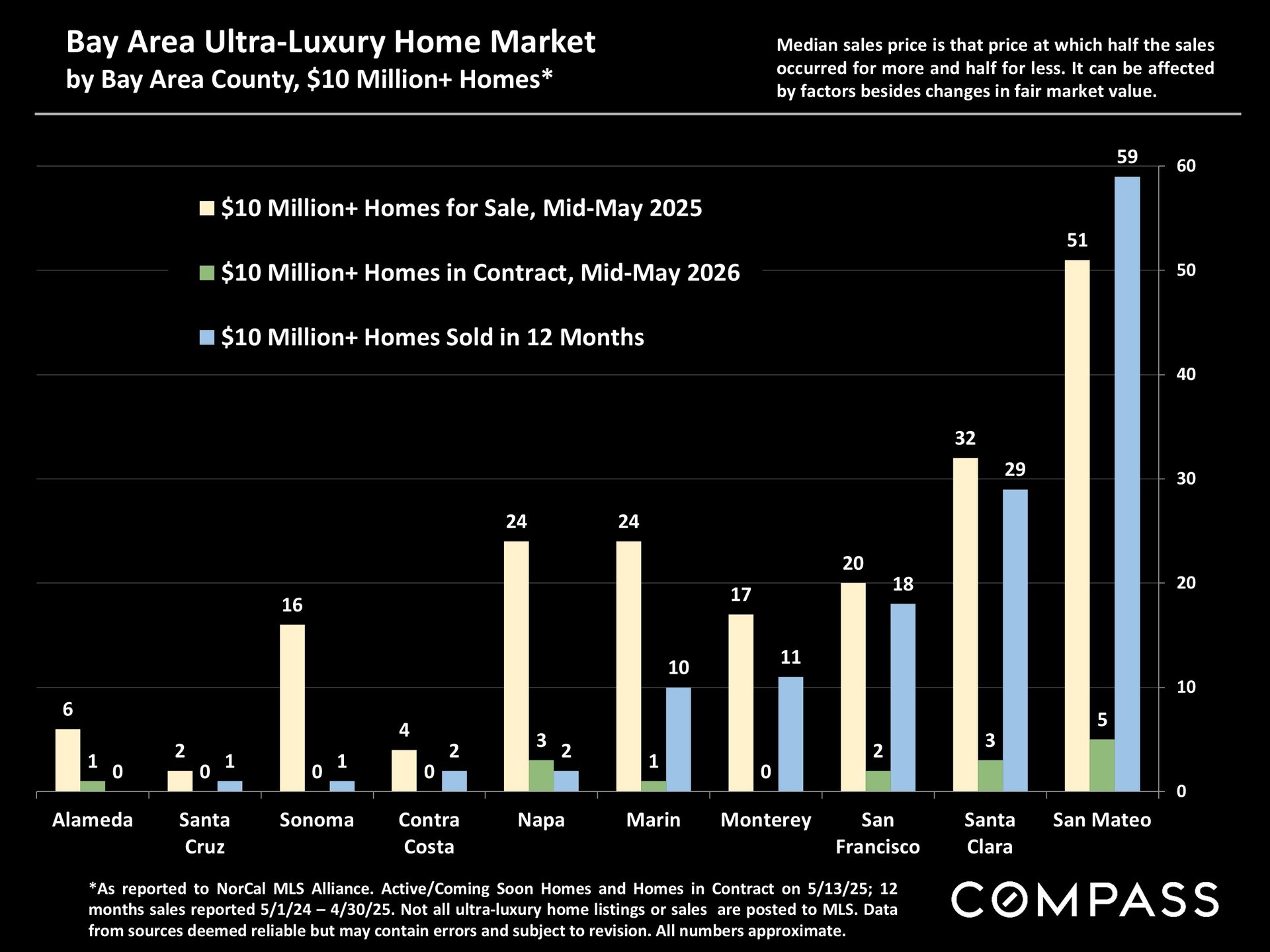

A snapshot of $10 million+ ultra-luxury homes markets: Homes for Sale, Homes in Contract, 12 months Sales. San Mateo & Santa Clara Counties continue to see the strongest markets in $10m homes (AI boom), followed by SF, Monterey and Marin. The Wine Country has an extremely high number of active listings (40) when compared to its 12-month rate of sales (3, plus 3 currently in contract). In Alameda, Contra Costa and Santa Cruz, the ultra luxury market would probably be defined at $4 million+, and there is very little activity in the $10m+ segment.