Inflation report released Tuesday, March 12th: General CPI slightly up, "Core CPI" slightly down. The Fed is still expected to lower the benchmark rate - presumably multiple times - later this year, but the lack of significant movements down in CPI is not adding any urgency to doing so. Meanwhile, every time Powell tugs his earlobe or scratches his nose, markets react.

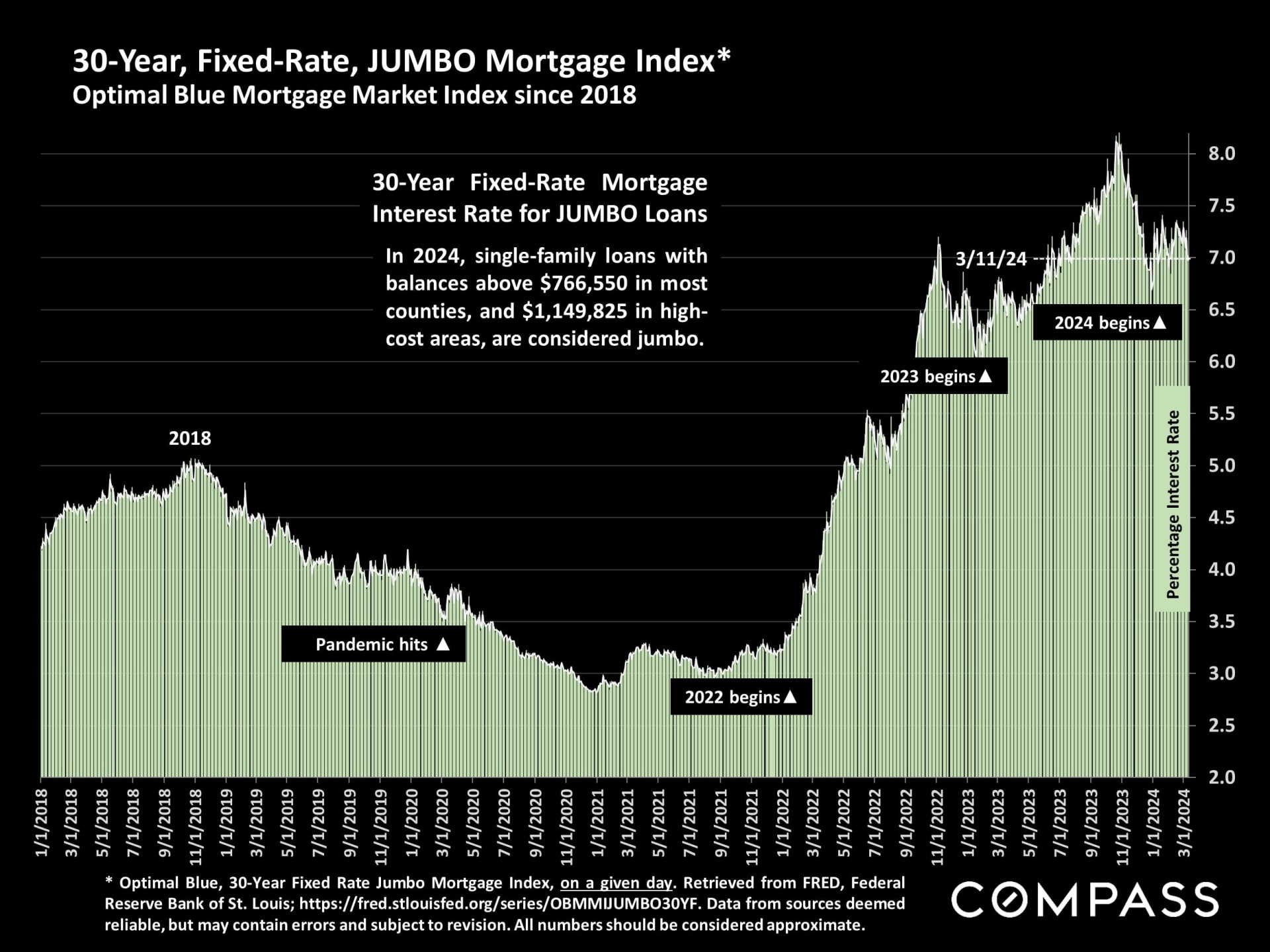

Daily JUMBO mortgage interest rates: Of course, rates can vary depending on the lender and the specific borrower.

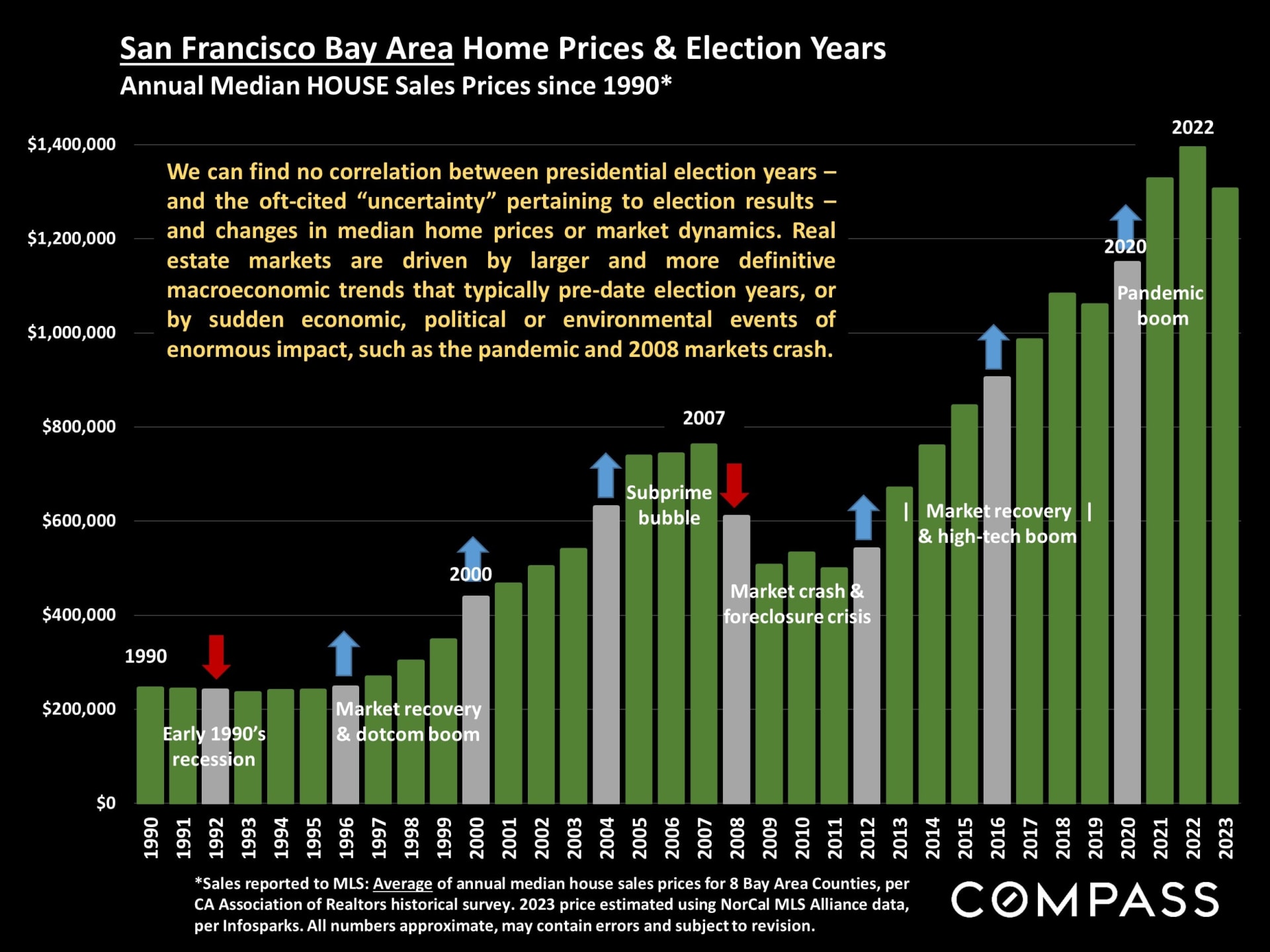

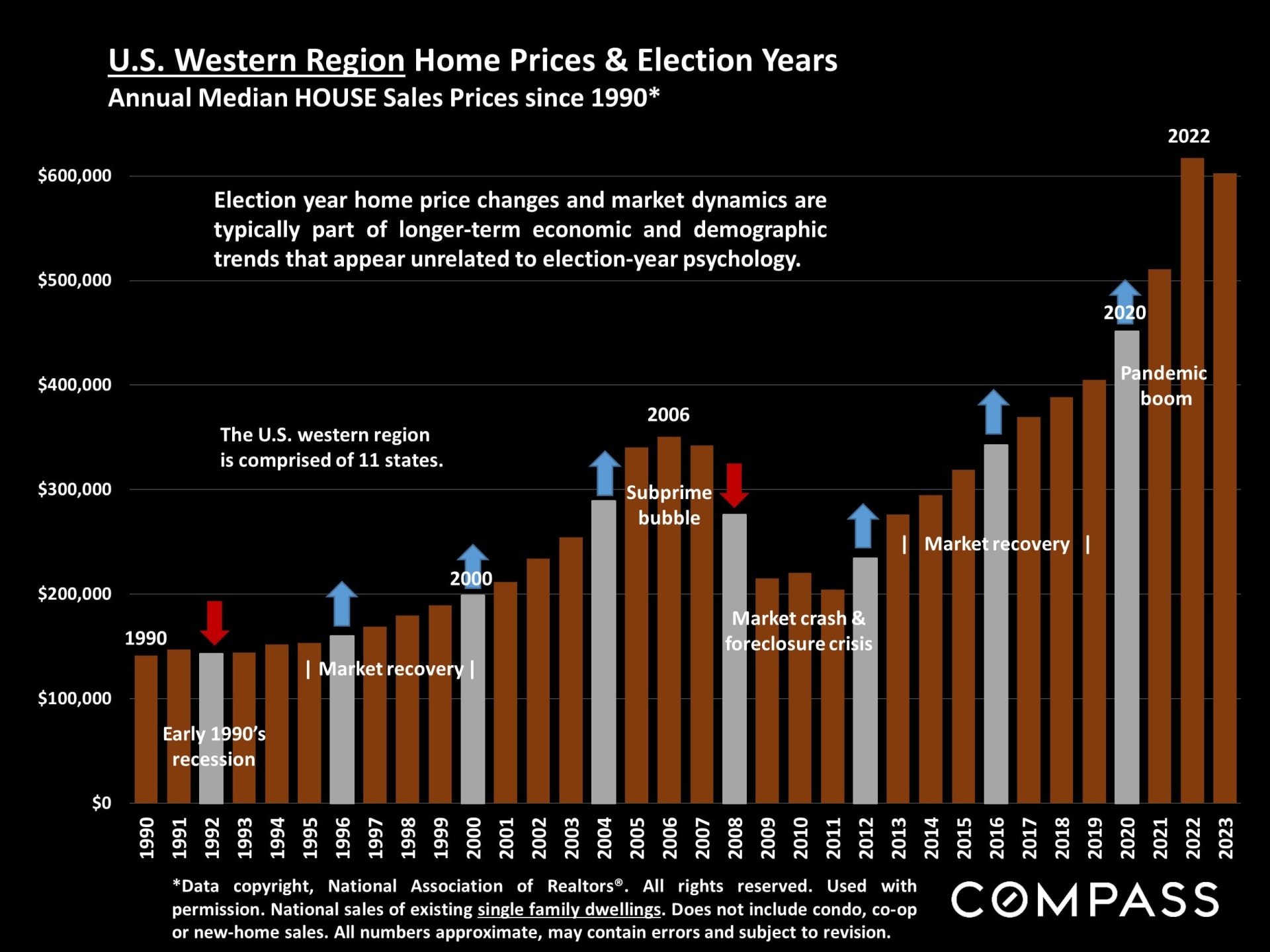

Election years and home prices: Despite the issue coming up every 4 years about election "uncertainty" impacting real estate markets, I can find no evidence of that being a significant factor in market dynamics or prices. Presidential elections have been cause for great uncertainty in most of the elections over the last 30+ years. In 2024, markets appear to be rebounding due to the usual reasons.

2 charts: 1 for the Bay Area, and 1 for the 11-state U.S. western region:

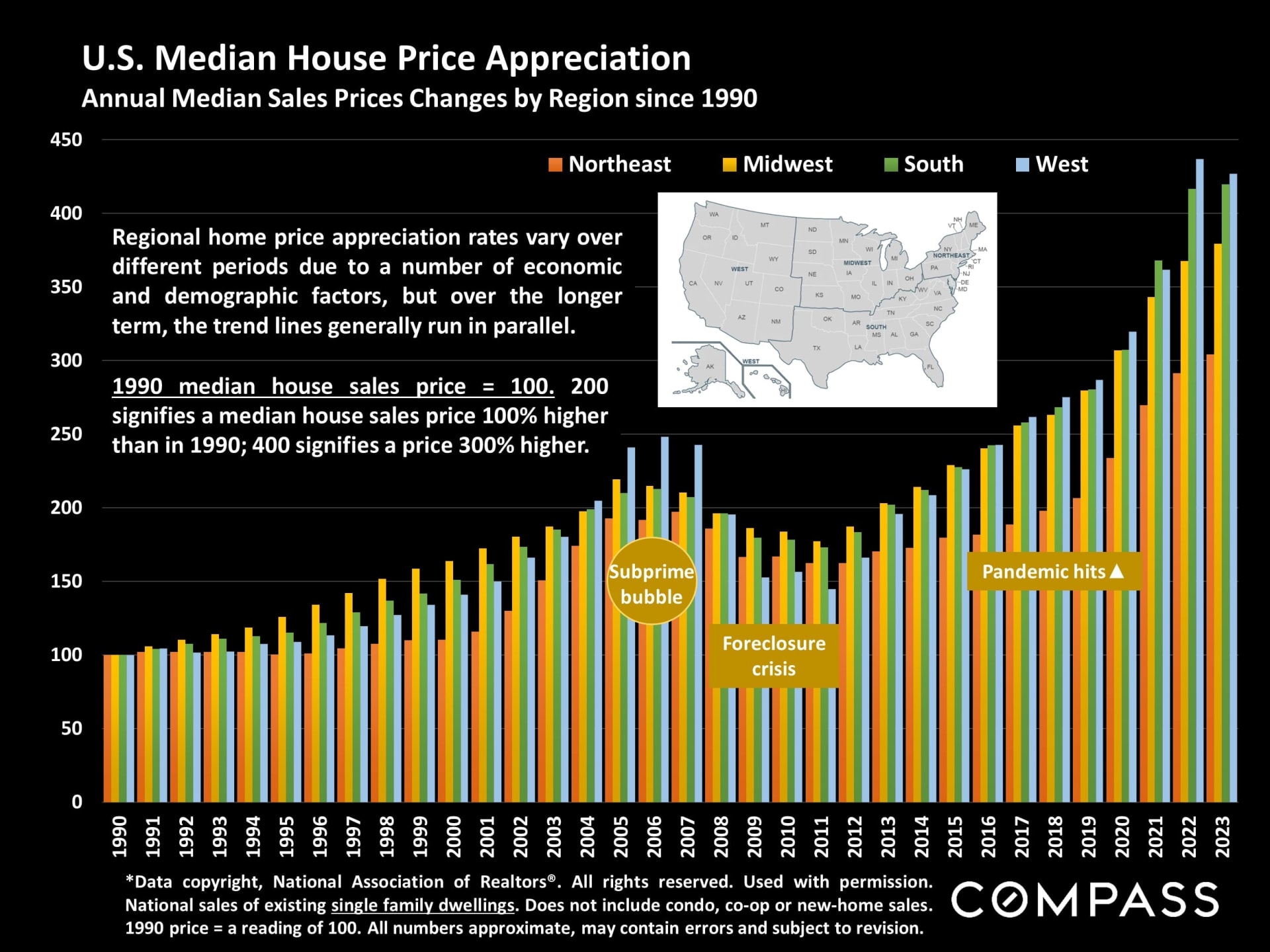

Though local markets can see differing price trends and appreciation rates due to their specific economic and demographic (and now ecological) conditions, over the longer term appreciation rates generally move in parallel over the longer term due to big macroeconomic factors.

Though local markets can see differing price trends and appreciation rates due to their specific economic and demographic (and now ecological) conditions, over the longer term appreciation rates generally move in parallel over the longer term due to big macroeconomic factors.

Latest WEEKLY NATIONAL data from Realtor.com (3/11/24 release): Positive trends on new and active listings, but the numbers remain far, far below long-term norms. Generally speaking, the Bay Area is seeing similar trends in inventory moving into spring.

New listings–a measure of sellers putting homes up for sale–were up this week, by 17.4% from one year ago. Newly listed homes reached above year ago levels for the 19th week in a row.

Active inventory increased, with for-sale homes 19.9% above year ago levels. For a 17th straight week, active listings registered above prior year level ...however, overall inventory is still 40% lower than in 2017-2019.

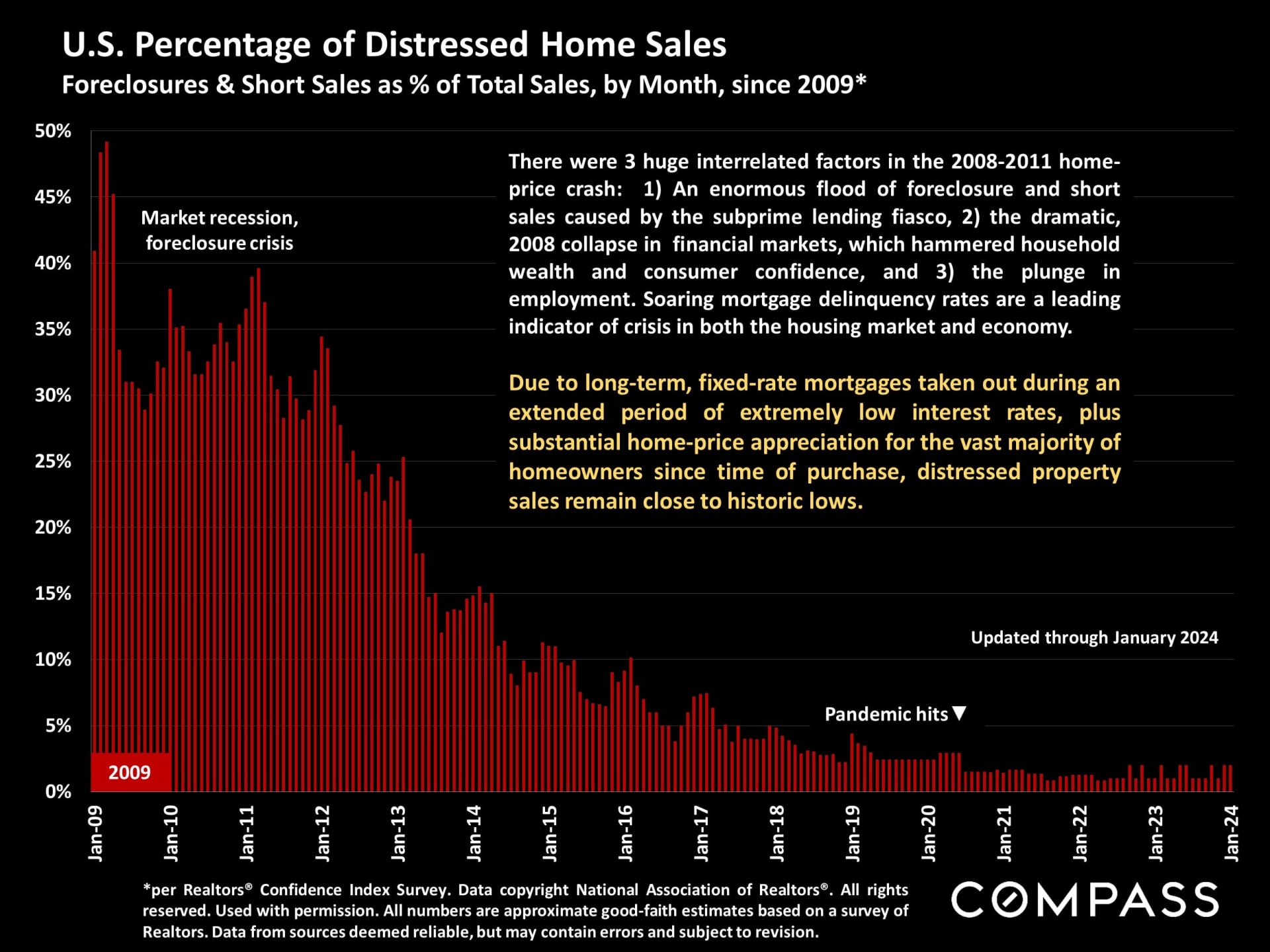

NAR data on distressed property sales: Foreclosures and short sales remain close to historic lows due to the high percentage of homeowners with very low interest-rate mortgages and substantial equity increases since purchase.

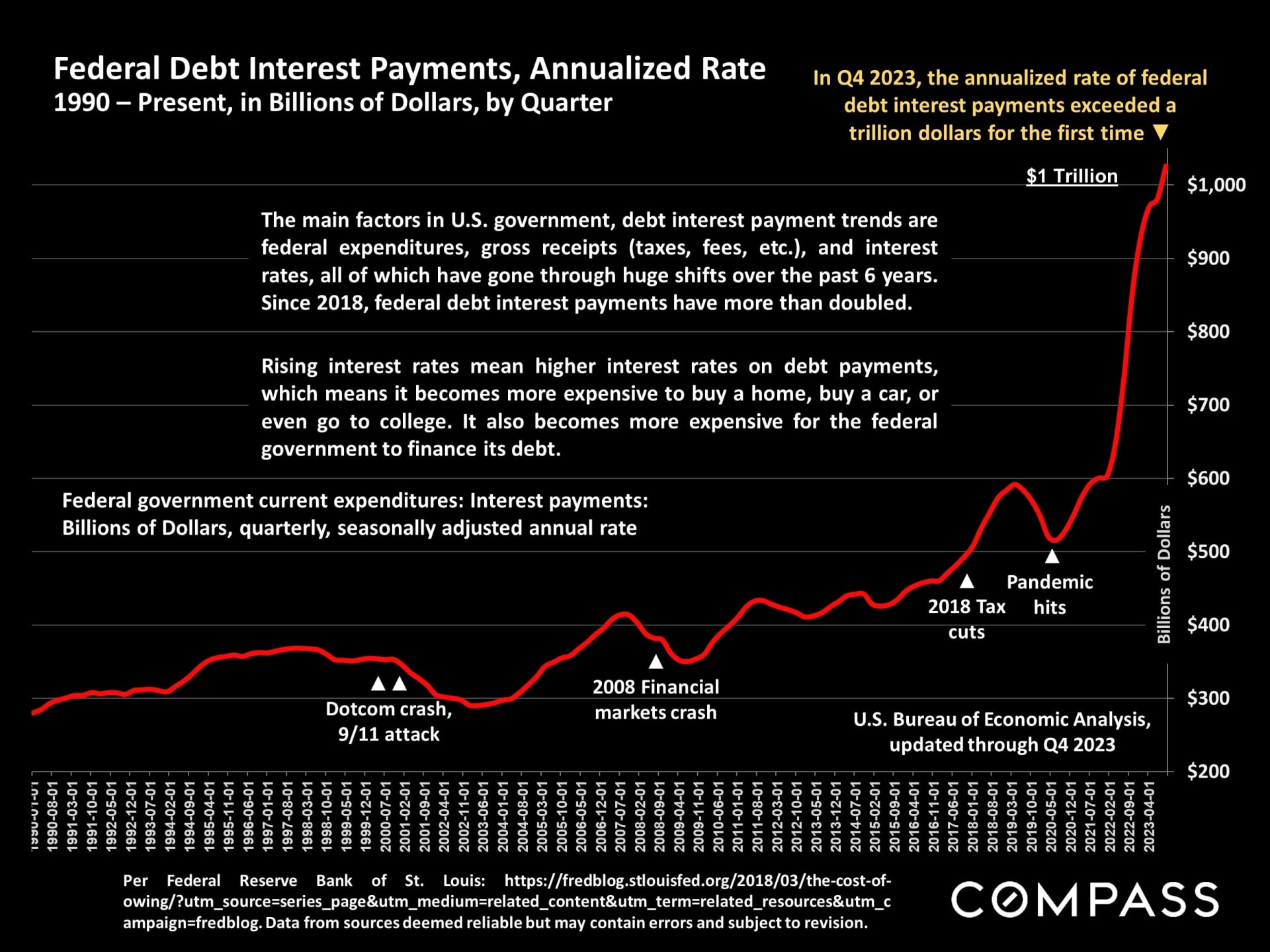

A somewhat terrifying trend in the annualized rate of federal debt interest payments: There are a number of negative issues pertinent to soaring national deficits and debt payments, some of which can, possibly, impact interest rates and real estate markets.

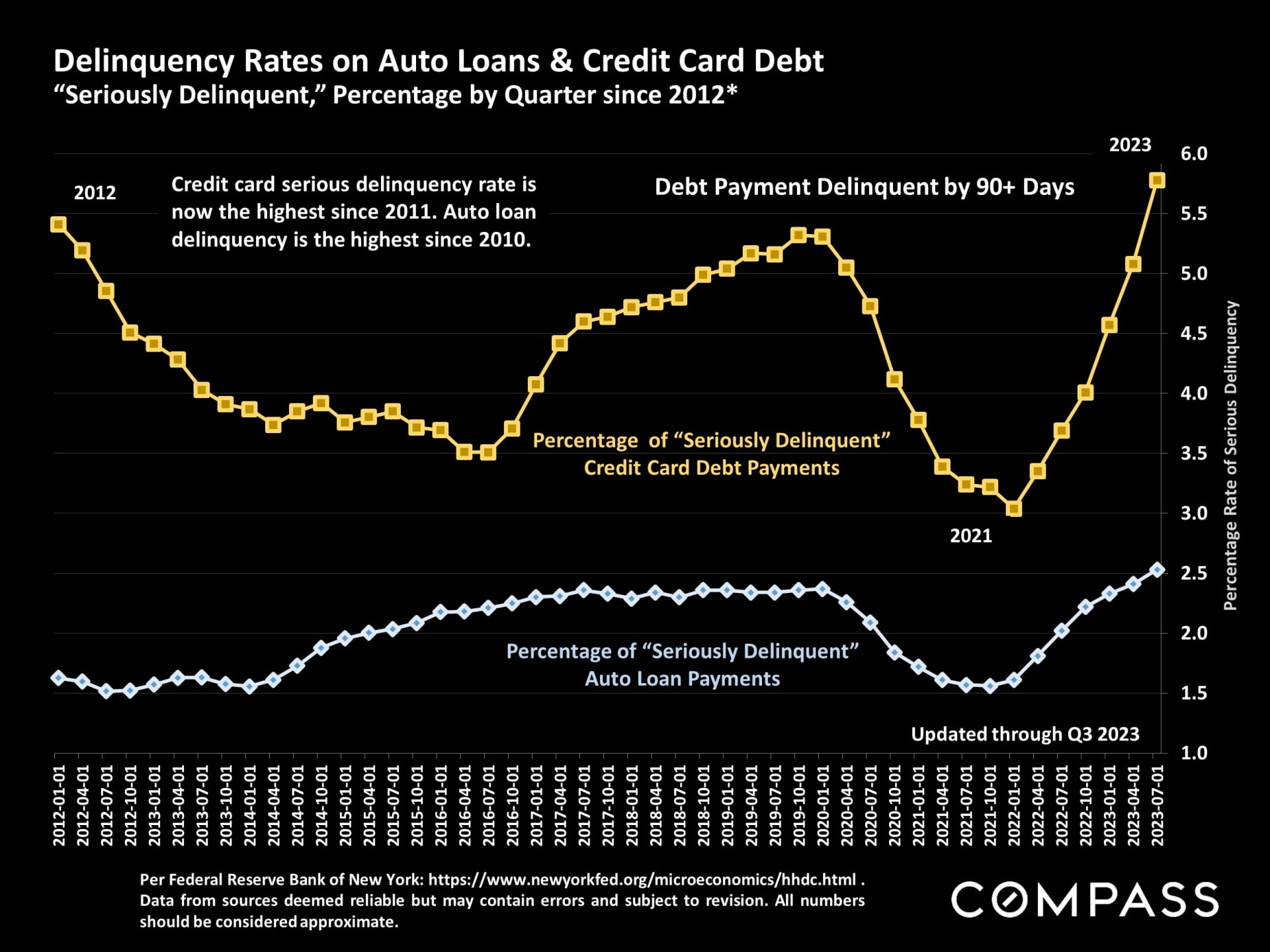

The increase in interest rates are also having increasingly unhealthy effects on consumer credit: Serious delinquency rates are the highest since the great recession, and appear to be heading higher.

A somewhat terrifying trend in the annualized rate of federal debt interest payments: There are a number of negative issues pertinent to soaring national deficits and debt payments, some of which can, possibly, impact interest rates and real estate markets.

The increase in interest rates are also having increasingly unhealthy effects on consumer credit: Serious delinquency rates are the highest since the great recession, and appear to be heading higher.