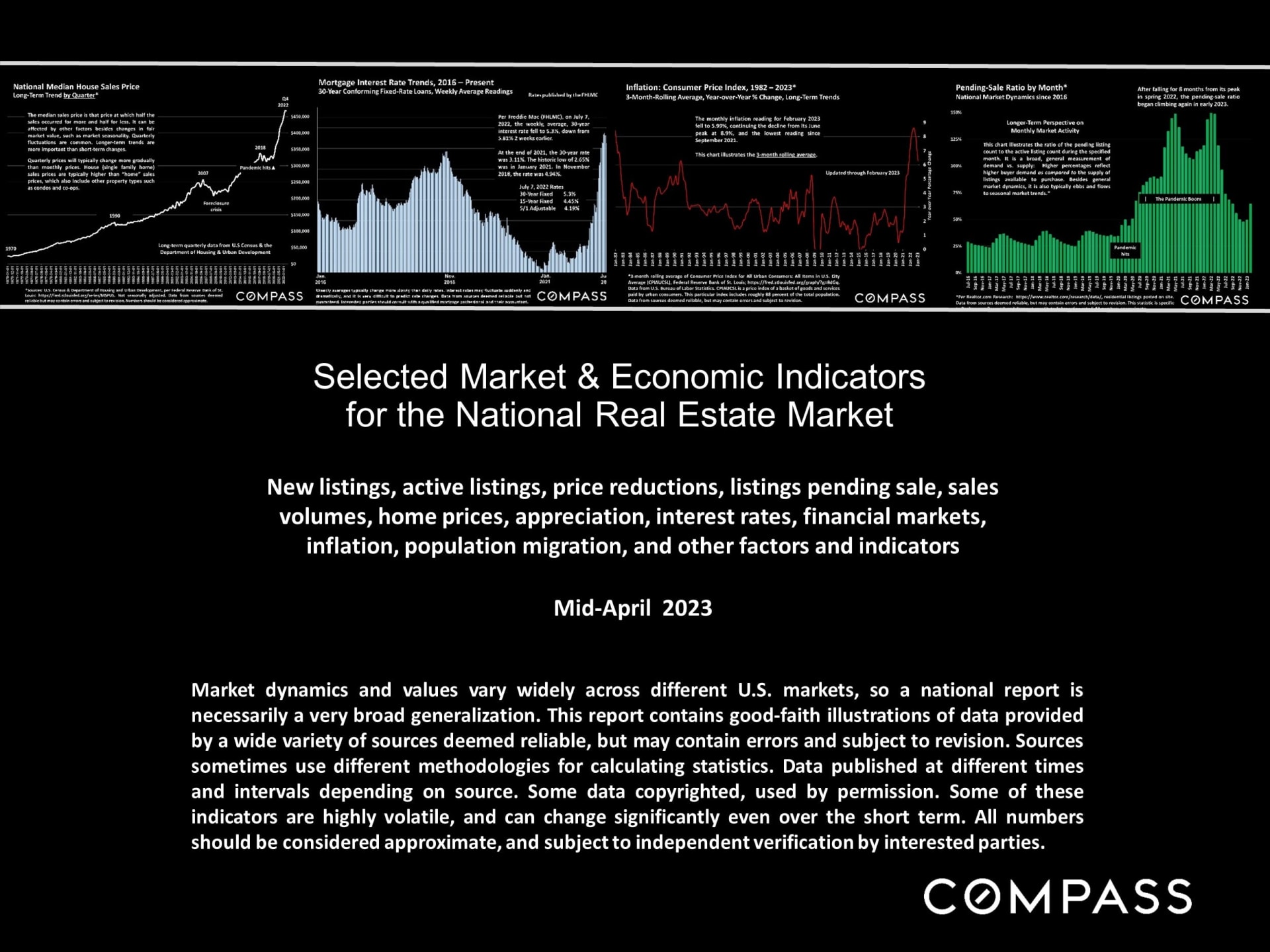

Selected Market & Economic Indicators for the National Real Estate Market

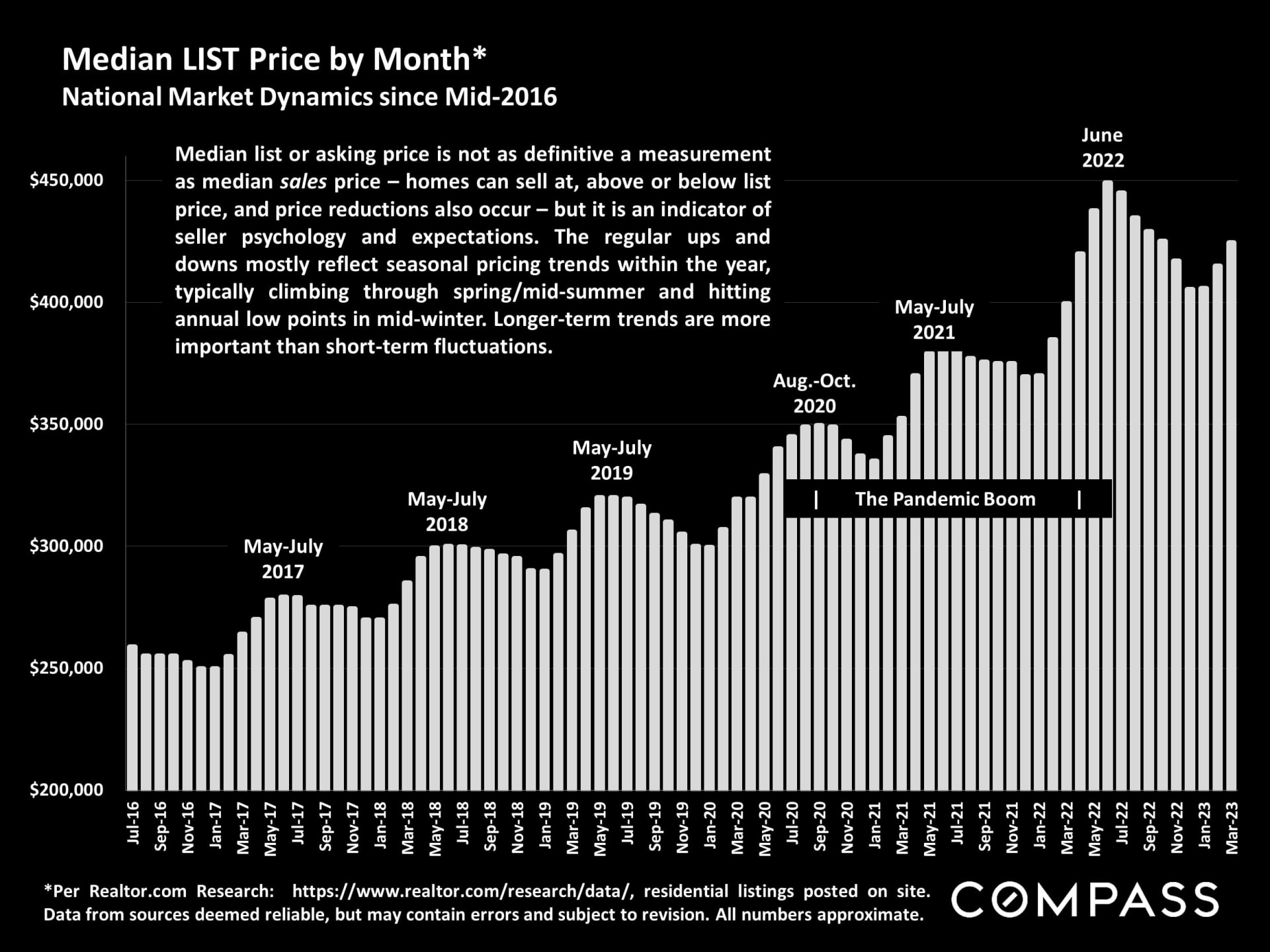

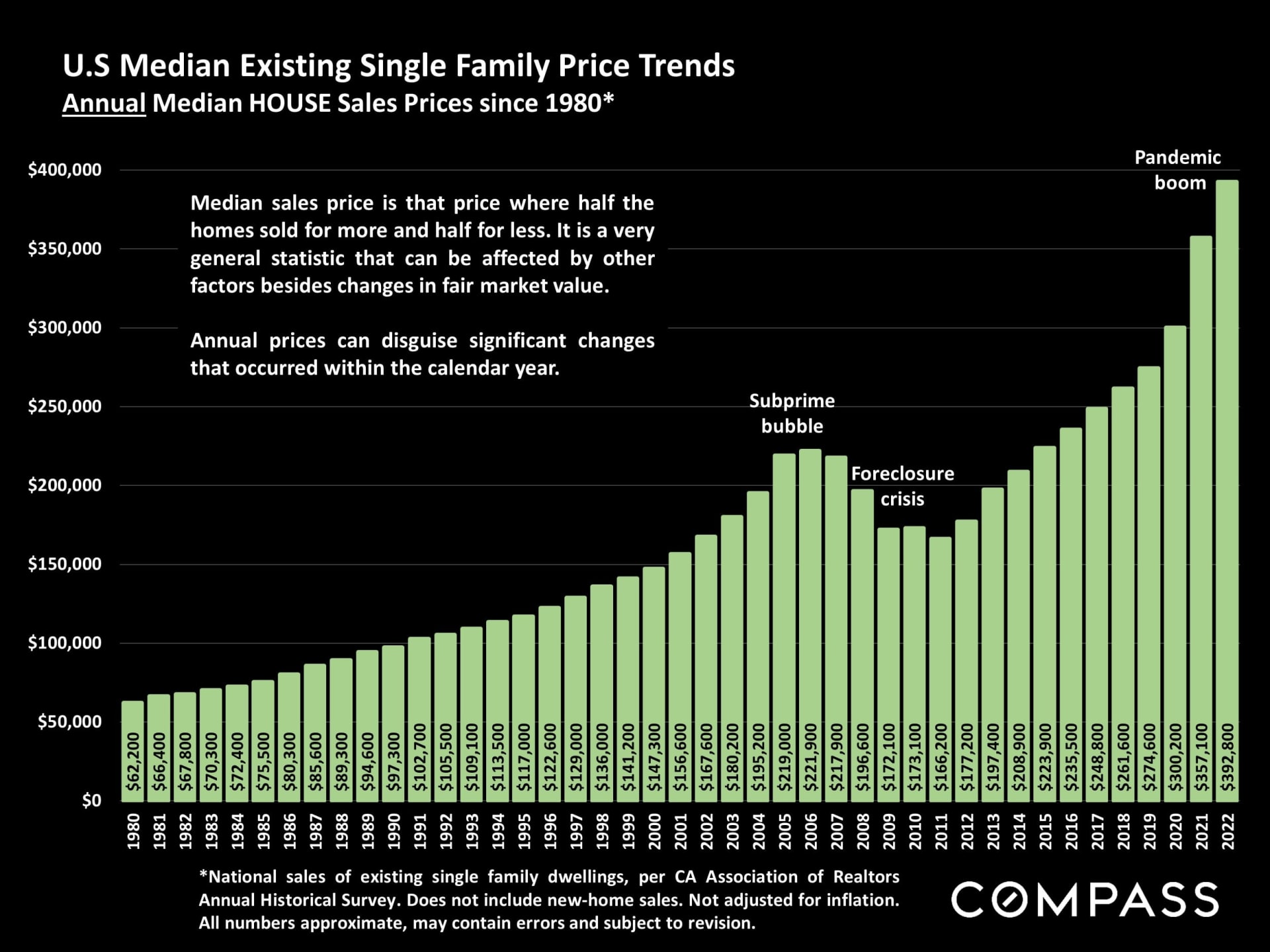

New listings, active listings, price reductions, listings pending sale, sales

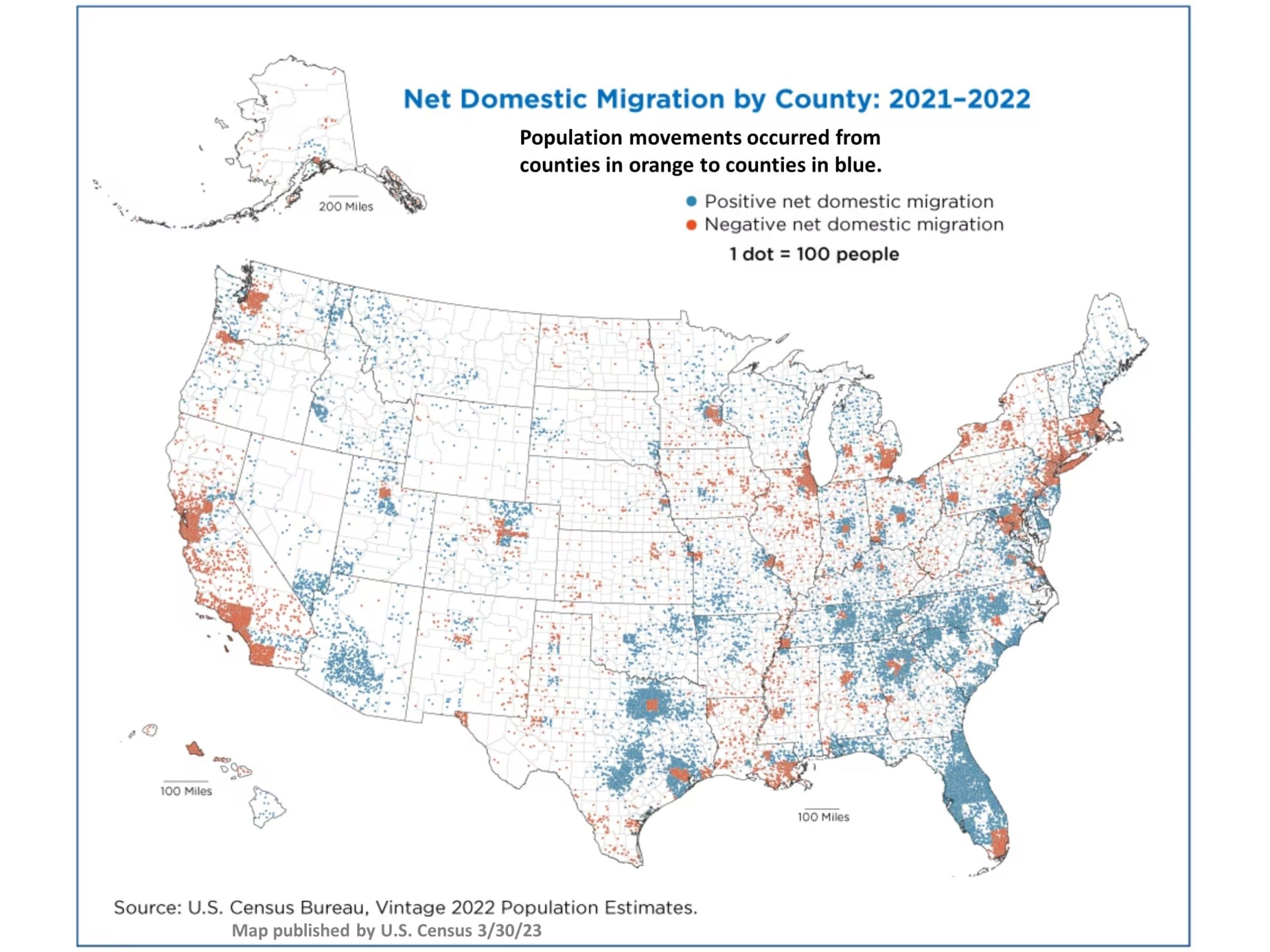

volumes, home prices, appreciation, interest rates, financial markets,

inflation, population migration, and other factors and indicators

Mid-April 2023

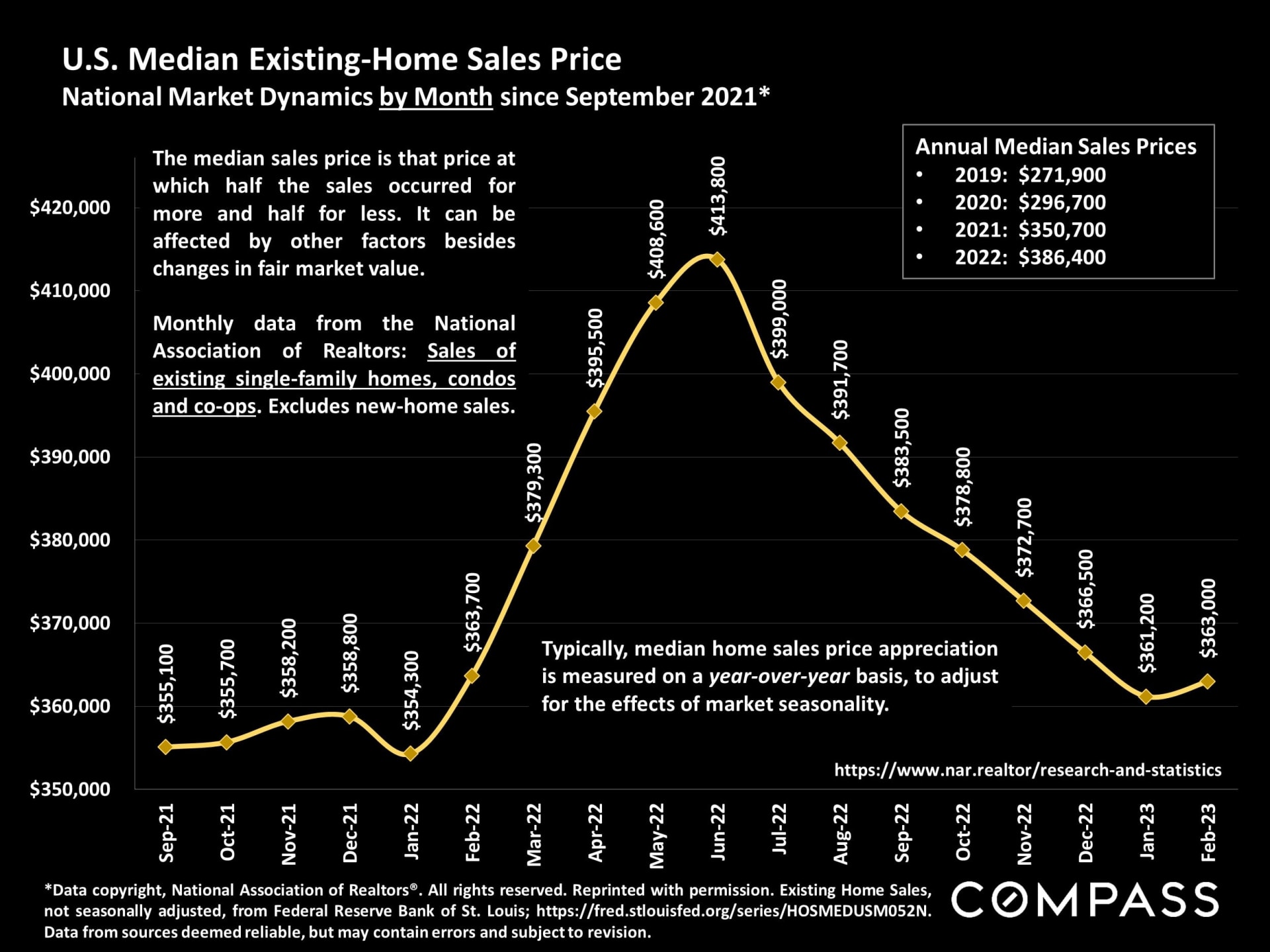

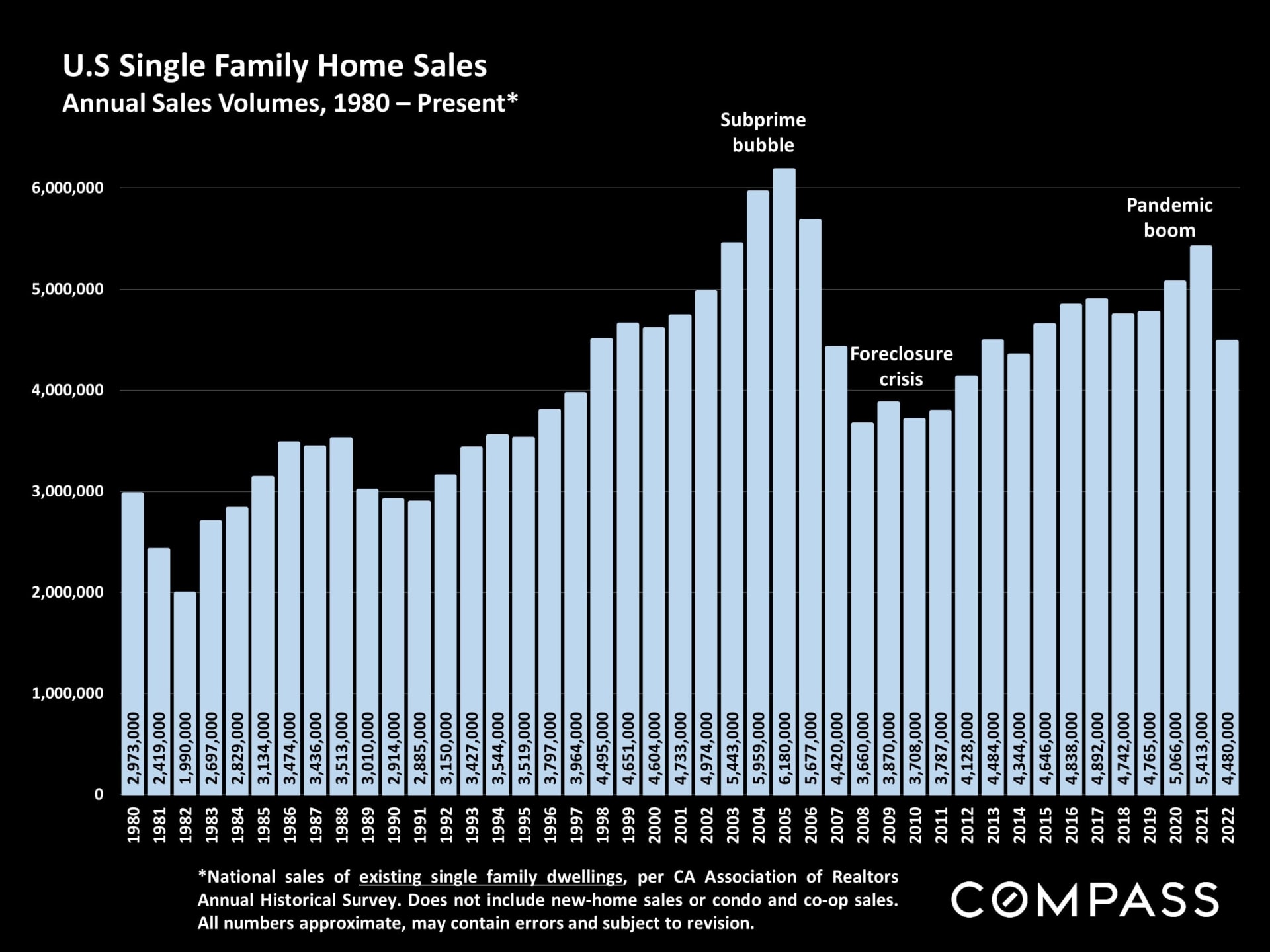

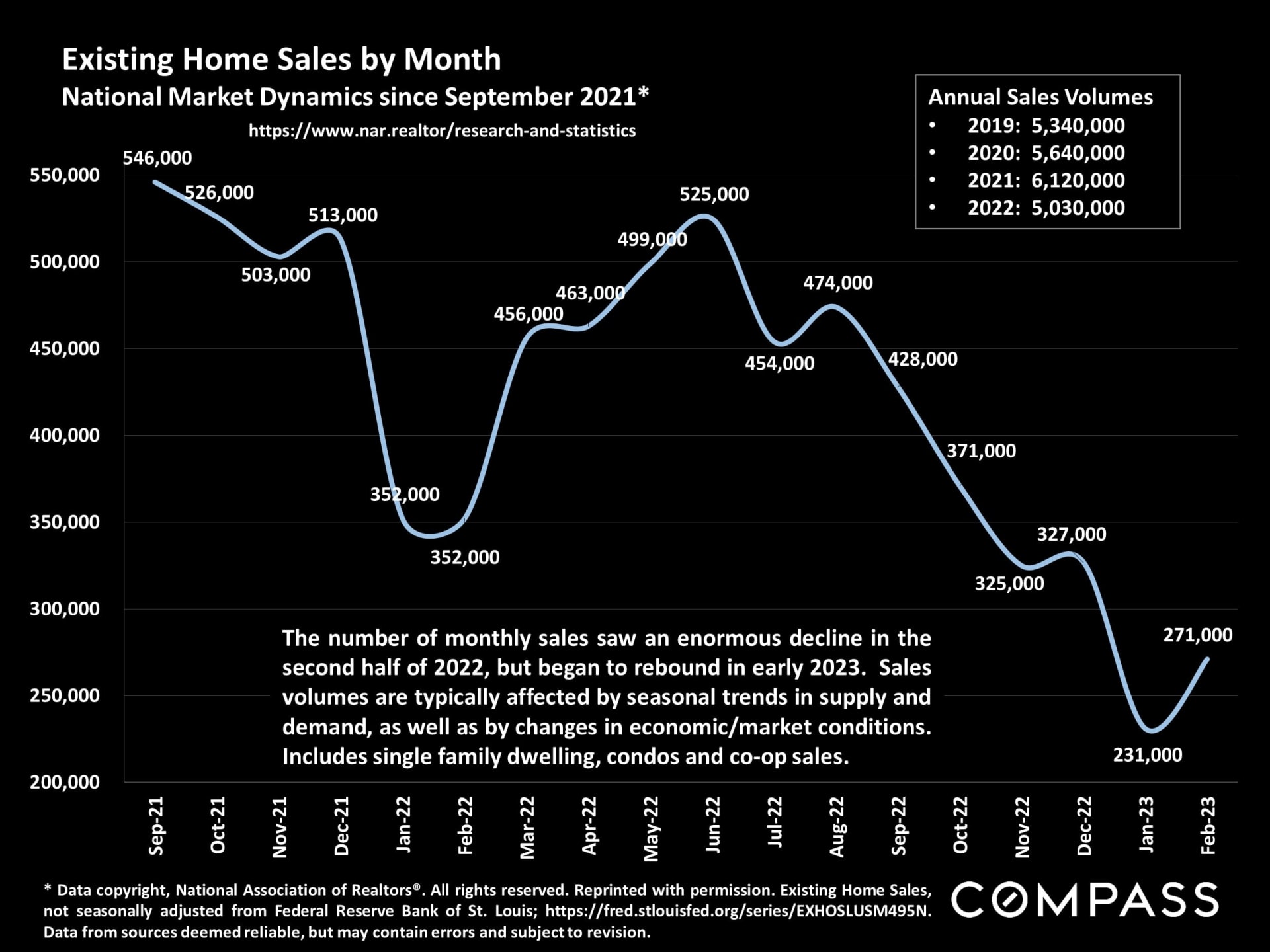

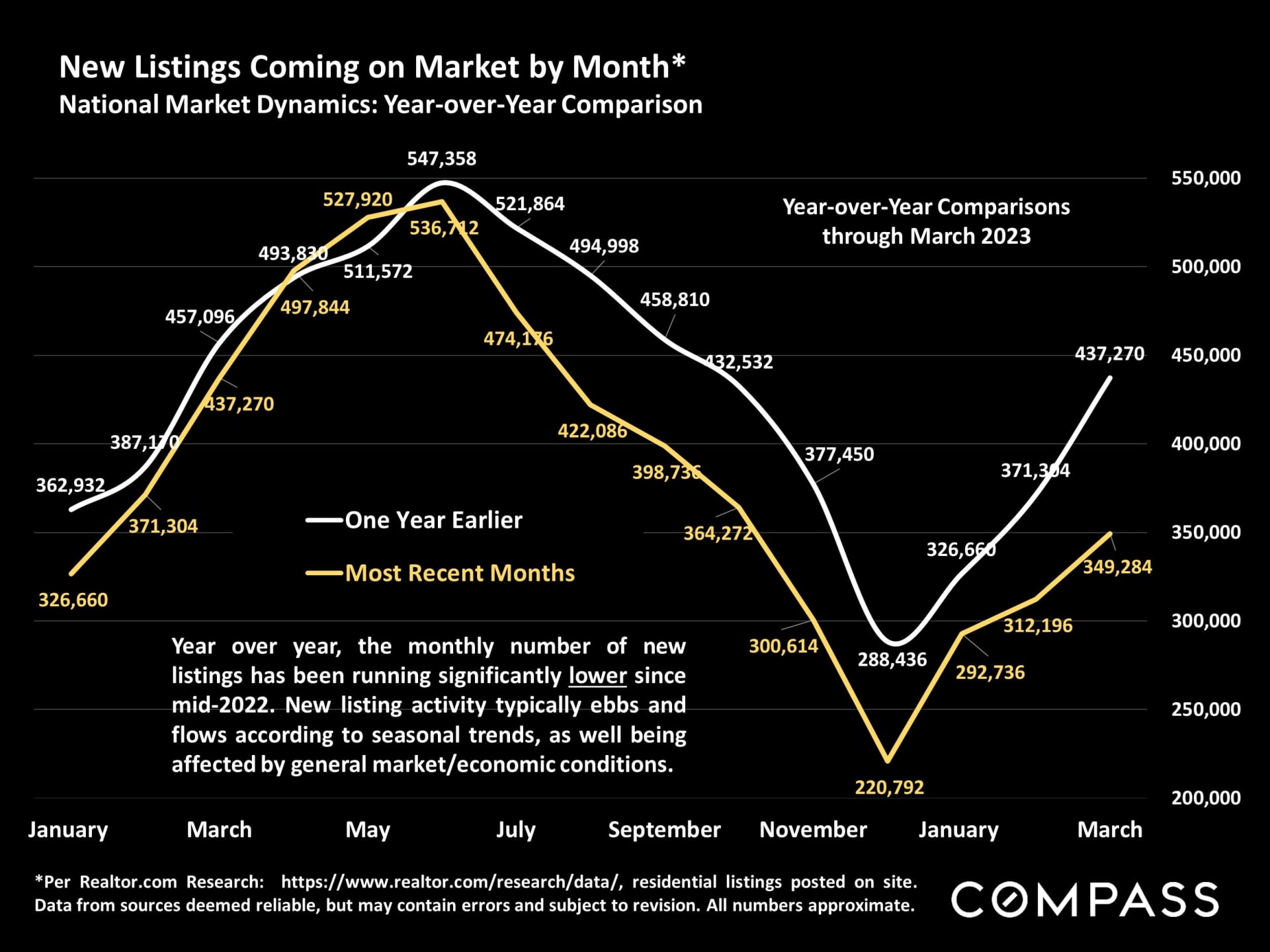

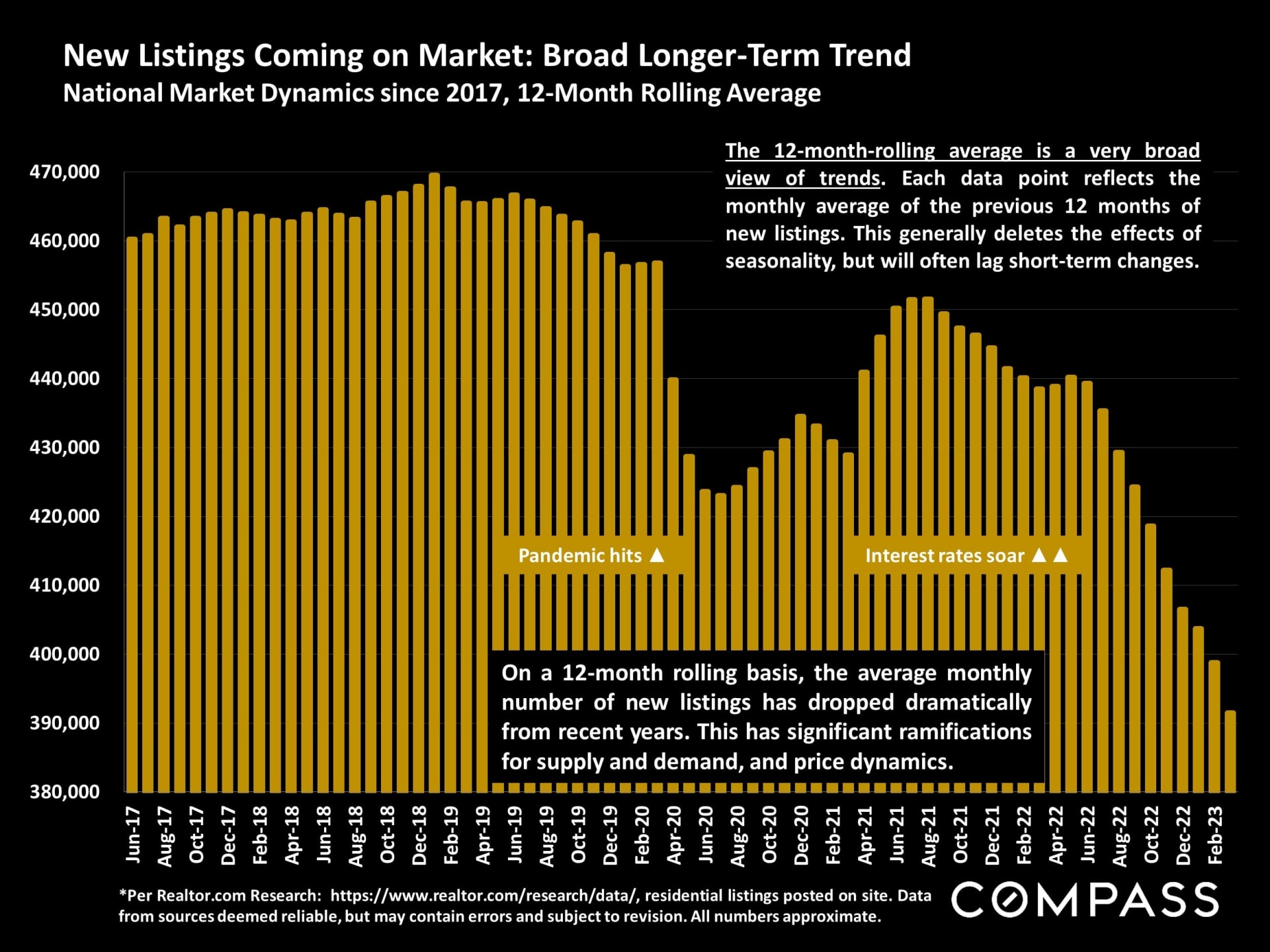

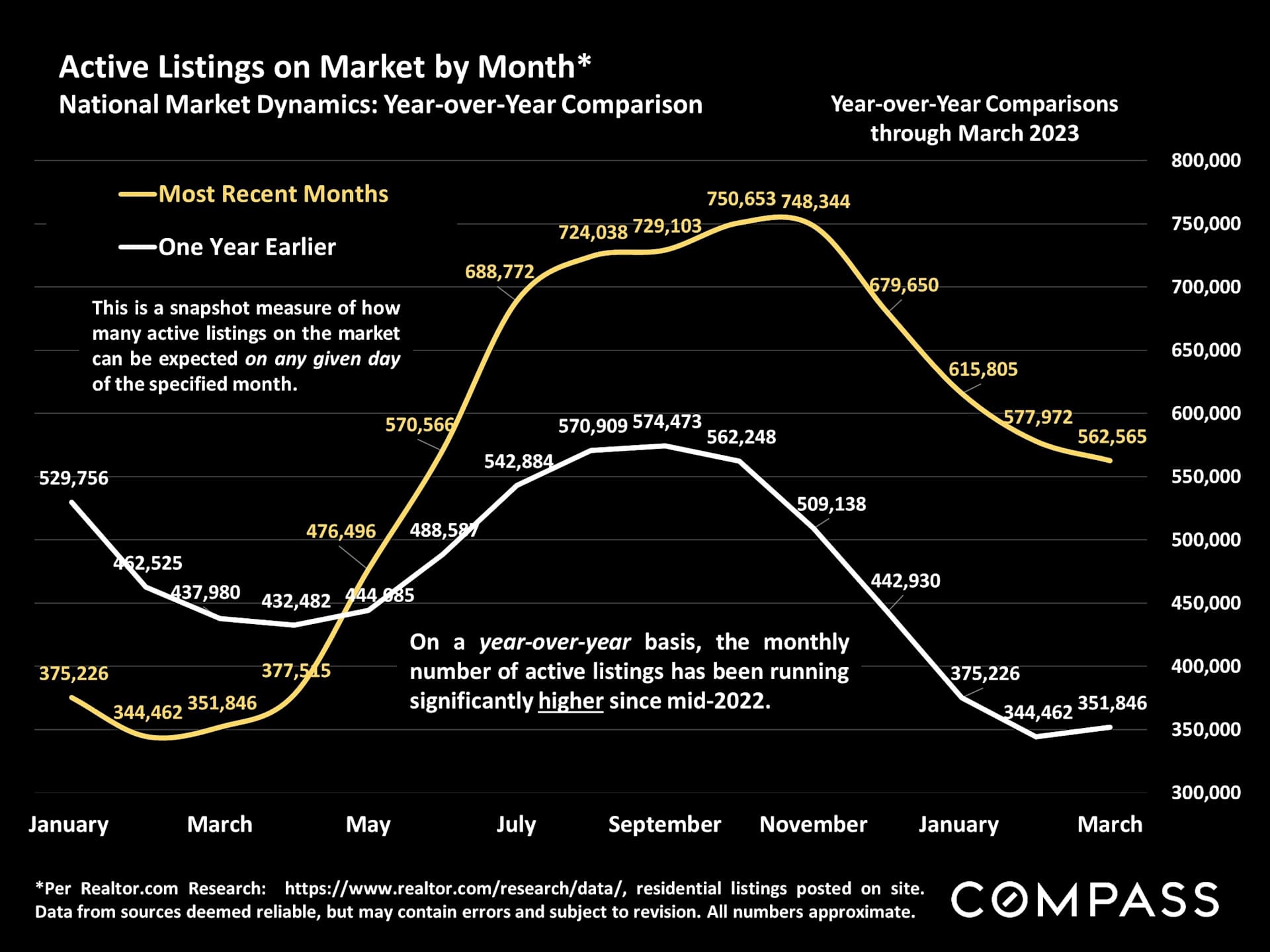

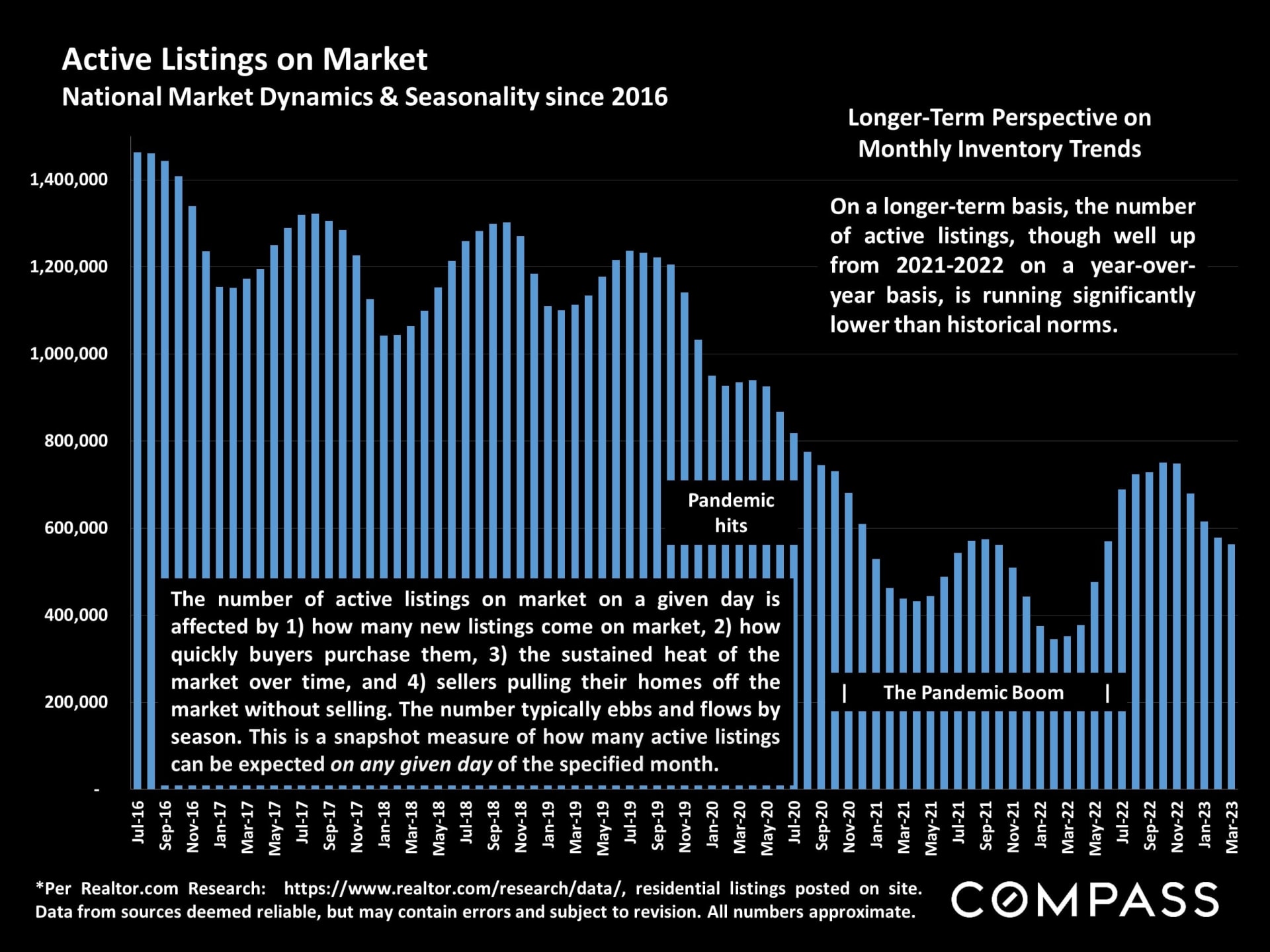

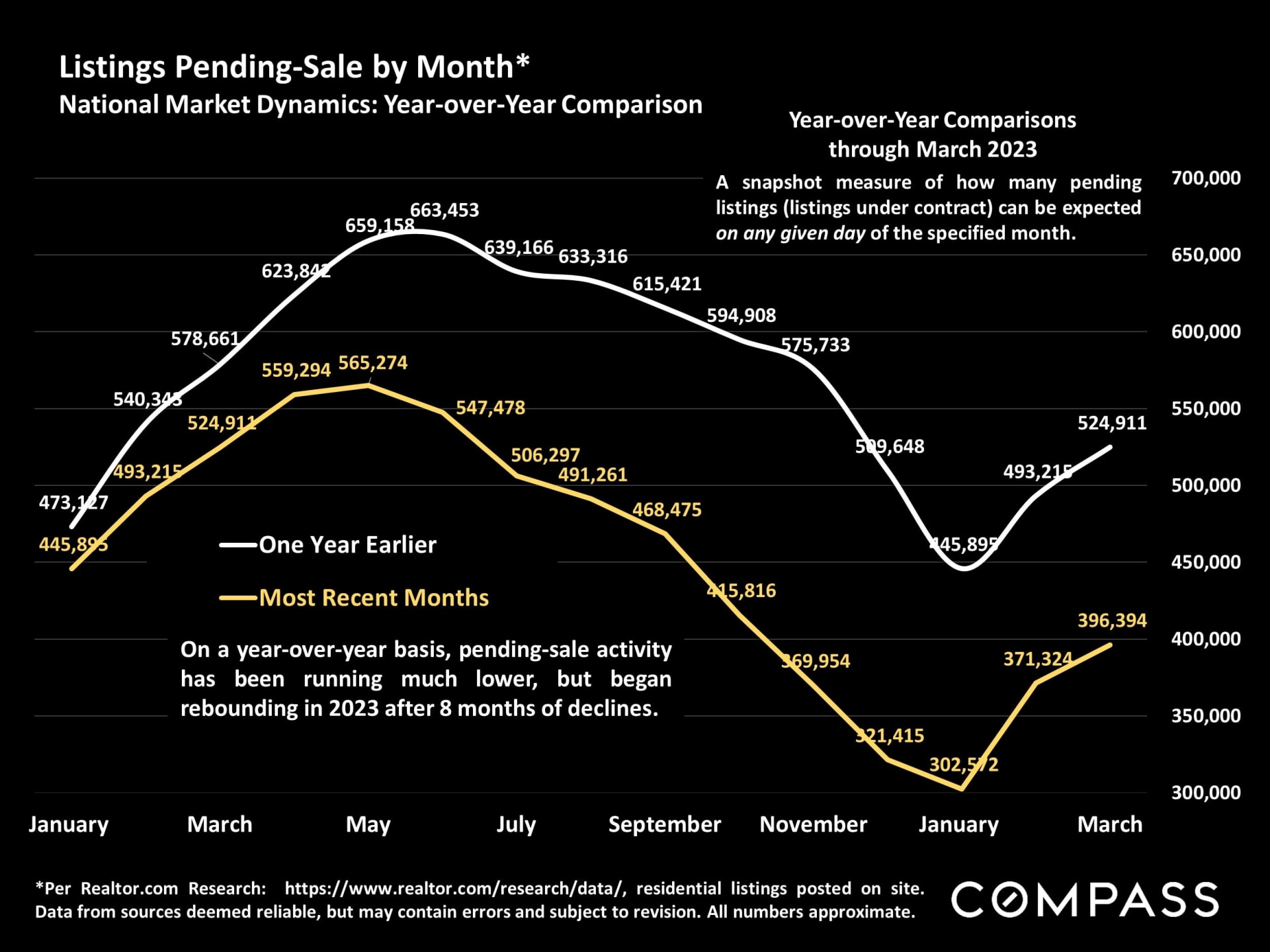

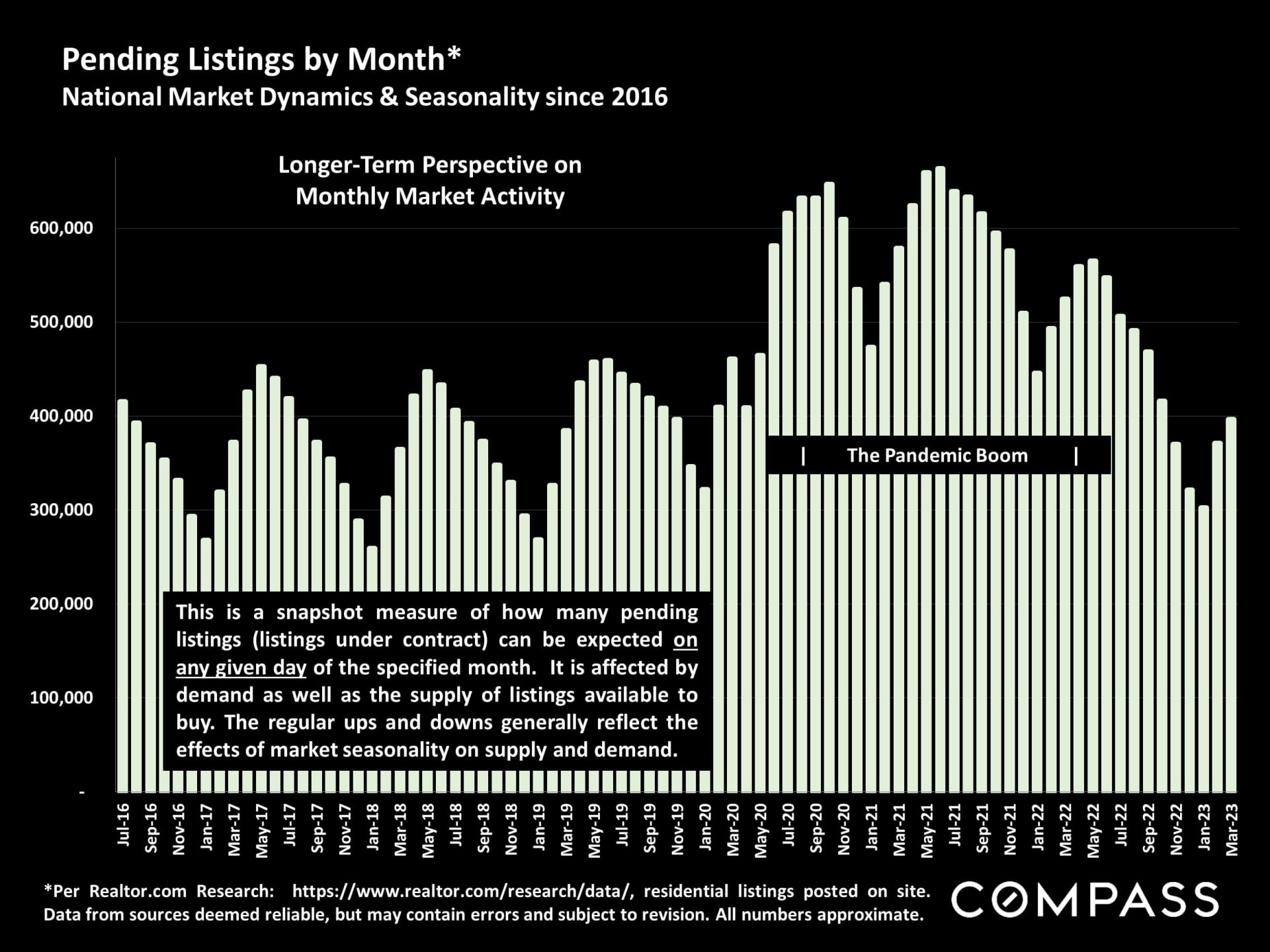

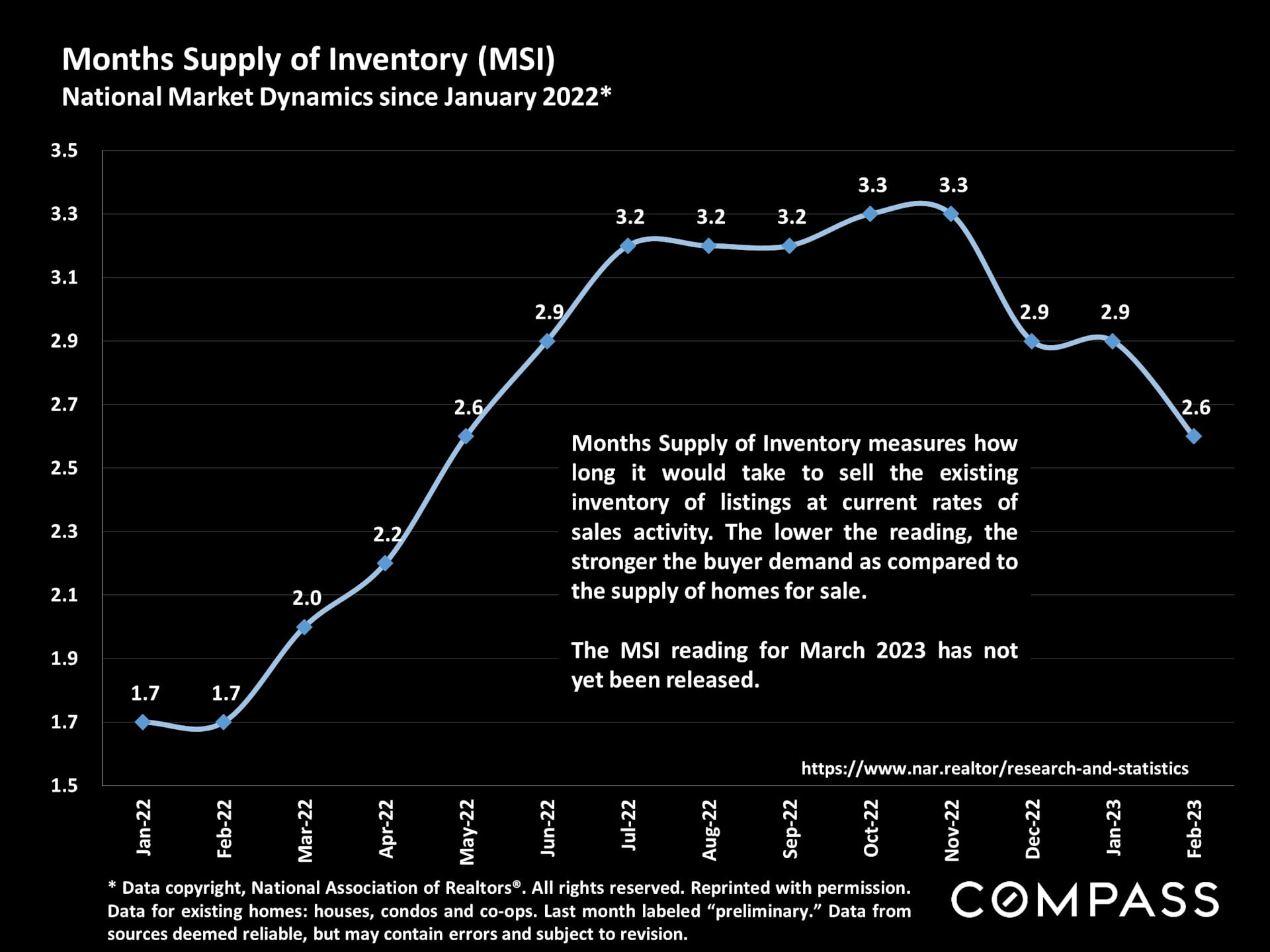

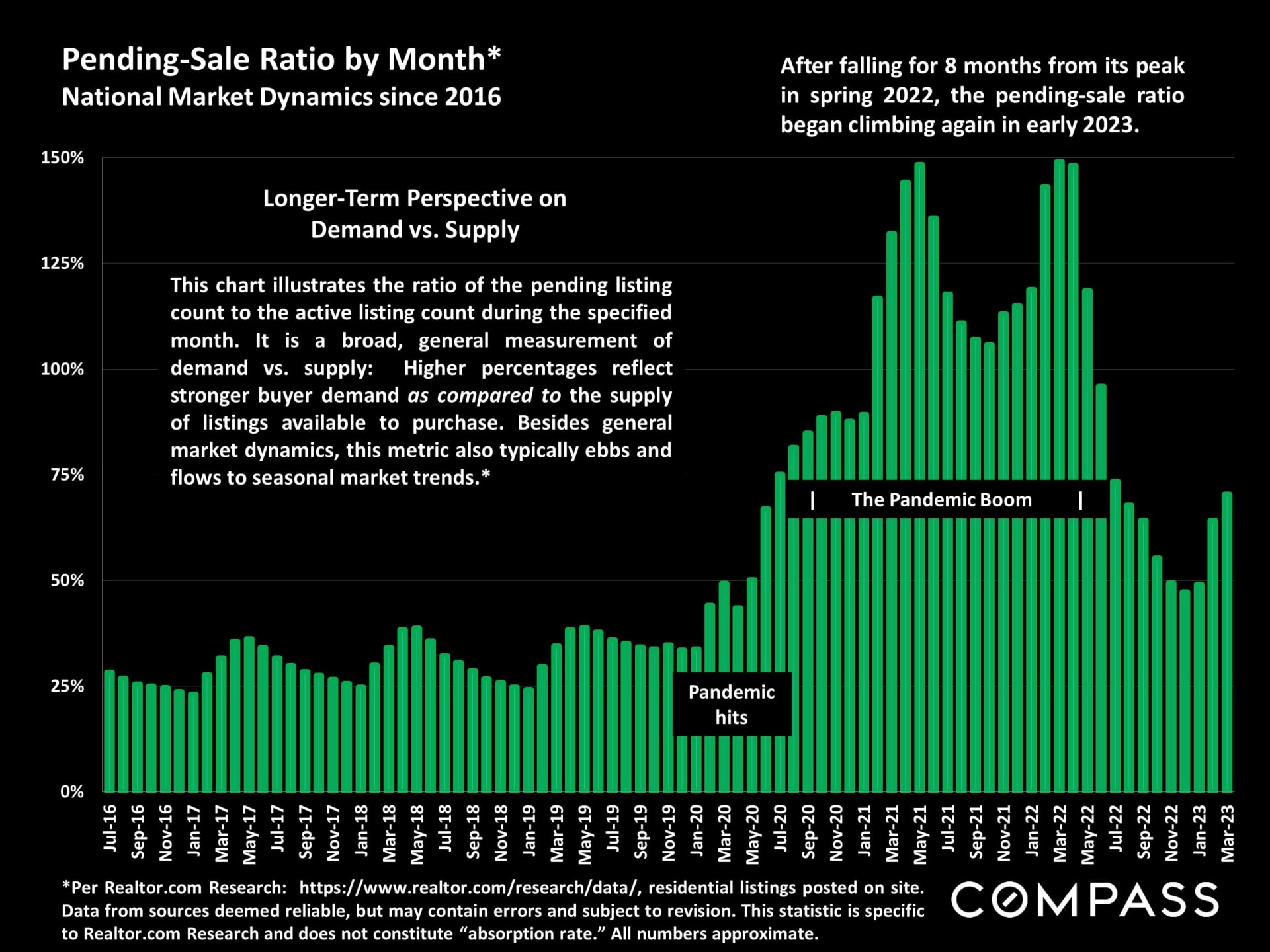

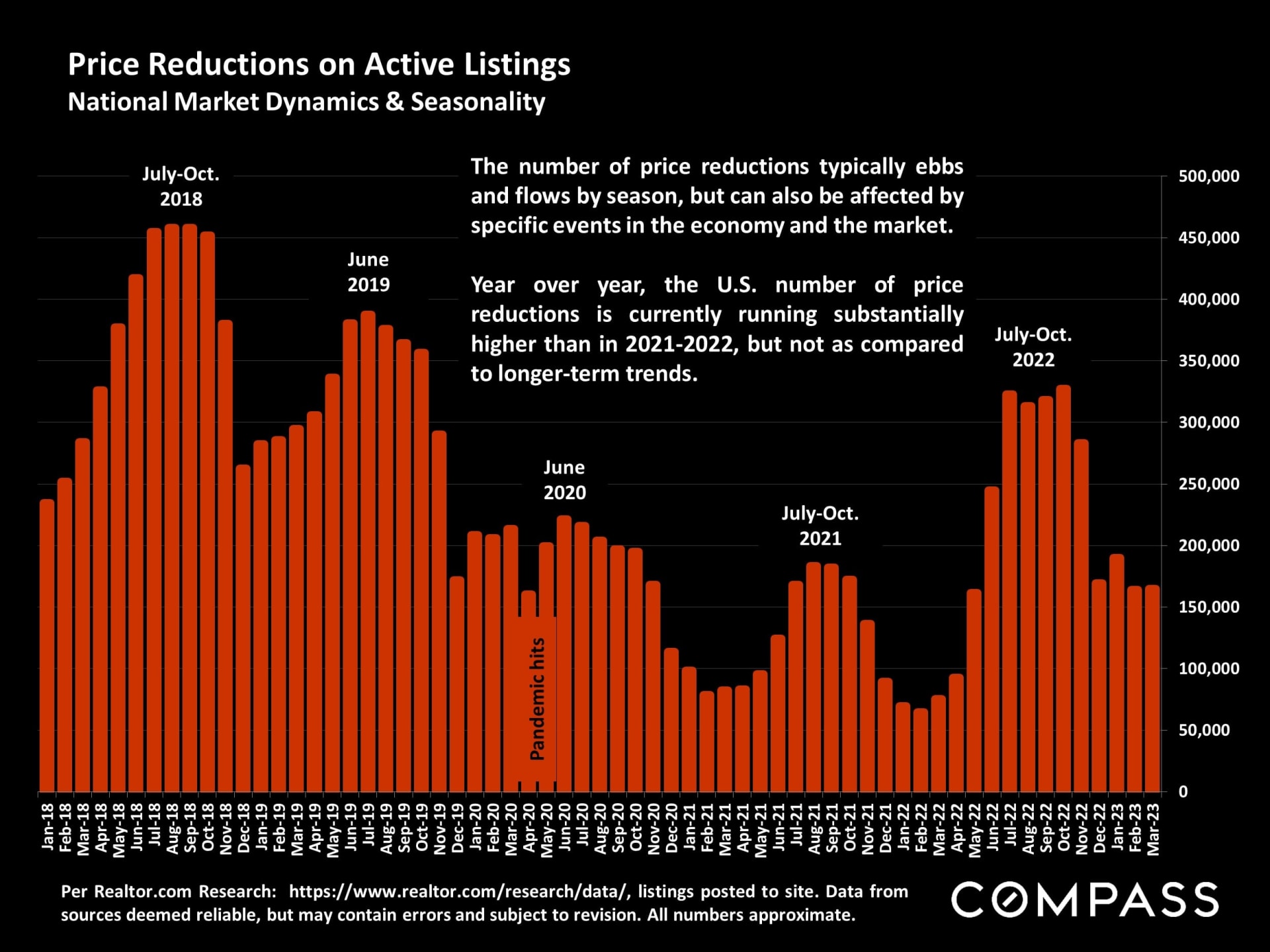

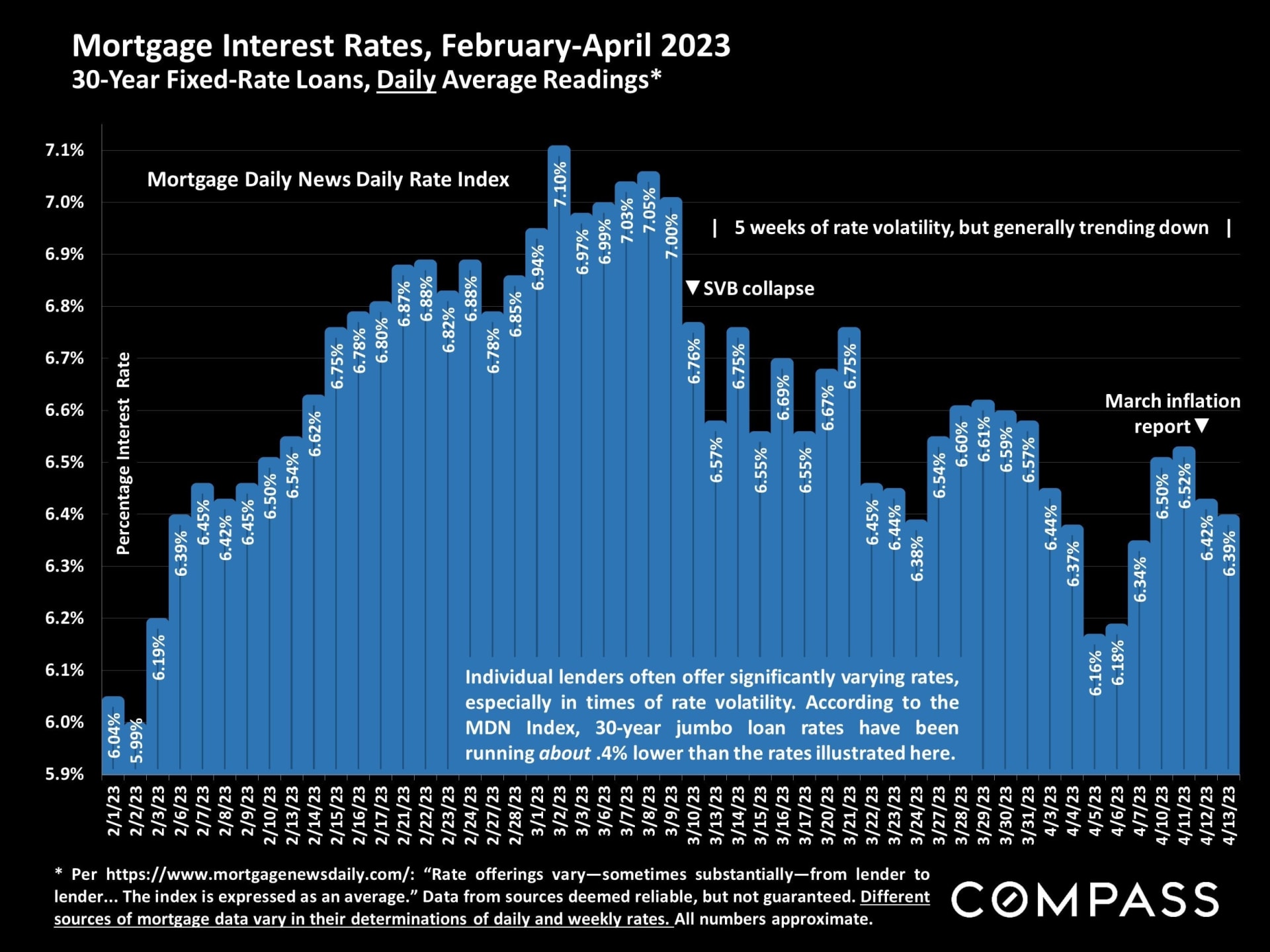

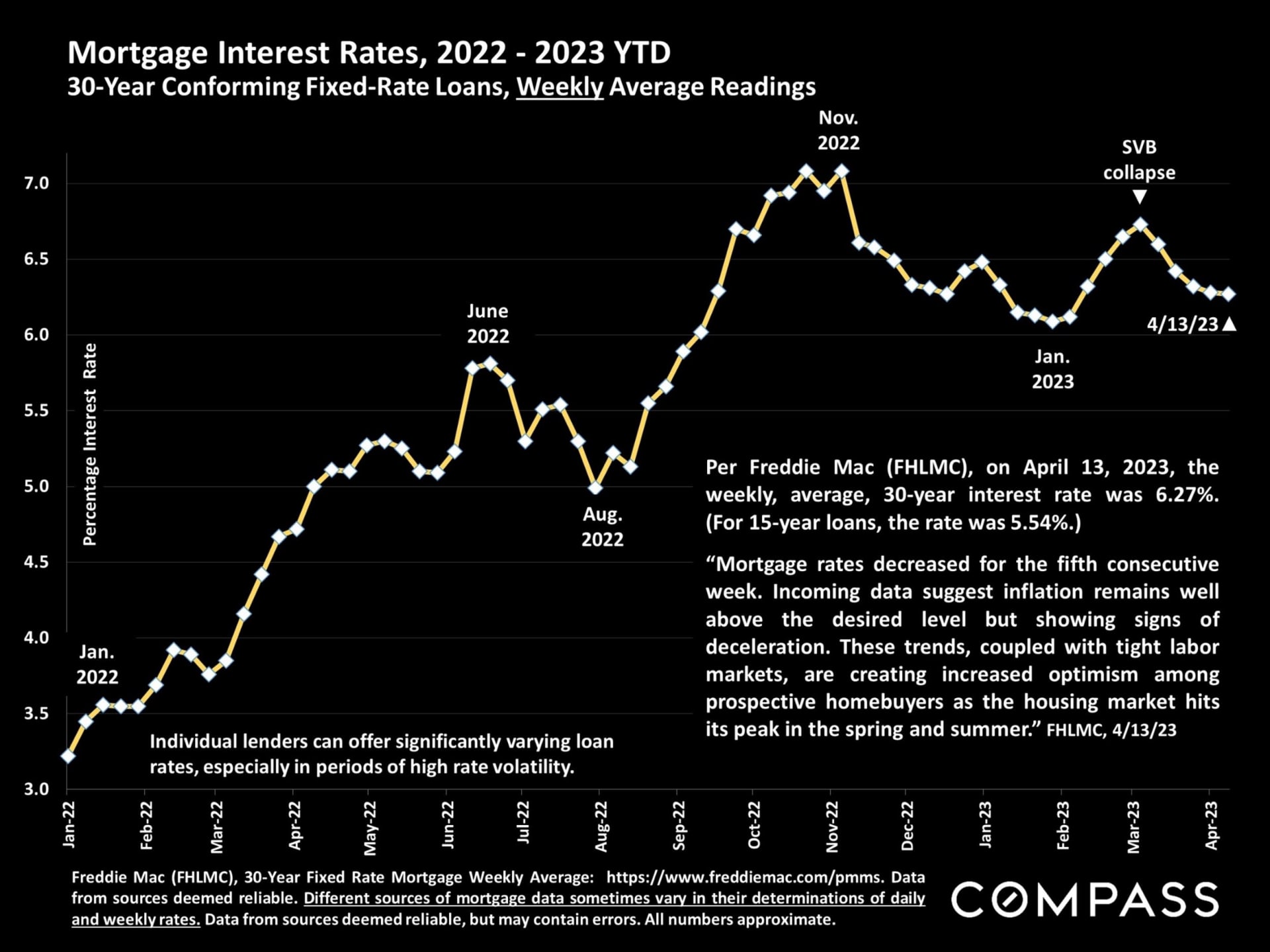

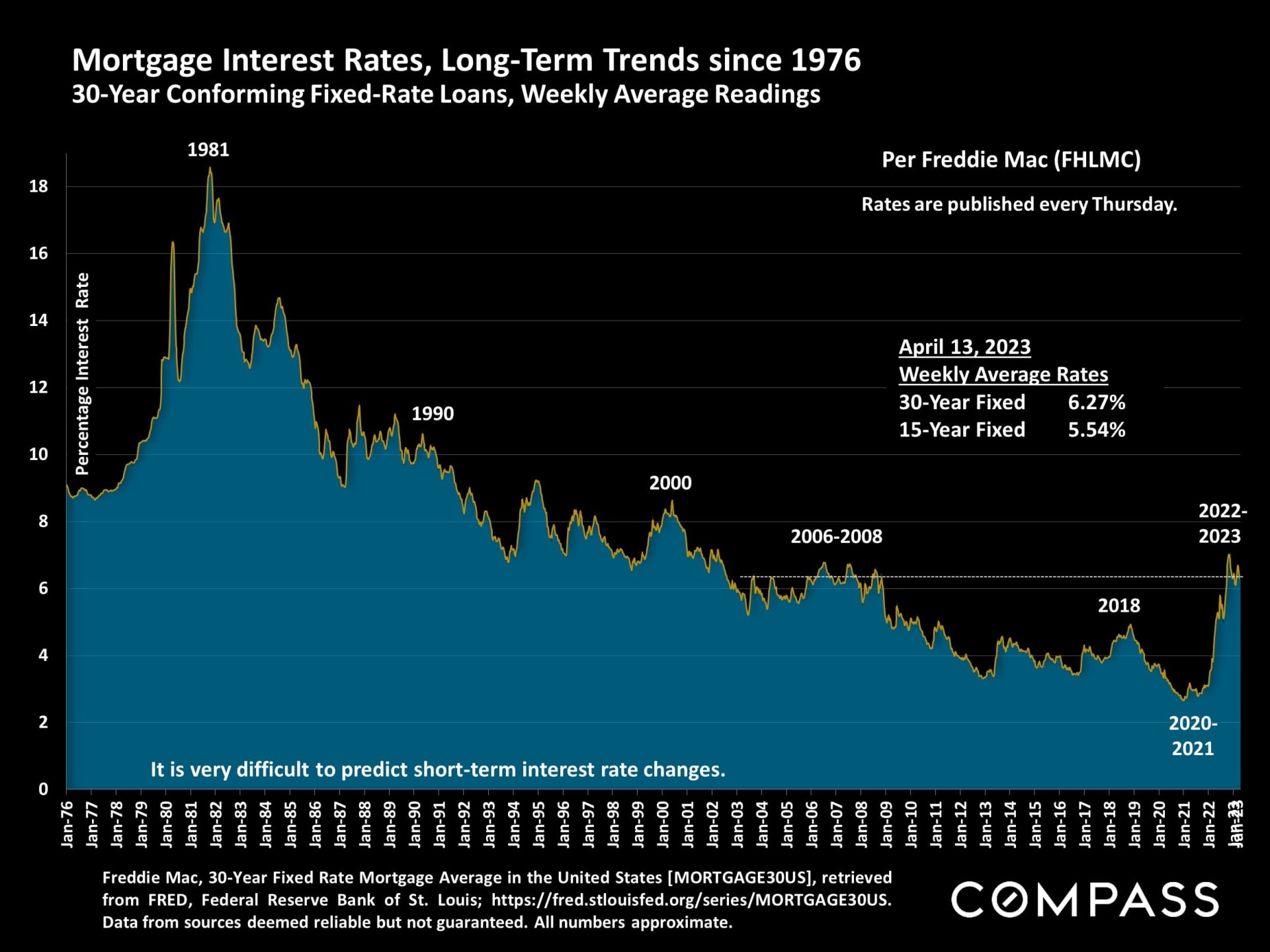

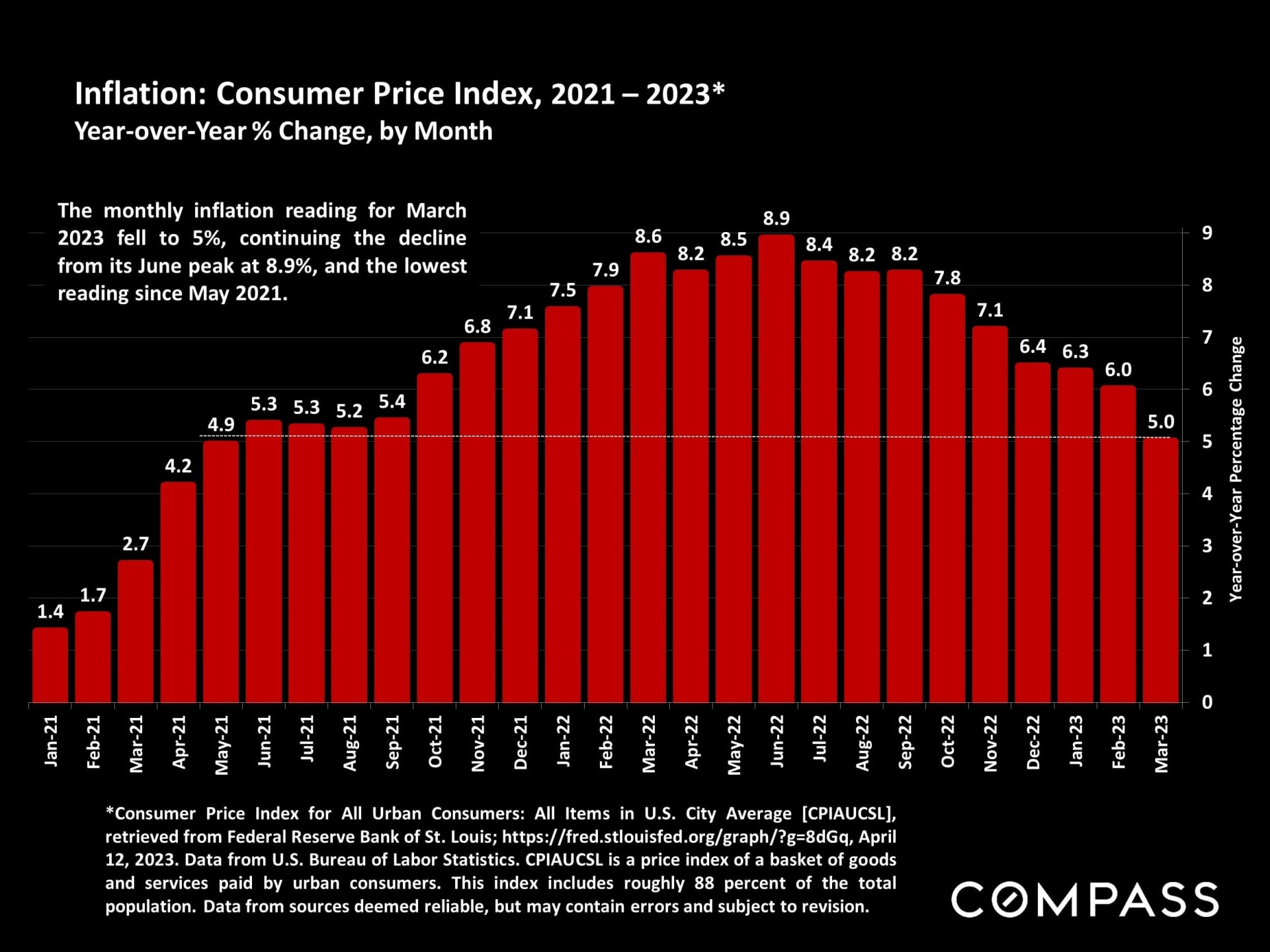

Buyer demand and market activity continued to rebound in early 2023 from the late 2022

low point, but the number of new listings coming on market remains very low, a situation

with wide ramifications for supply and demand dynamics, and for home prices. Many

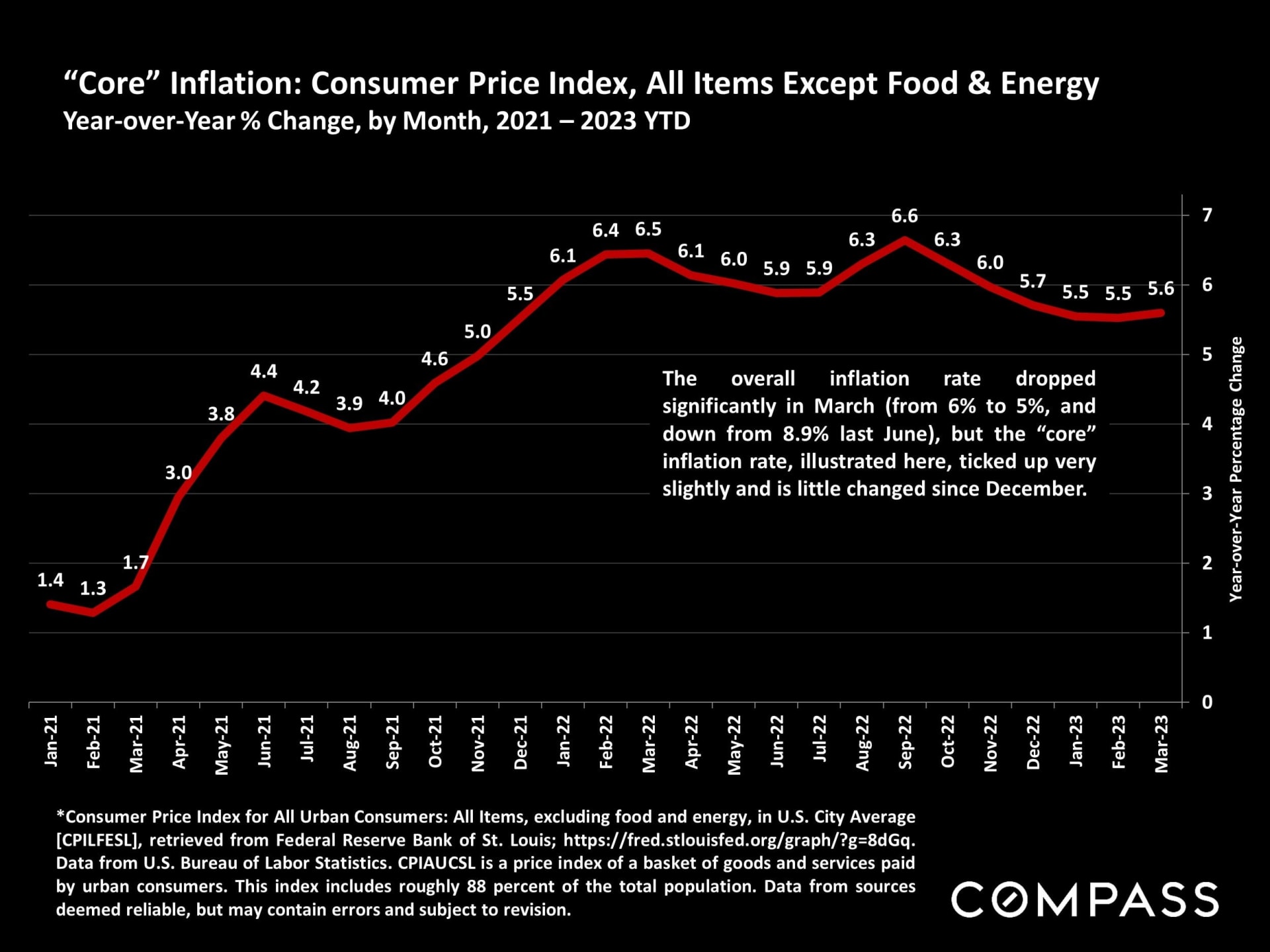

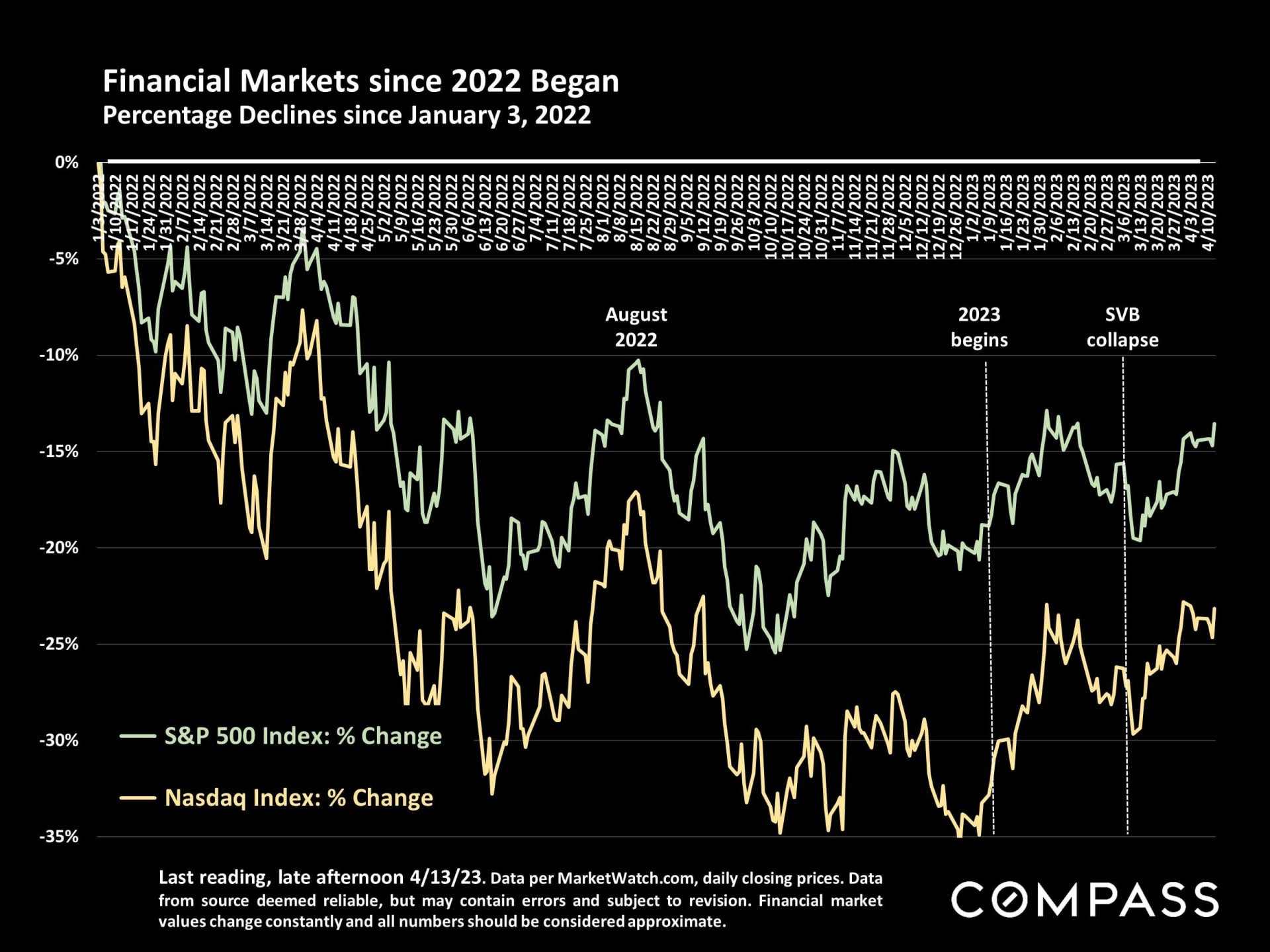

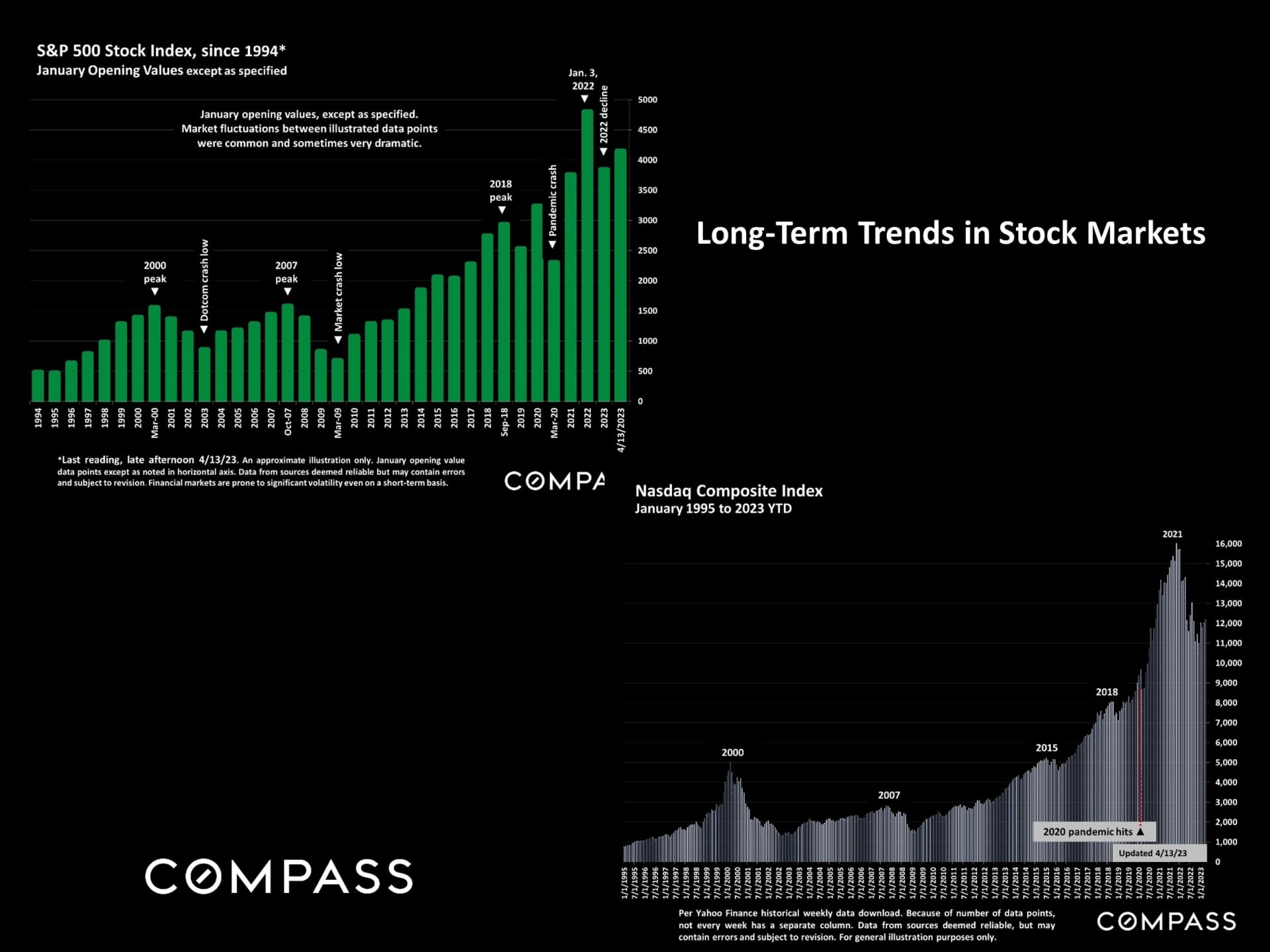

important economic factors at play – such as interest rates, inflation, financial markets,

the stability of the banking industry, federal debt limit negotiations, and so on – continue

to be uncertain and/or volatile.

This report is divided into two parts: The first looks at home prices, and supply and

demand conditions and trends in the overall national market. The second part reviews

selected macroeconomic factors and indicators that often impact real estate. A national

report is necessarily a huge generalization of broad trends across an enormous range of

regional submarkets, whose dynamics often vary. How the data in this report applies to

any particular property is unknown without a specific comparative market analysis.

As of the date of this report, depending on the source of data, some data points for

March 2023 and Q1 2023 may not be available for several weeks or longer, and will be

covered in future updates.

The spring selling season is typically the most active of the year – though this too can vary

between submarkets – and much more data will soon be available.