San Francisco Real Estate

January 2023 Report

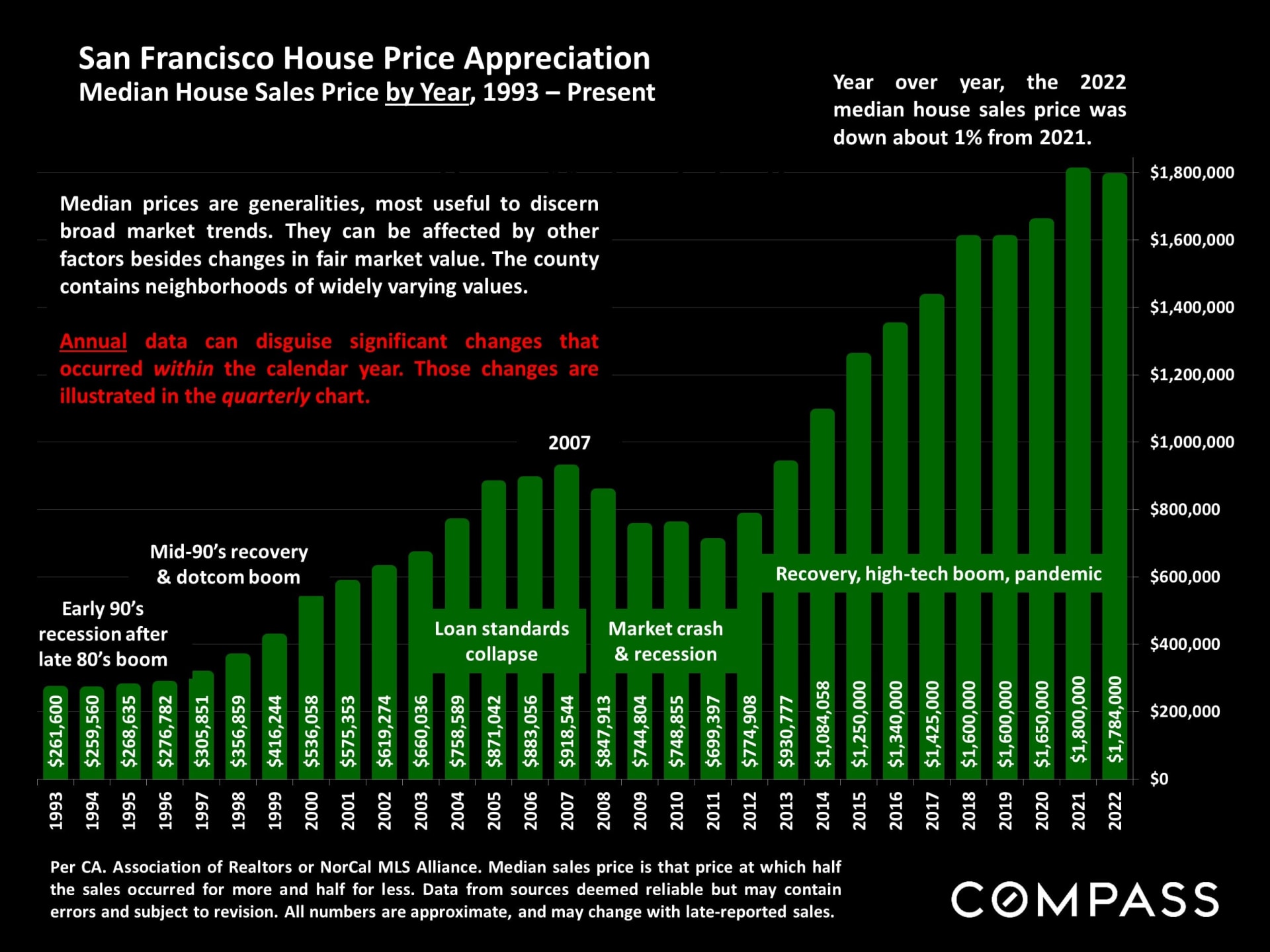

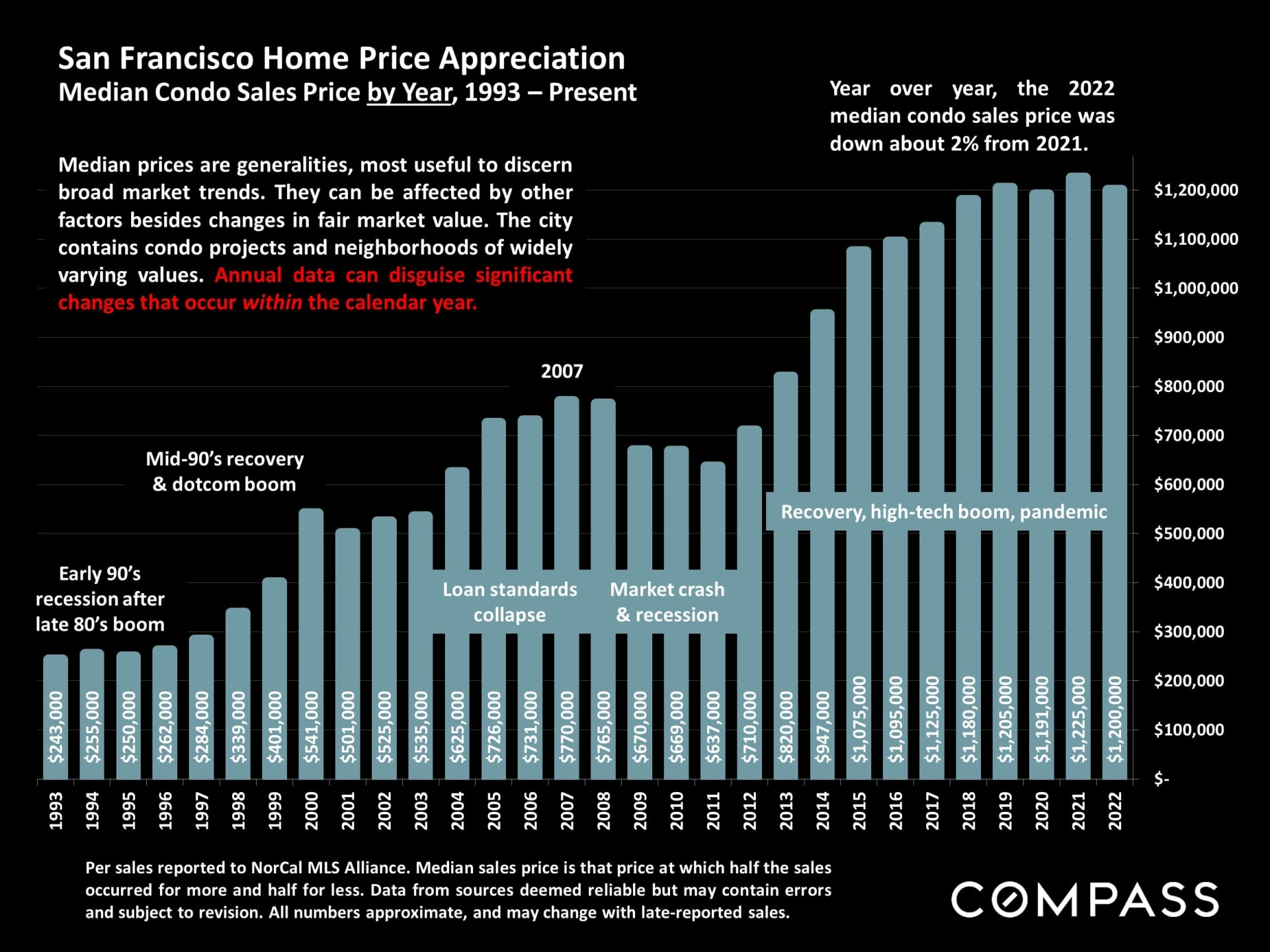

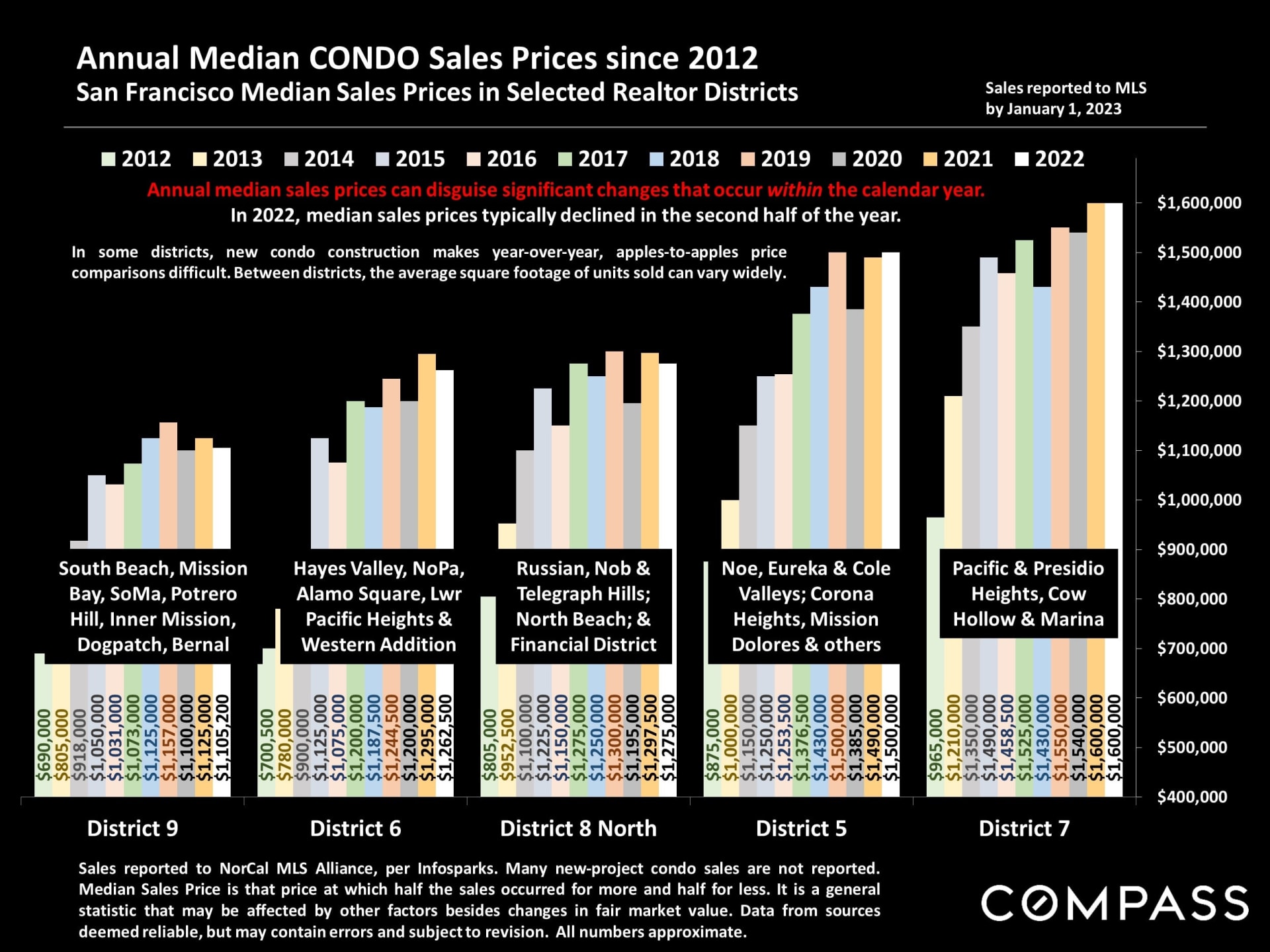

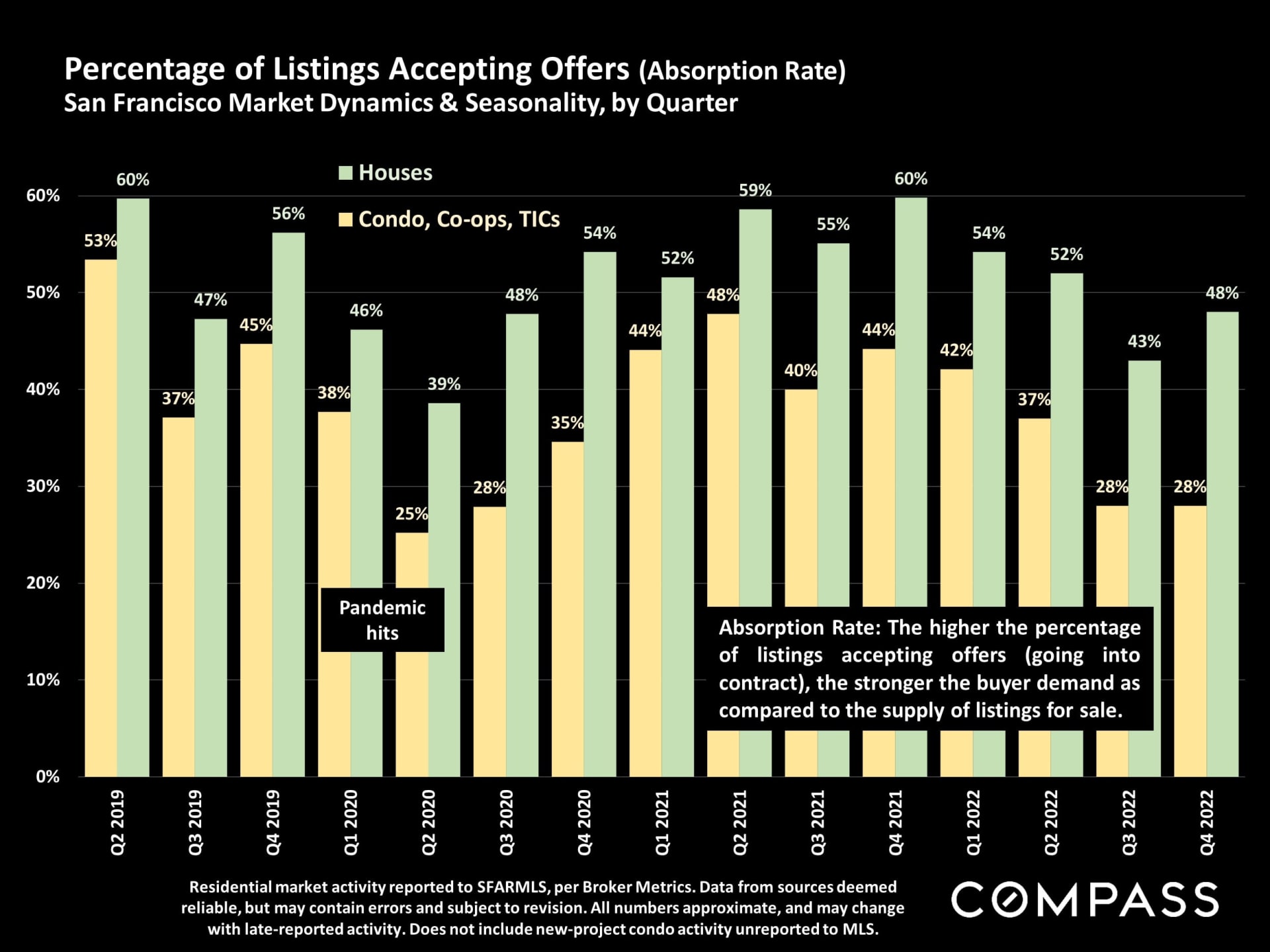

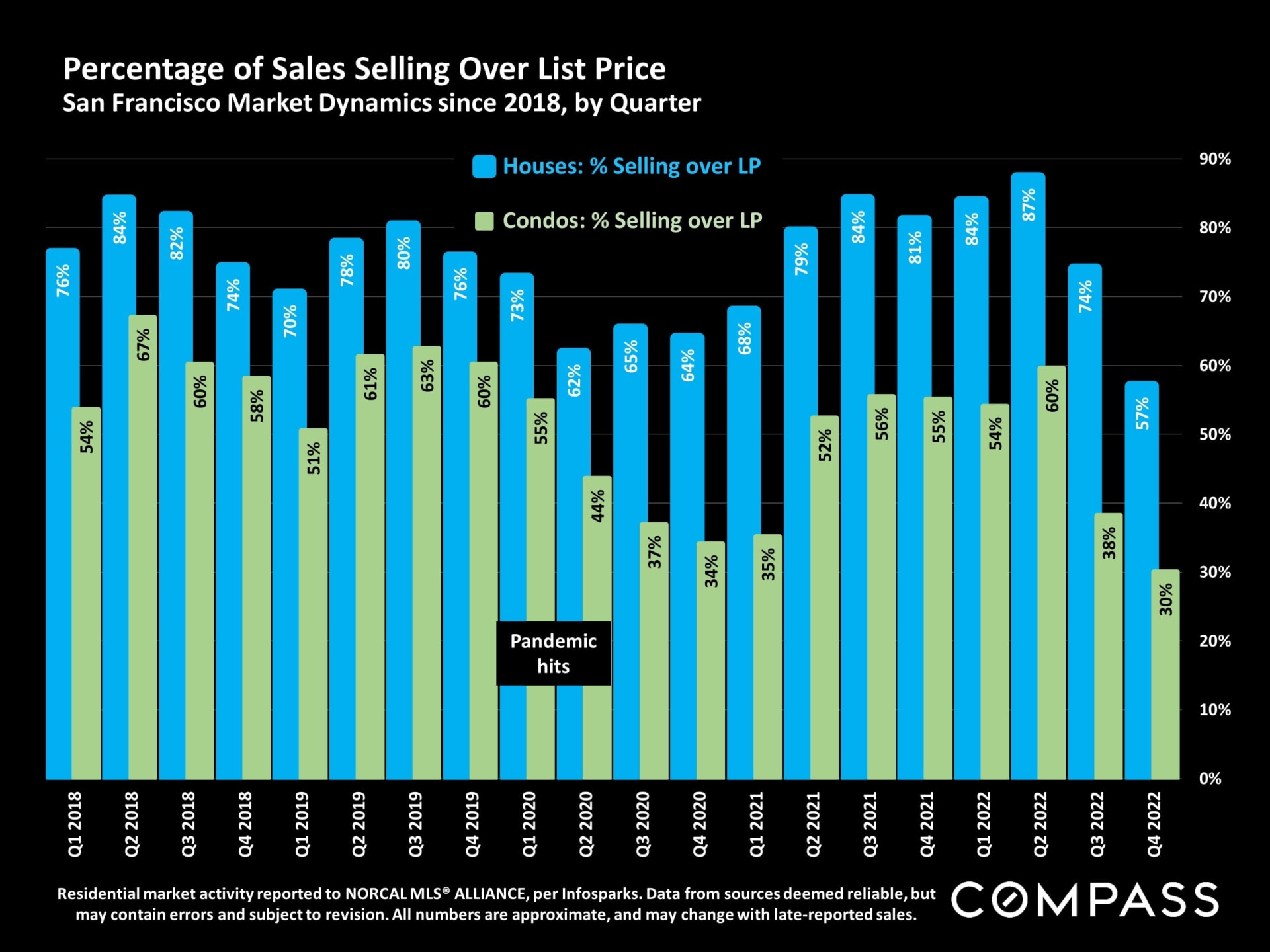

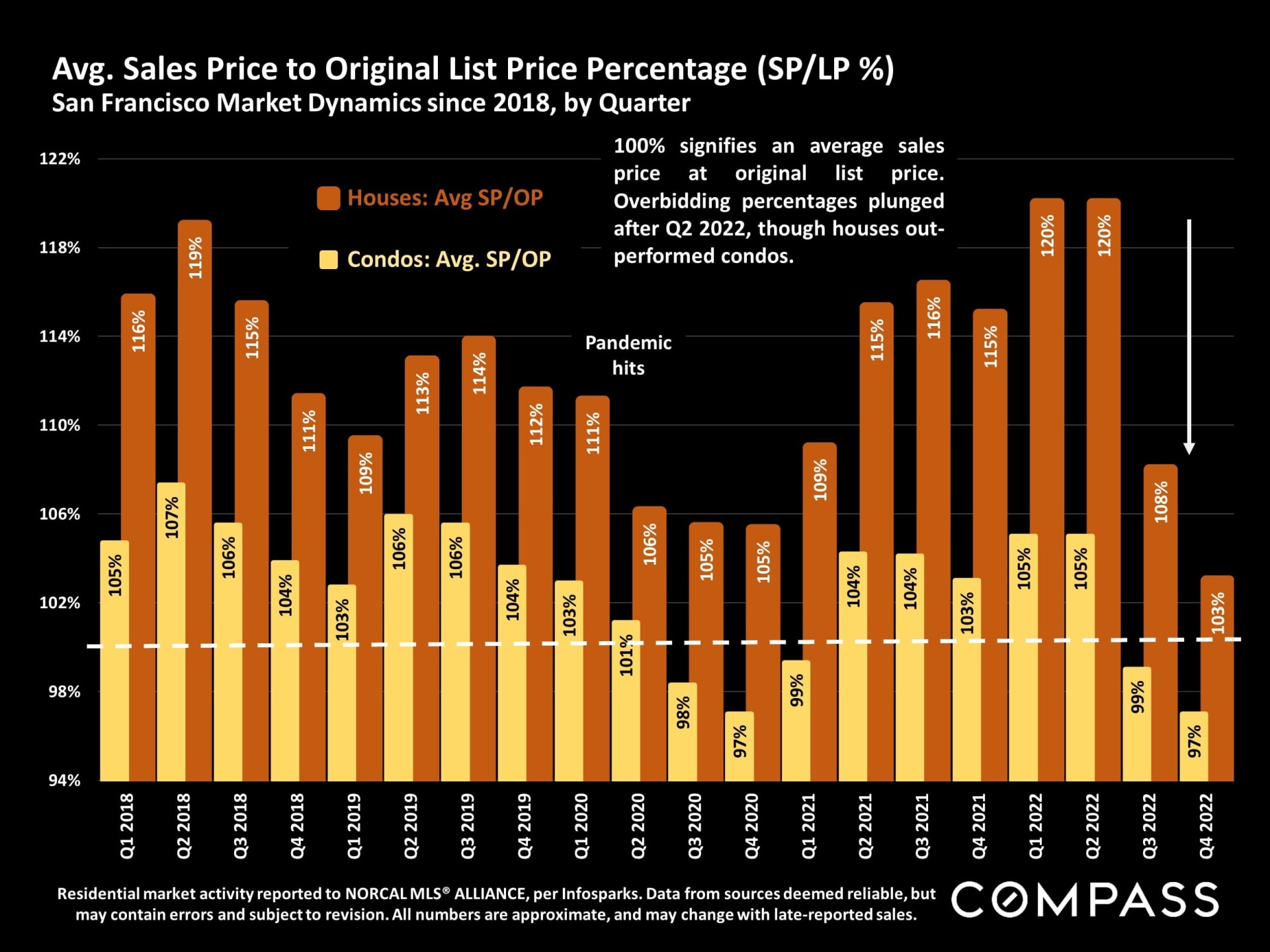

2022 Review of Selected Indicators

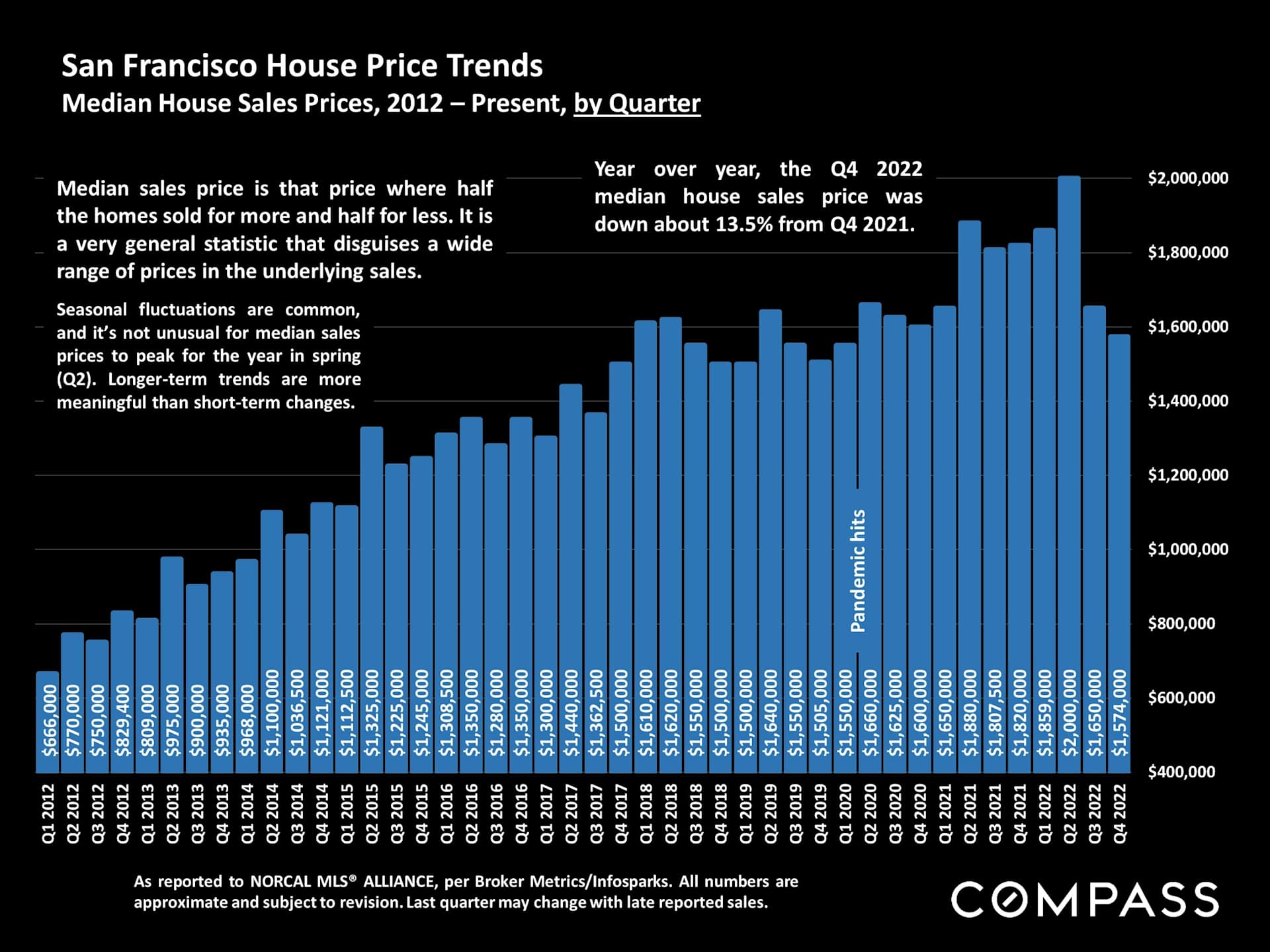

Real Estate Market Statistics, Comparing Q4 2022 to Q4 2021 (Annual median house price changes – 2021 to 2022 – can also be found within this report.)

- Quarterly Median House Sales Price: Down 13.5% from Q4 2021

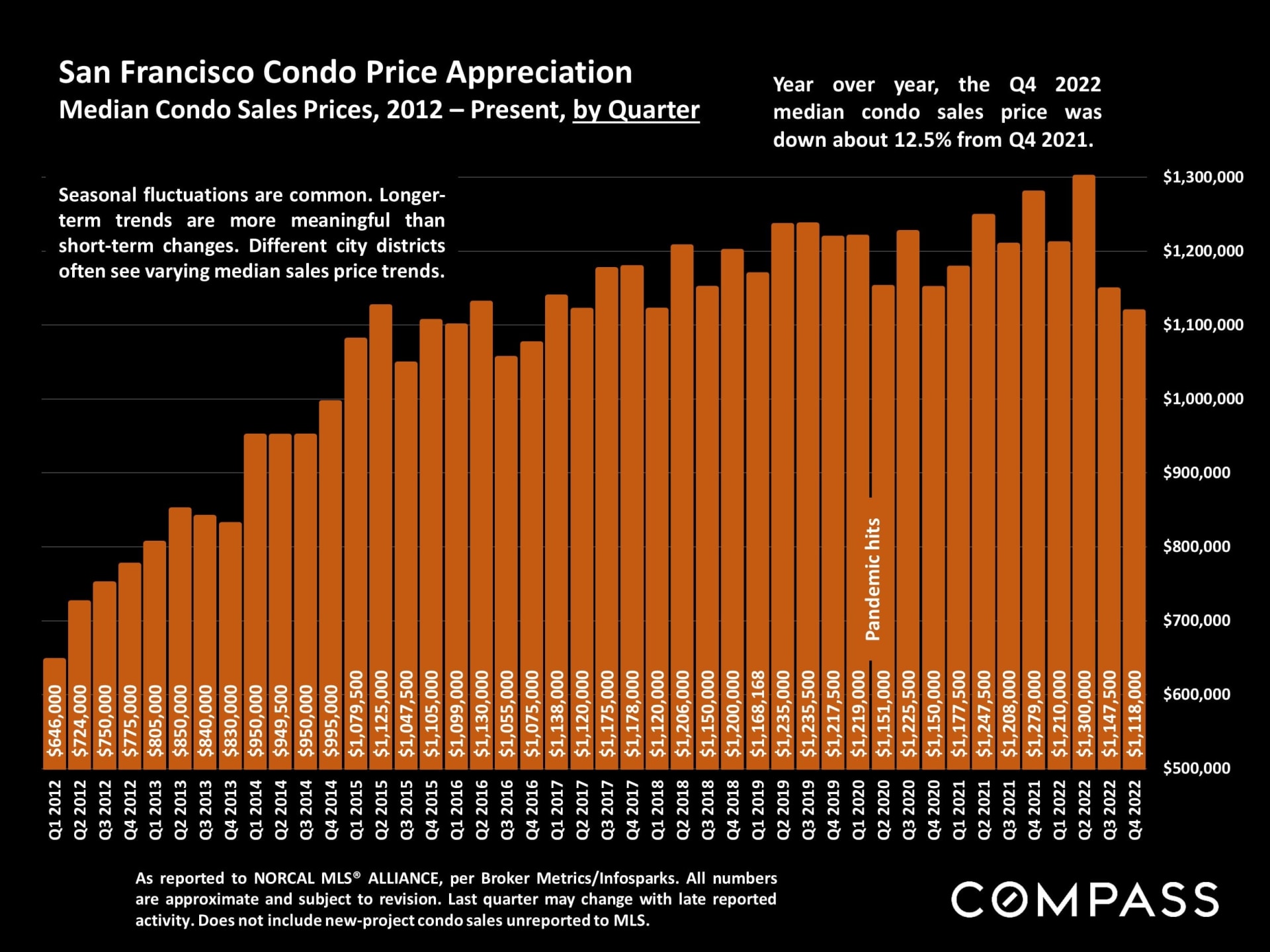

- Quarterly Median Condo Sales Price: Down 12.5% from Q4 2021

- Quarterly Sales Volume: Down 42%

- % of Sales over Final List Price: 43%, down from 66% in Q4 2021

- Avg. Sales Price to Original List Price %: 100% (at list price), down from 108% in Q4 2021

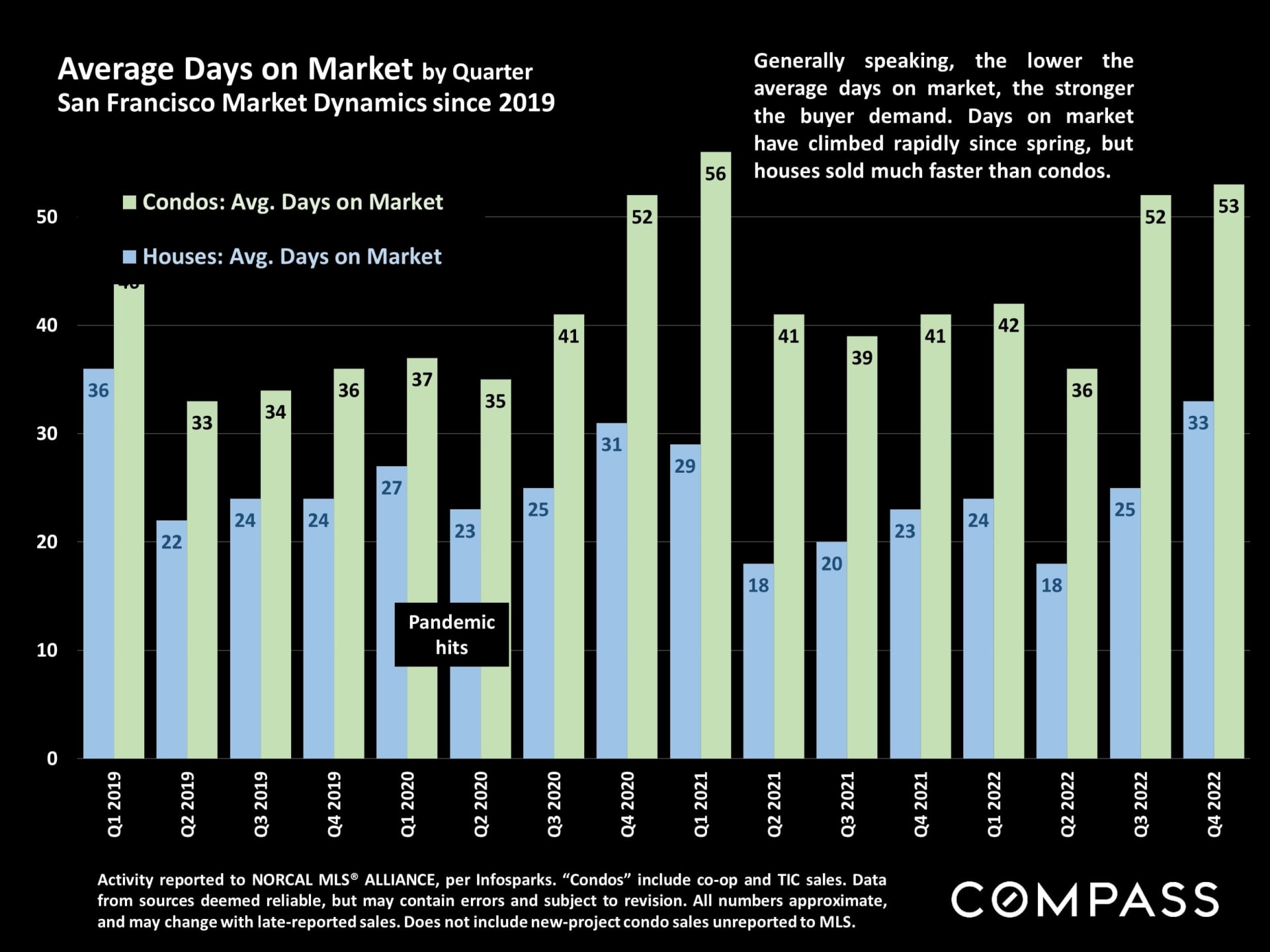

- Average Days on Market: 44 days, up from 34 days in Q4 2021

- Absorption Rate (% of listings into contract): 36% of listings, down from 49% in Q4 2021

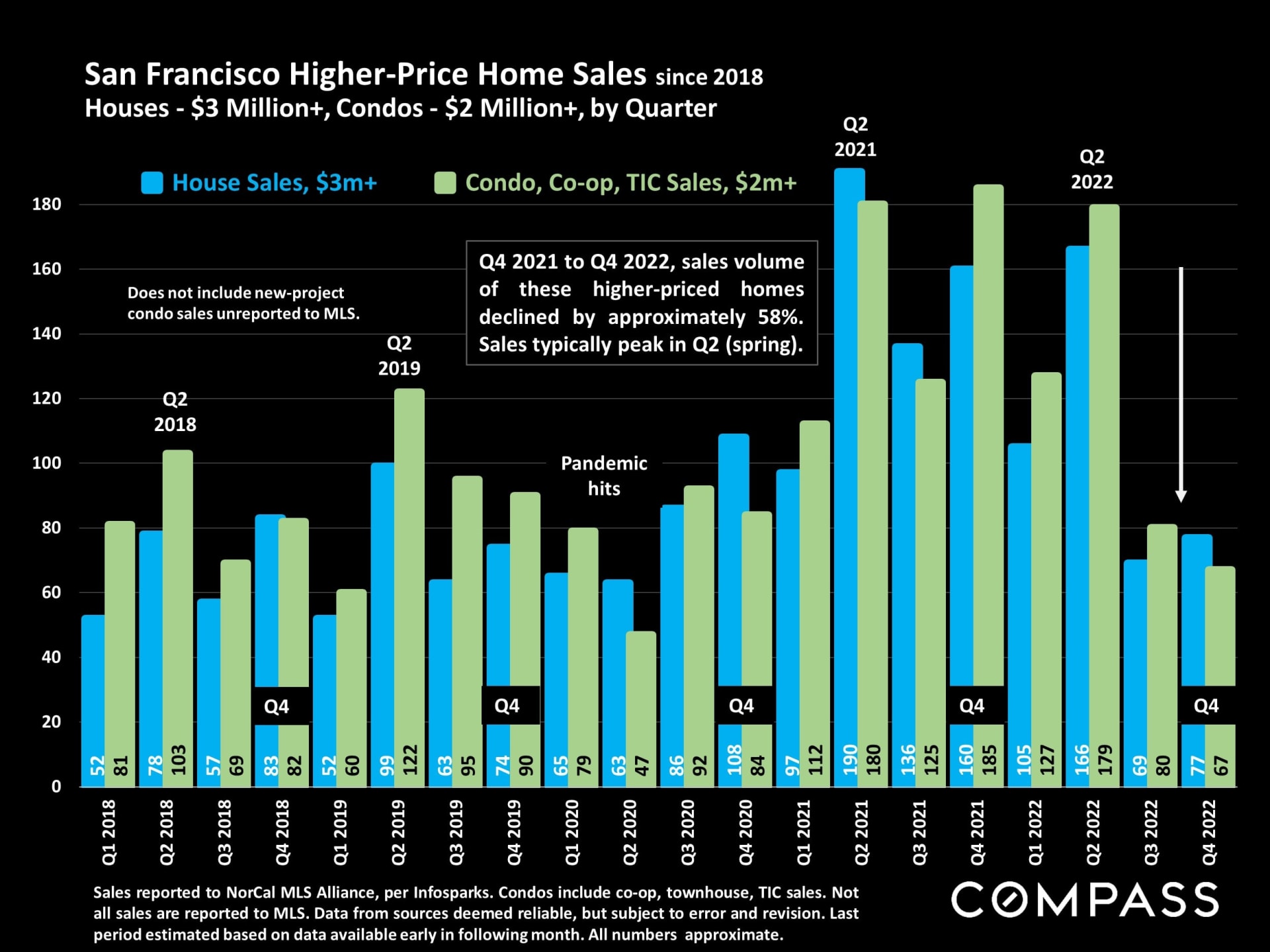

- Luxury Home Sales Volume, Sales $3 Million+: Down 52% from Q4 2021

Major Economic Indicators in 2022

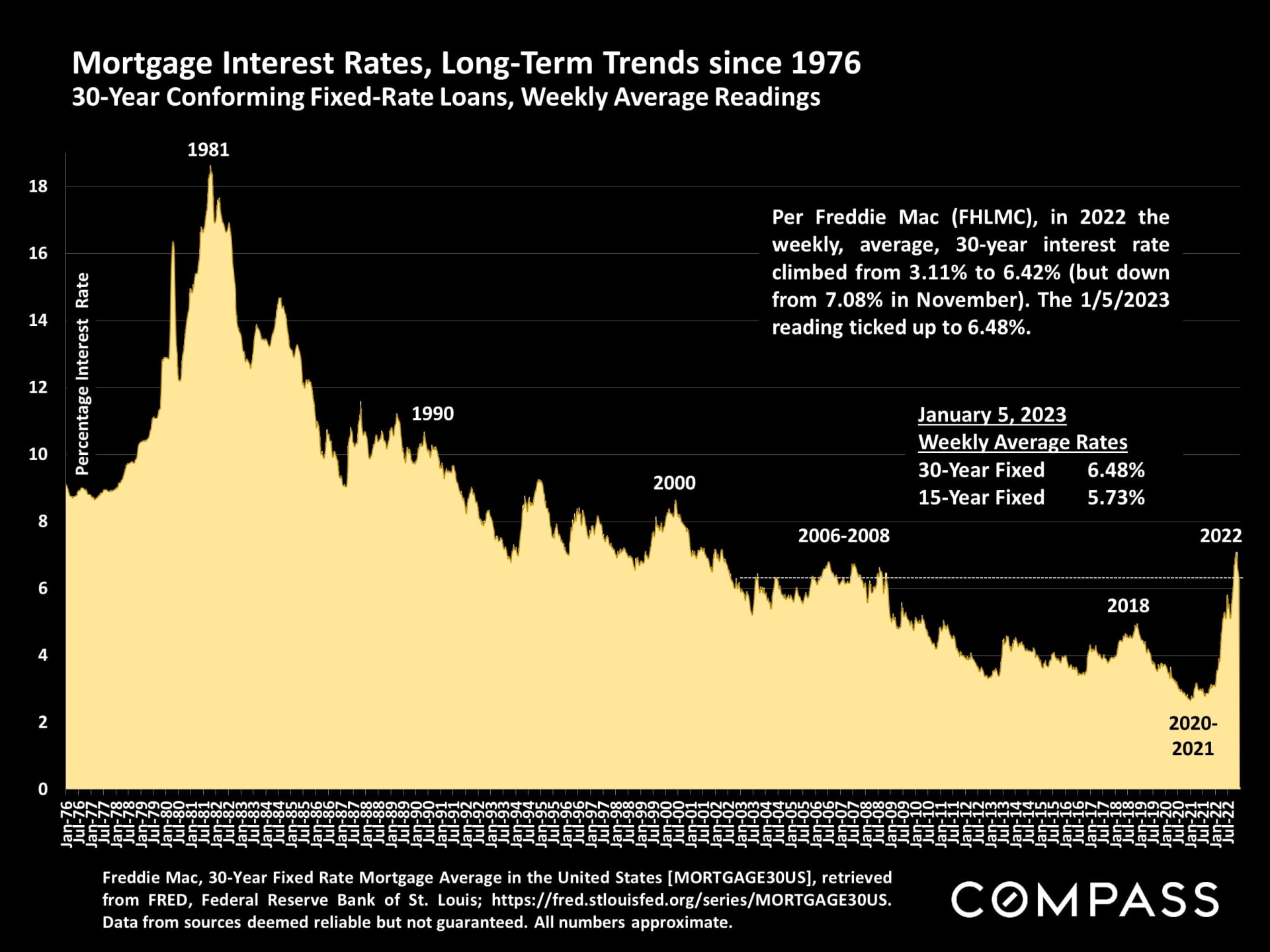

- Weekly Avg. 30-Year Mortgage Rate: Climbed from 3.11% to 6.42% (but is down from 7.08% peak in November 2022)

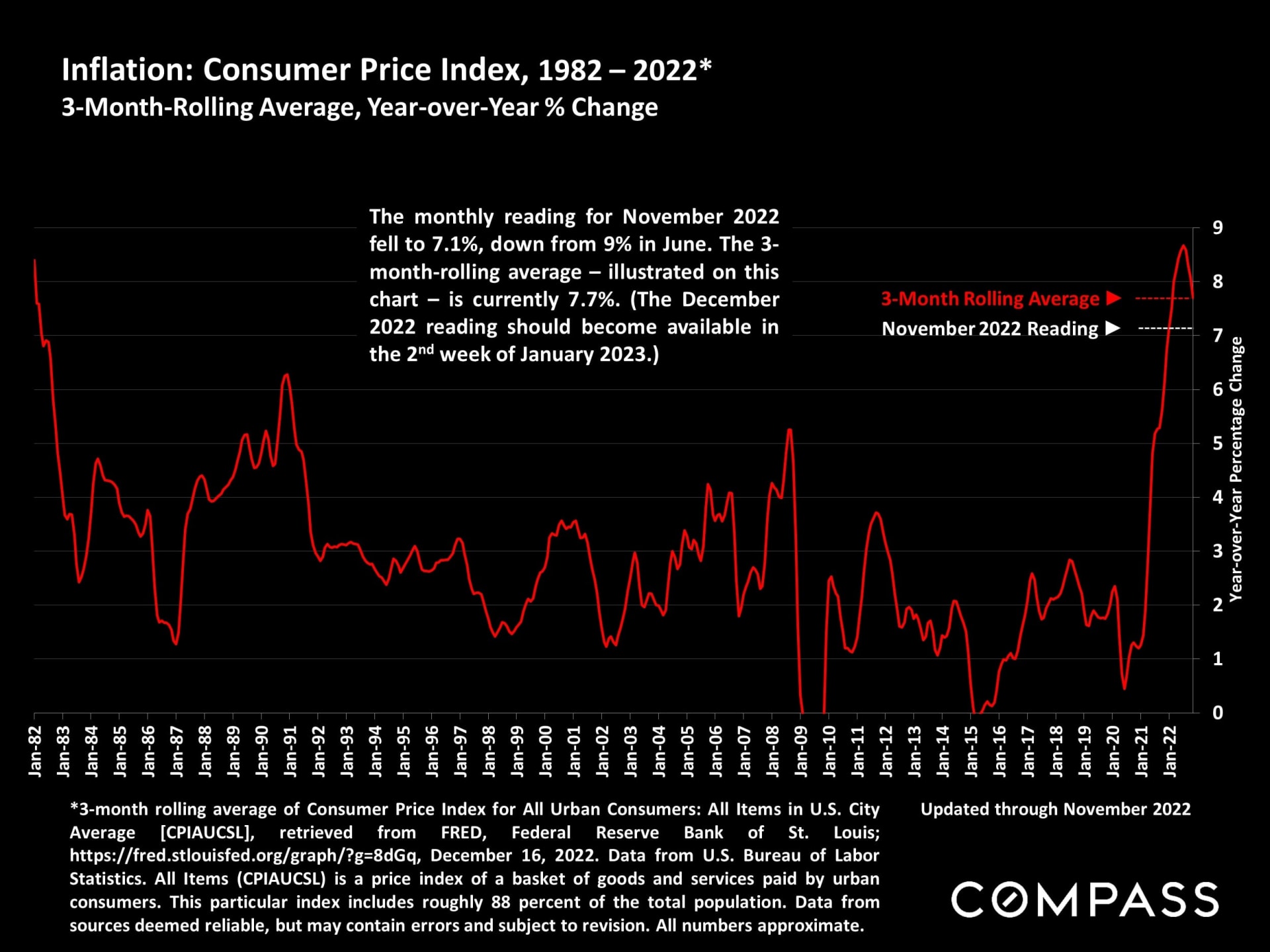

- Consumer Price Index (inflation rate): January to November, dropped from 7.5% to 7.1% (It is down from 9% peak in June 2022, but up from 1.4% in January 2020.)

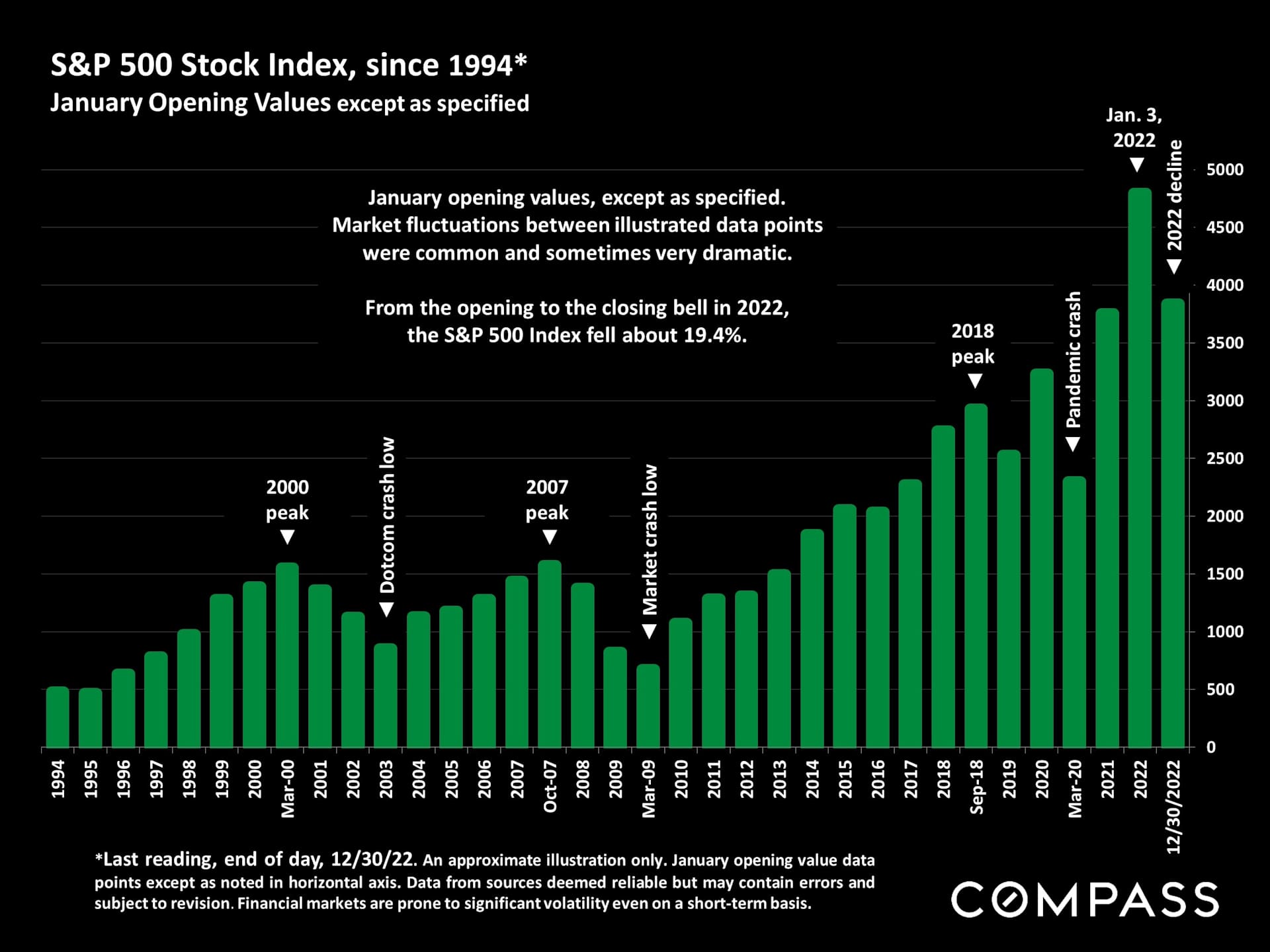

- S&P Stock Index: Opening to closing bell in 2022, down approximately 19.4%

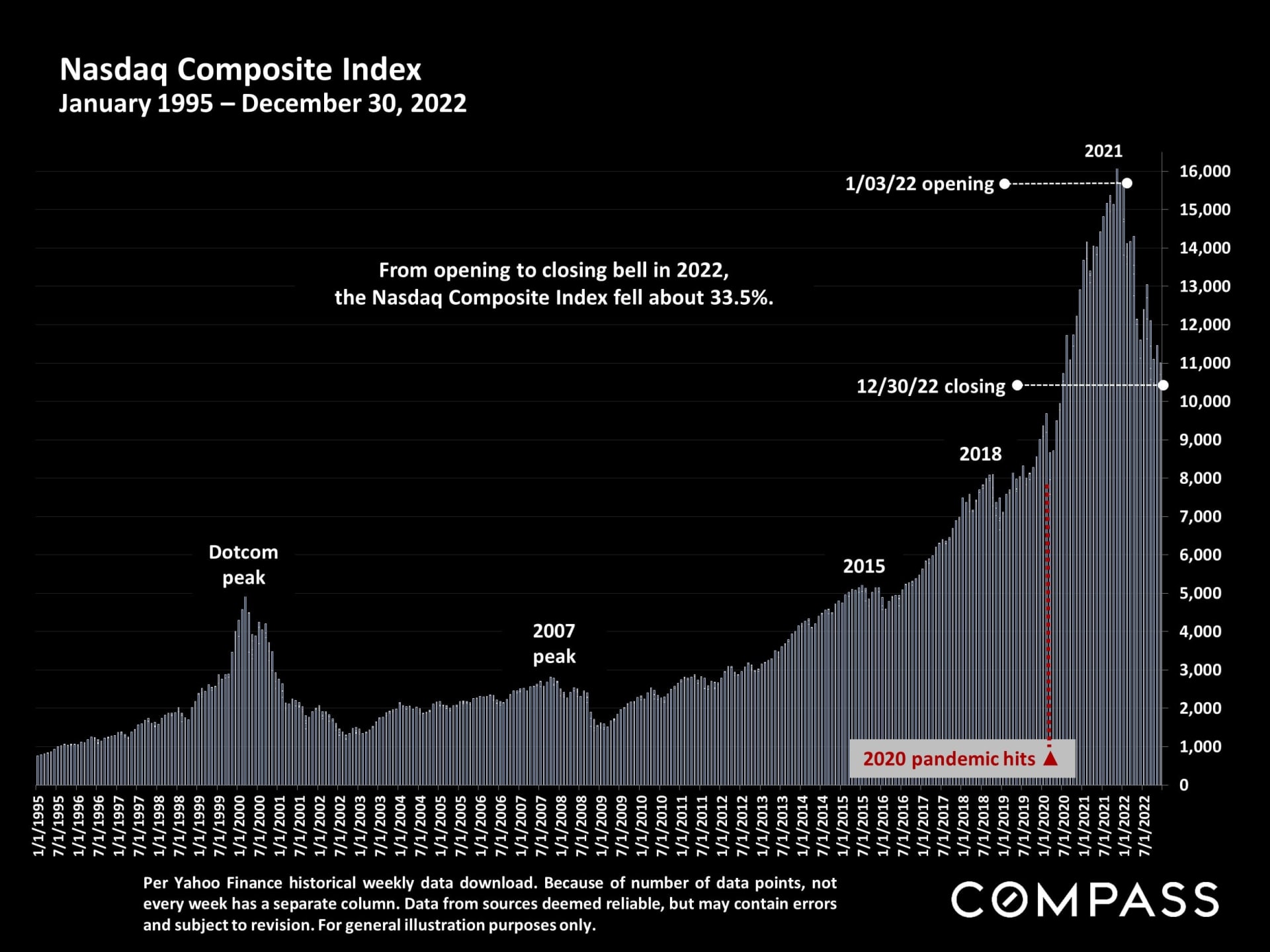

- Nasdaq Stock Index: Opening to closing bell in 2022, down approximately 33.5%

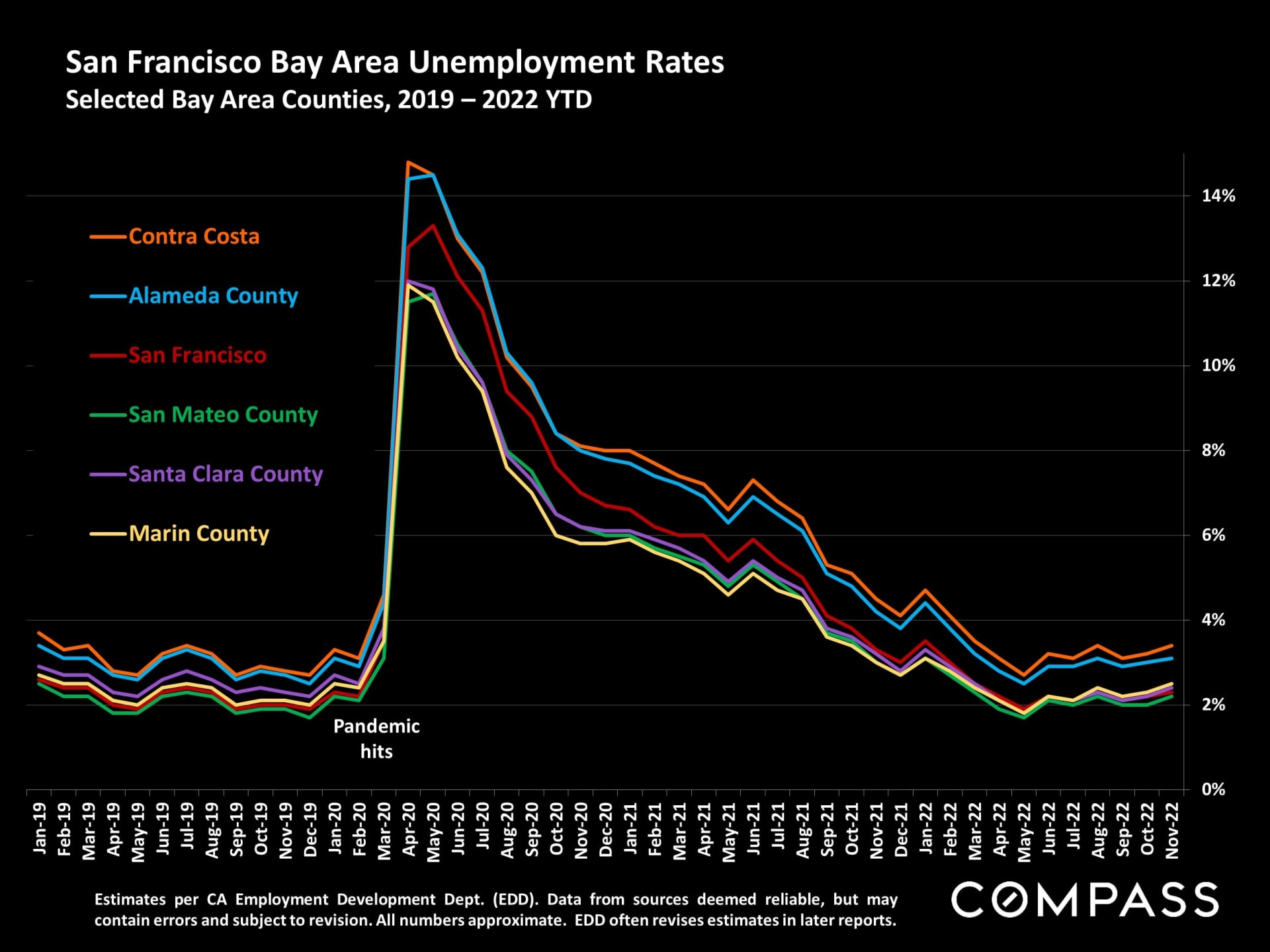

- Employment: Bay Area unemployment rates remain close to historic lows. (According to the WSJ, “Most laid off tech workers are finding jobs shortly after beginning their search”).

Mortgage rate data per FHLMC. Stock market data per Marketwatch.com. Consumer Price Index, all urban consumers, per Federal Reserve Bank of St. Louis. Market statistics per sales reported to NorCal MLS Alliance, per Infosparks or Broker Metrics, or the CA Association of Realtors. Statistics are very general indicators. All numbers are approximate. Market statistics from data available in early January 2023 and may change with late-reported sales. How this data applies to any particular property is unknown without a specific comparative market analysis.“Mortgage application activity sunk to a quarter century low this week as high mortgage rates continue to weaken the housing market. While mortgage market activity has significantly shrunk over the last year, inflationary pressures are easing and should lead to lower mortgage rates in 2023. Homebuyers are waiting for rates to decrease more significantly, and when they do, a strong job market and a large demographic tailwind of Millennial renters will provide support to the purchase market.” FHLMC, 1/5/2023

In 2022, the market saw a dramatic shift from Q2 (spring), at which time the market peaked after a dramatic 10-year upcycle supercharged at its end by the pandemic boom, through the 2 nd half of the year, when the market cooled significantly. Prompted by a number of economic factors - especially inflation and interest rates, and financial markets - this played out in substantial declines in sales volumes, median sales prices, appreciation rates, and virtually all the standard measurements of buyer demand. However, tens of thousands of Bay Area homes continued to sell in the 2 nd half, a considerable, but declining percentage still selling quickly at over asking price. On the other hand, some buyers are making the best deals in years. For sellers, pricing, preparation and marketing are now critical, while buyers shouldn’t hesitate to negotiate aggressively, especially on homes with longer days-on-market.

The period from just before Thanksgiving through mid-January usually sees the lowest levels of listing and offer-acceptance activity of the year, so it’s difficult to derive definitive conclusions about market trends from its numbers. The early spring market – which, weather cooperating, can begin as early as February in the Bay Area – would typically provide the next major indicator of market direction, but developments may occur sooner to provide increased clarity regarding what awaits us in 2023. For the time being, the market remains in a period of adjustment, with major macroeconomic conditions still in flux.

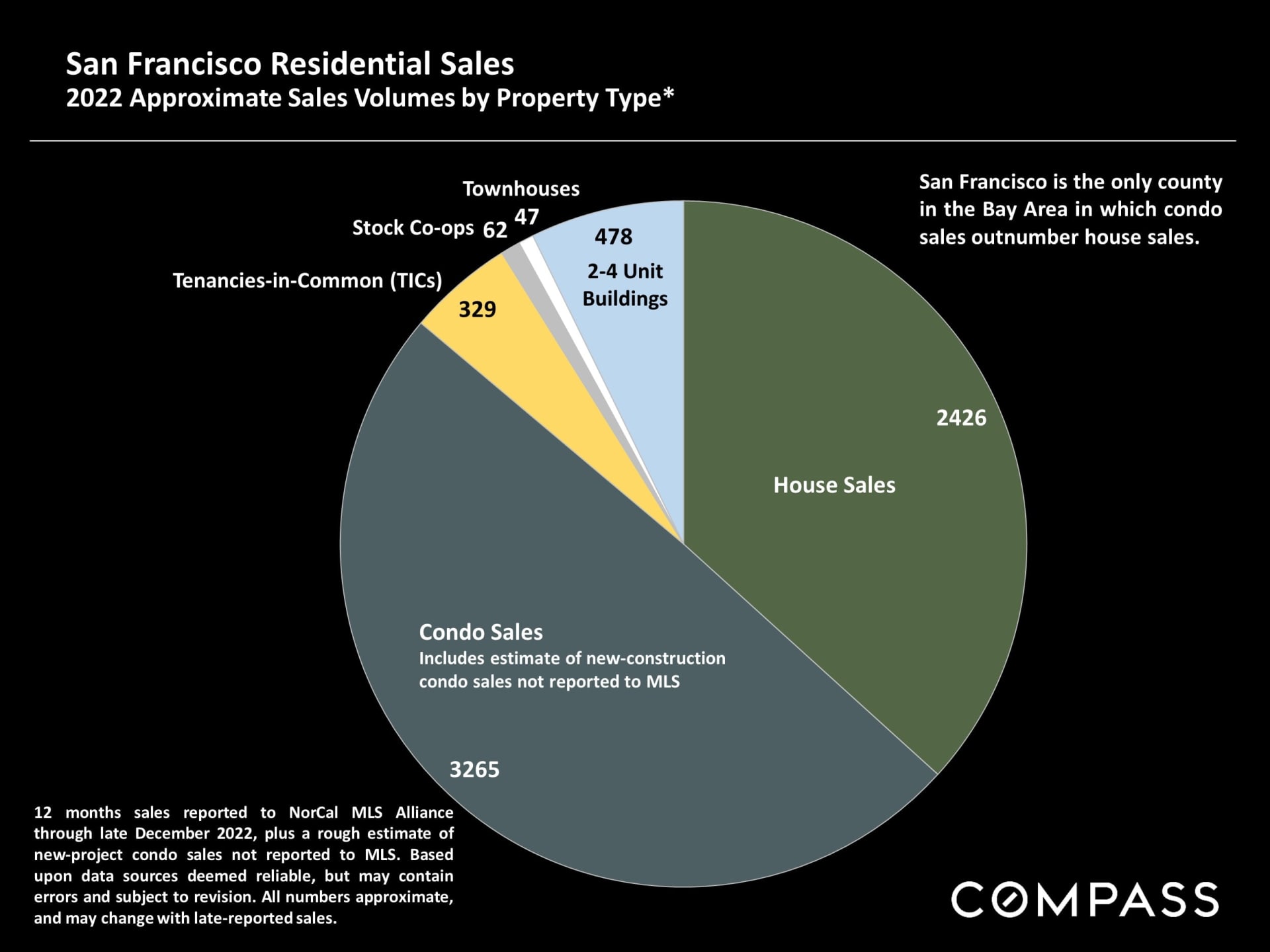

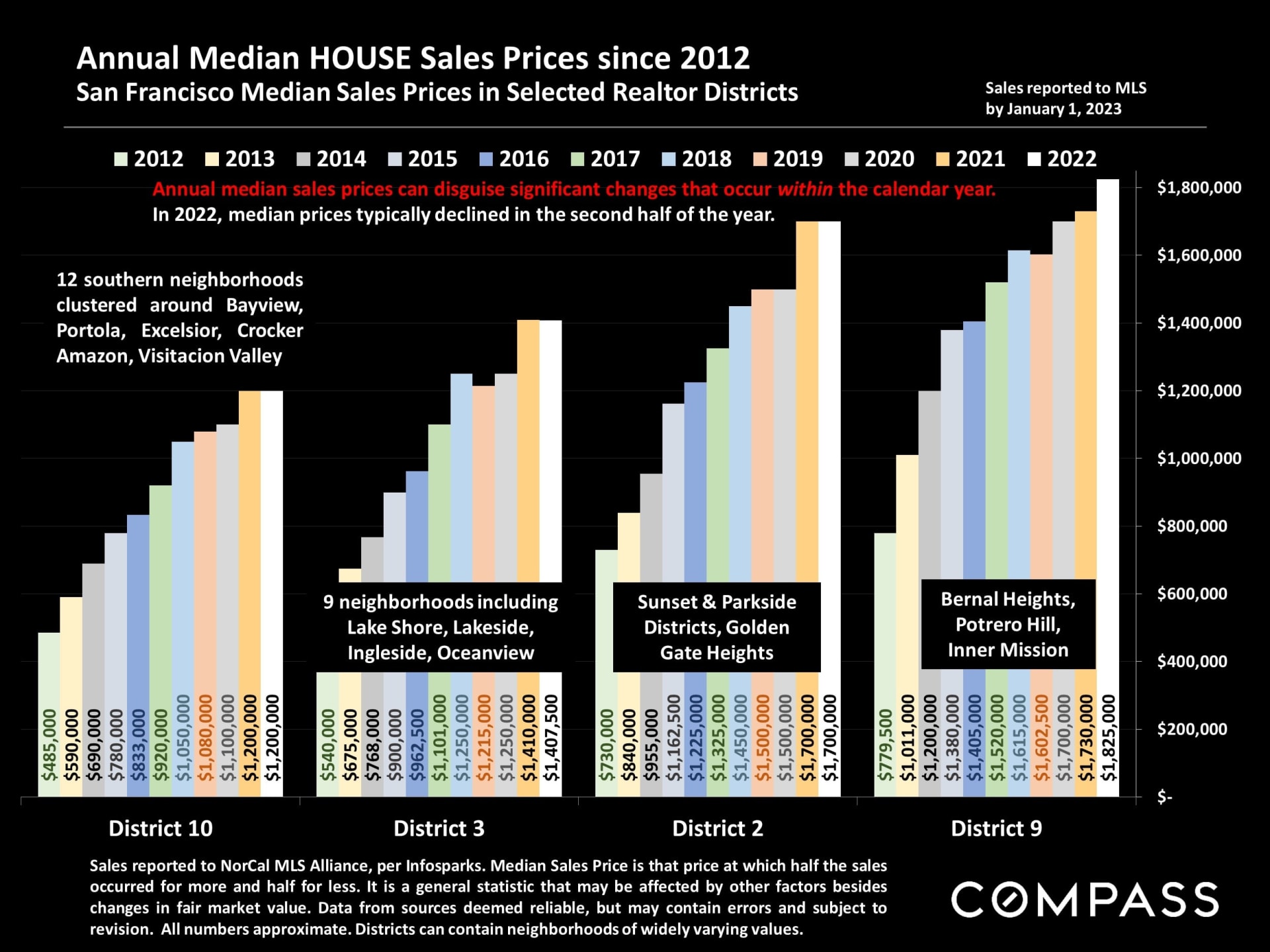

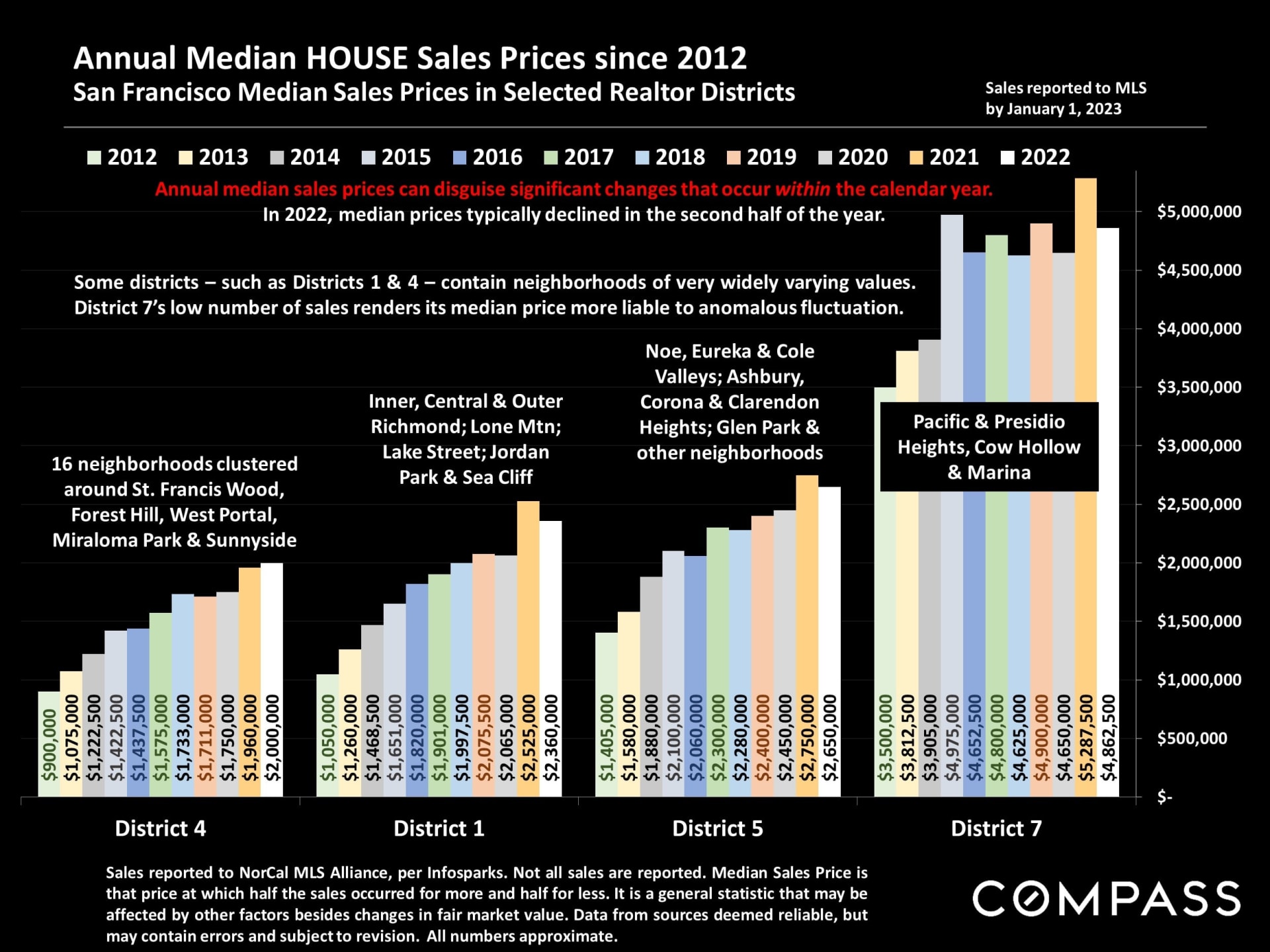

This report will look at the market from a variety of angles, including annual, quarterly and monthly data. Because of the large shifts in the market that occurred between the 1 st and 2 nd halves of the year, annual data will often disguise these changes, blending as it does heated, peak-market data with data in which very different conditions prevailed.