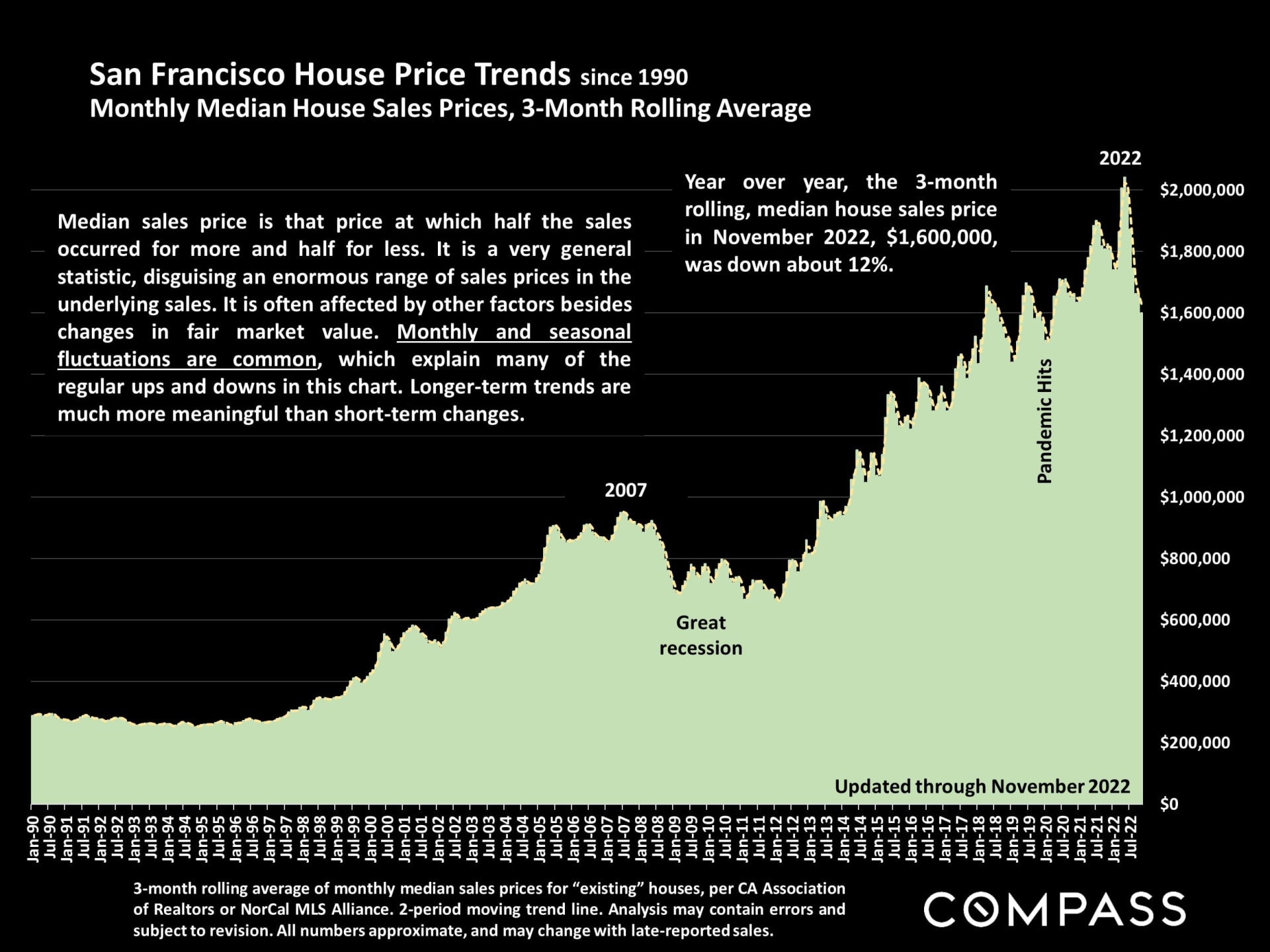

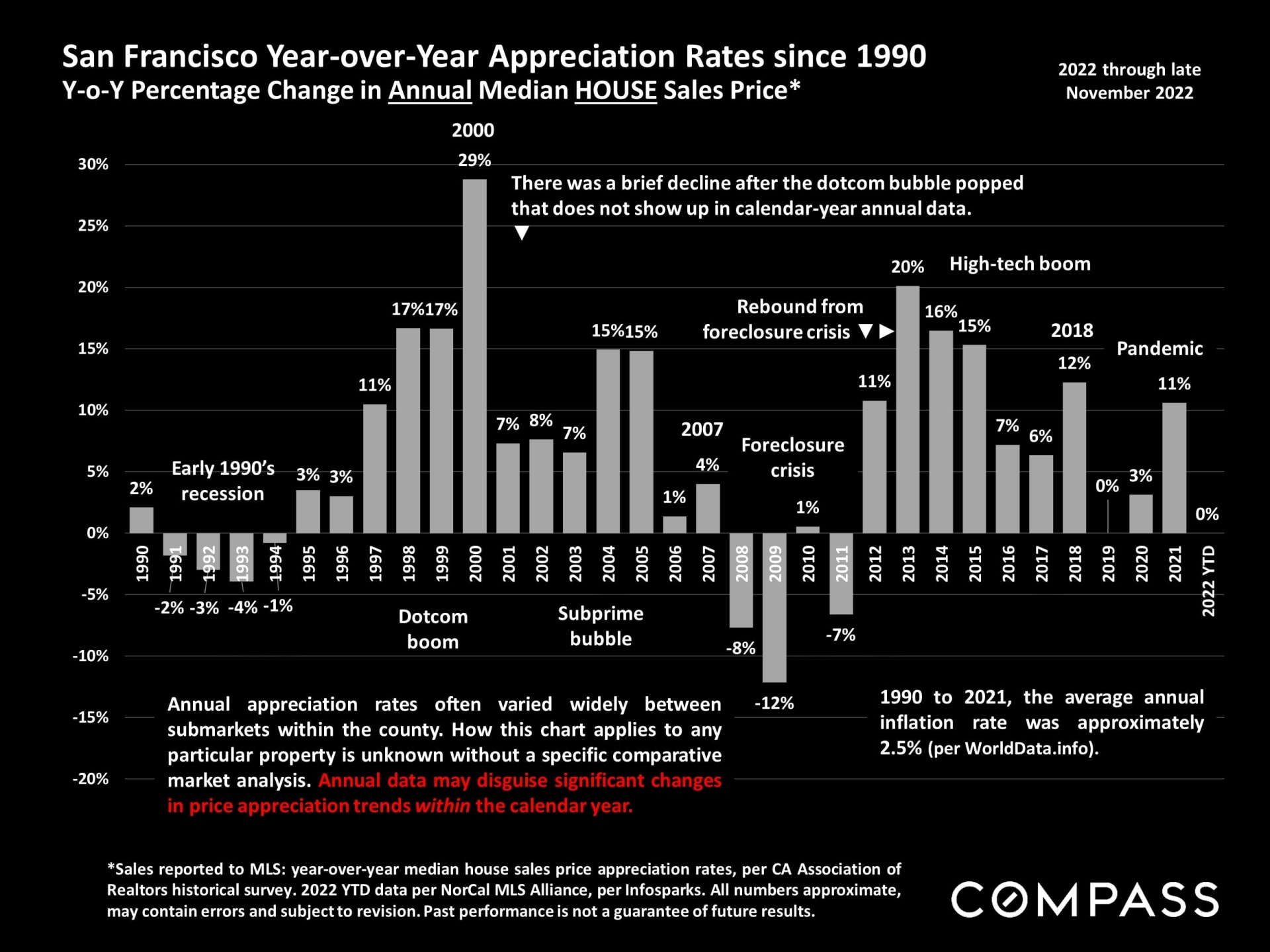

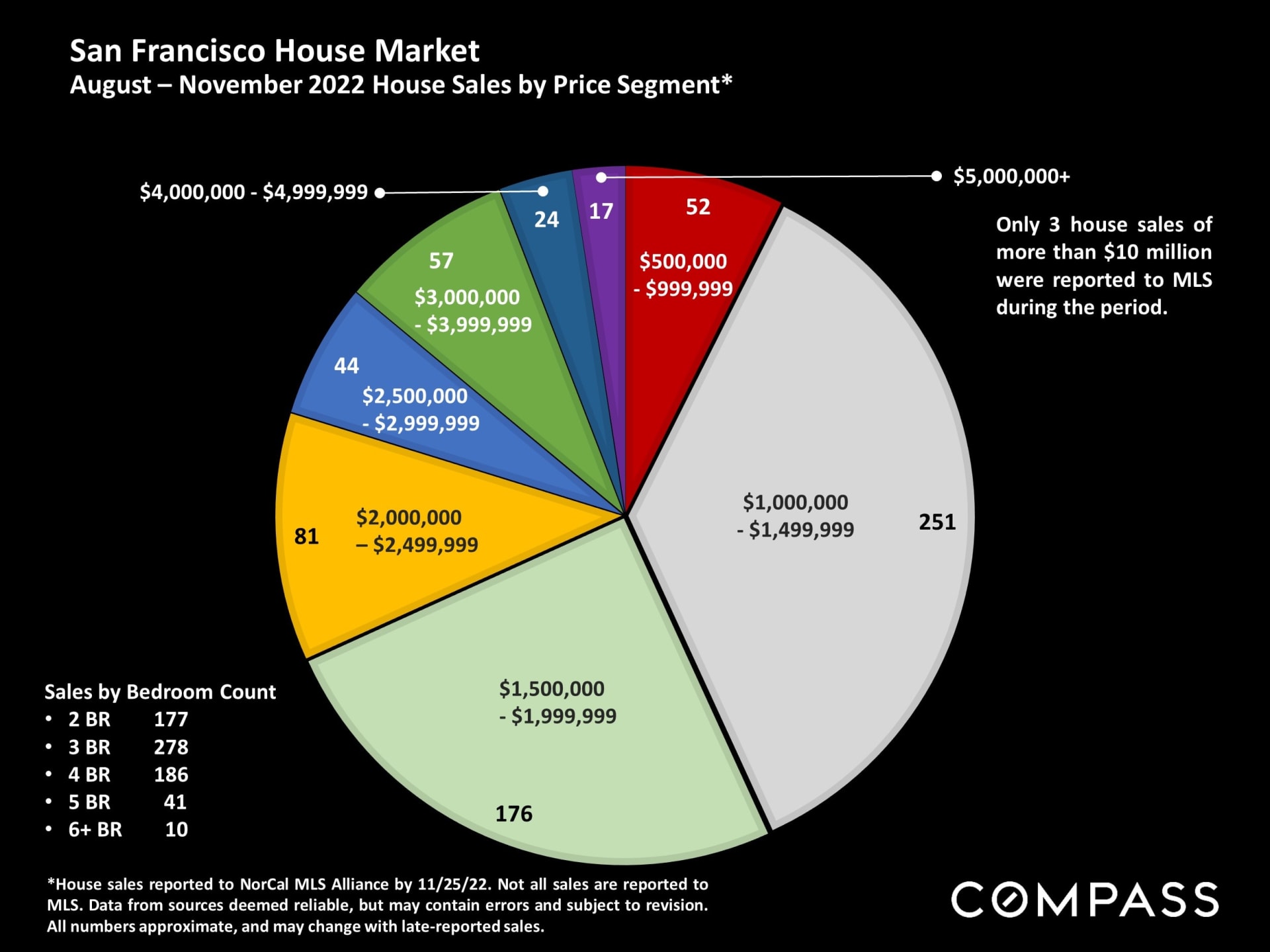

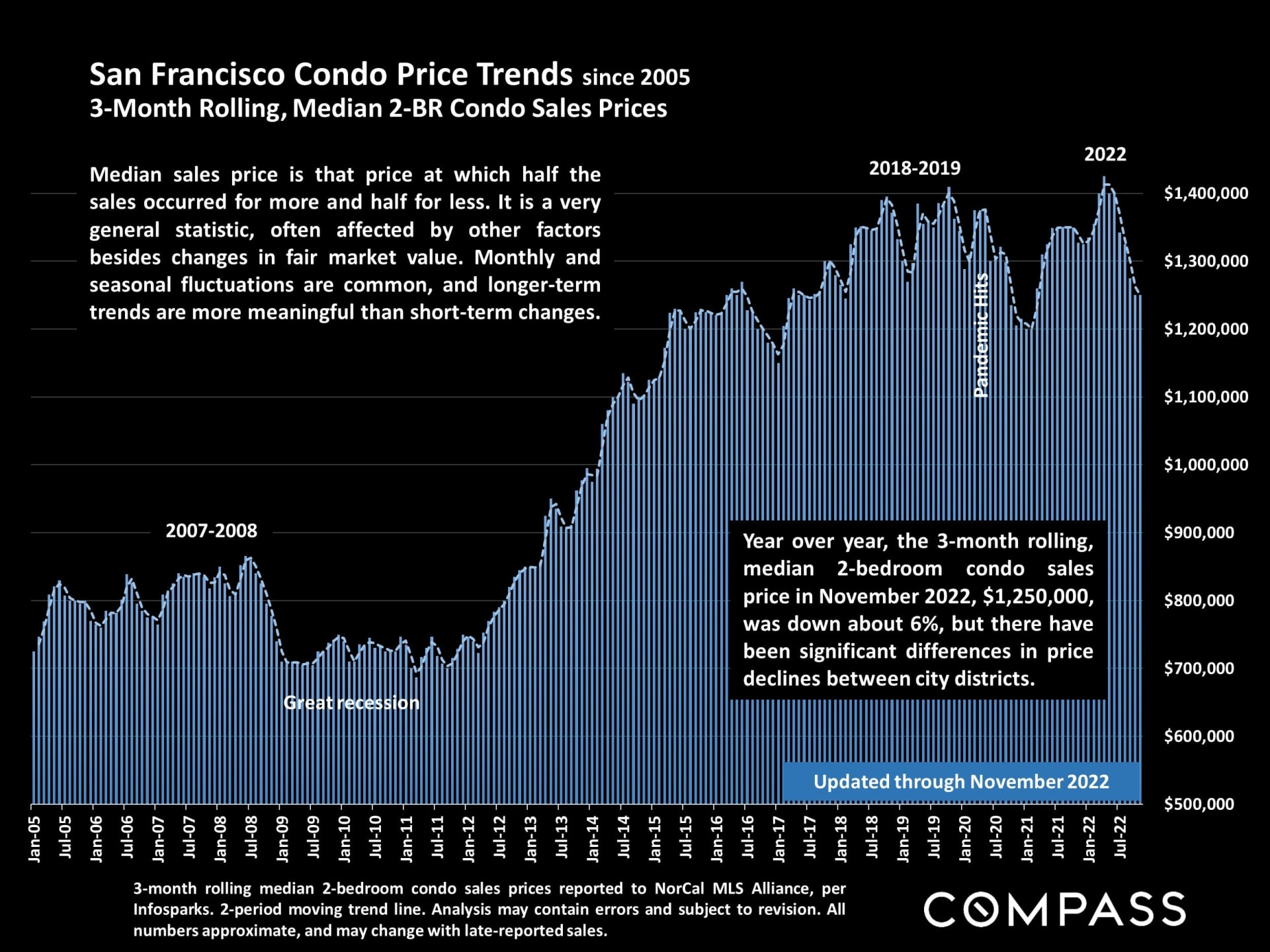

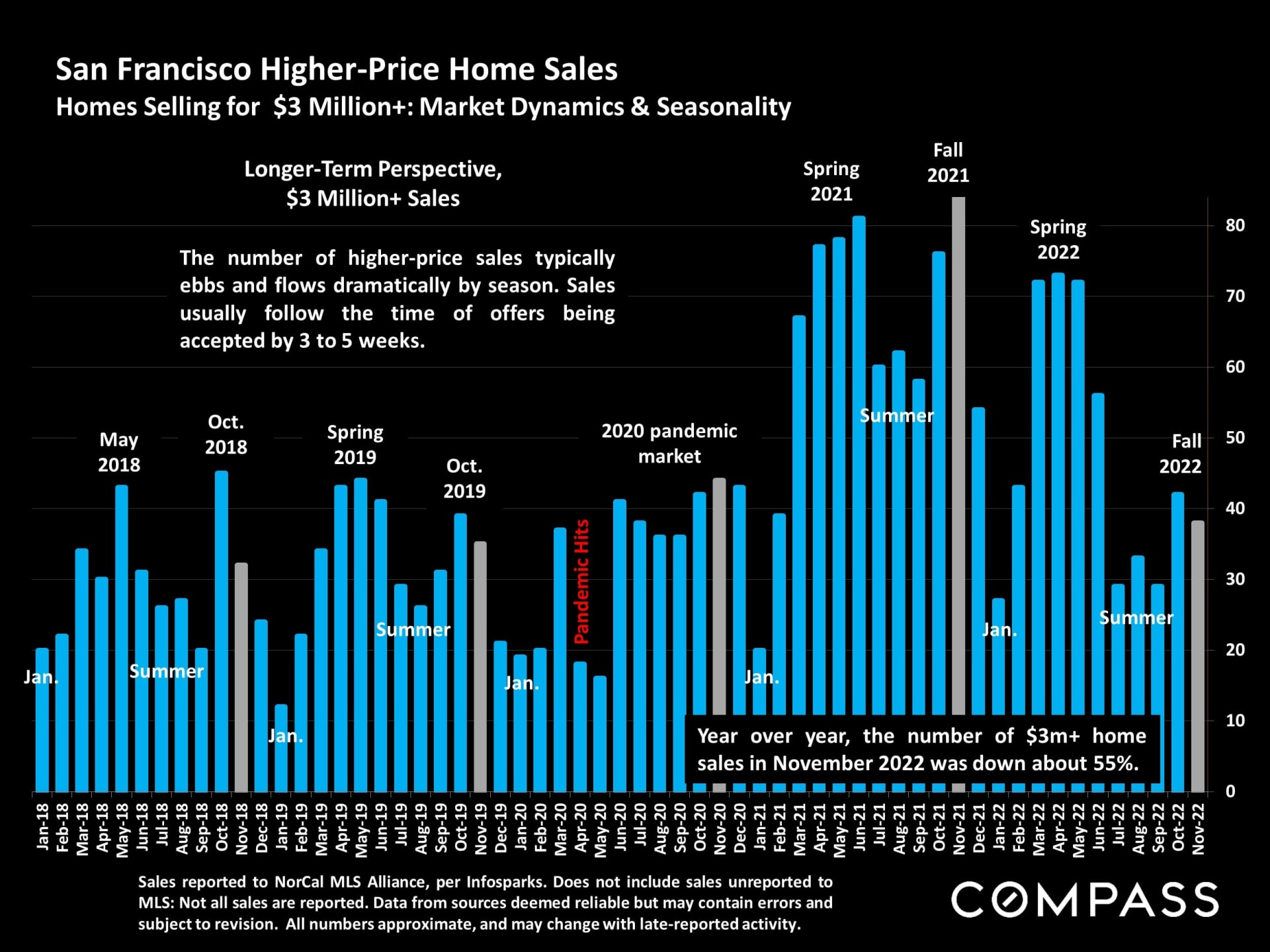

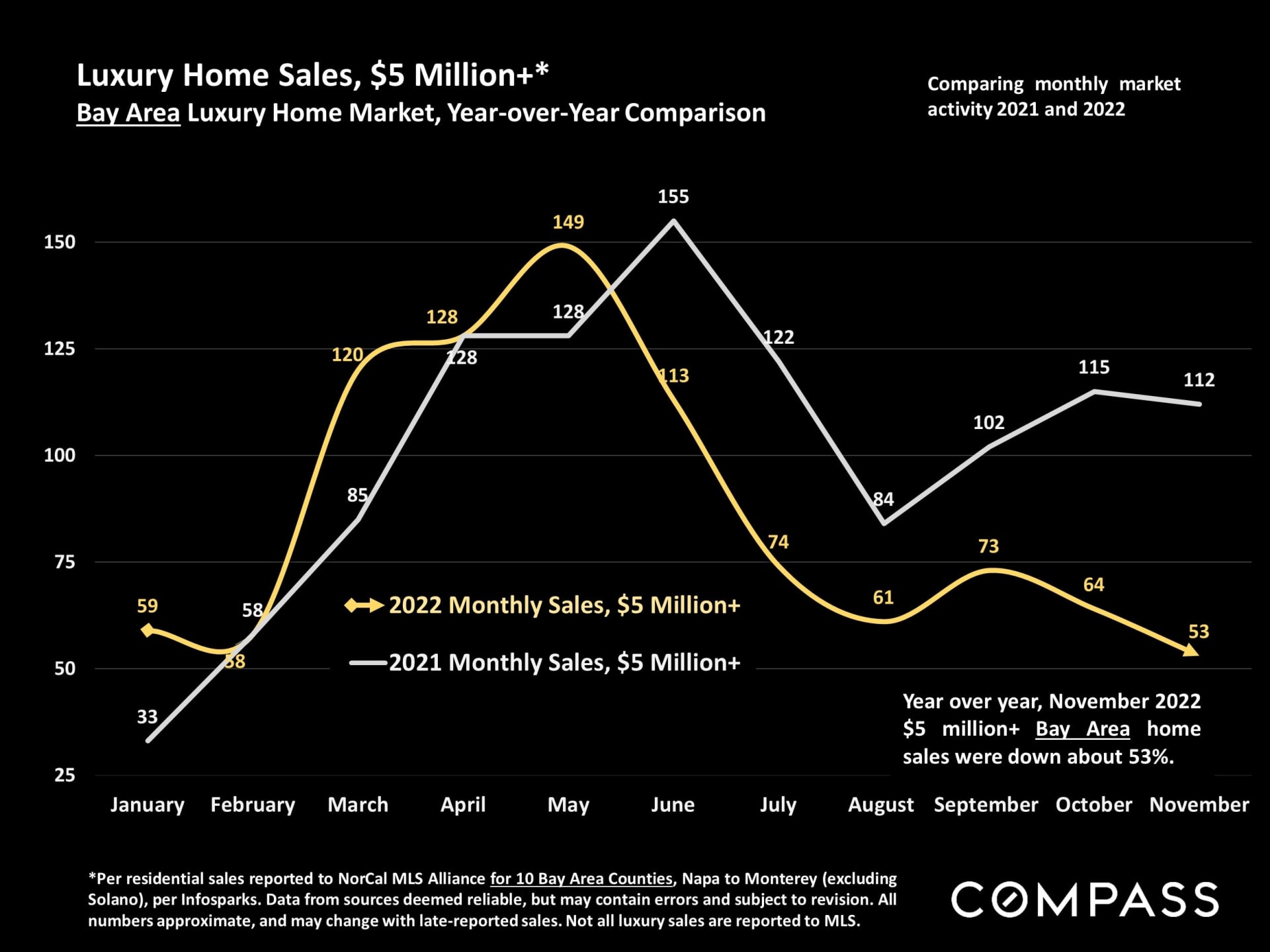

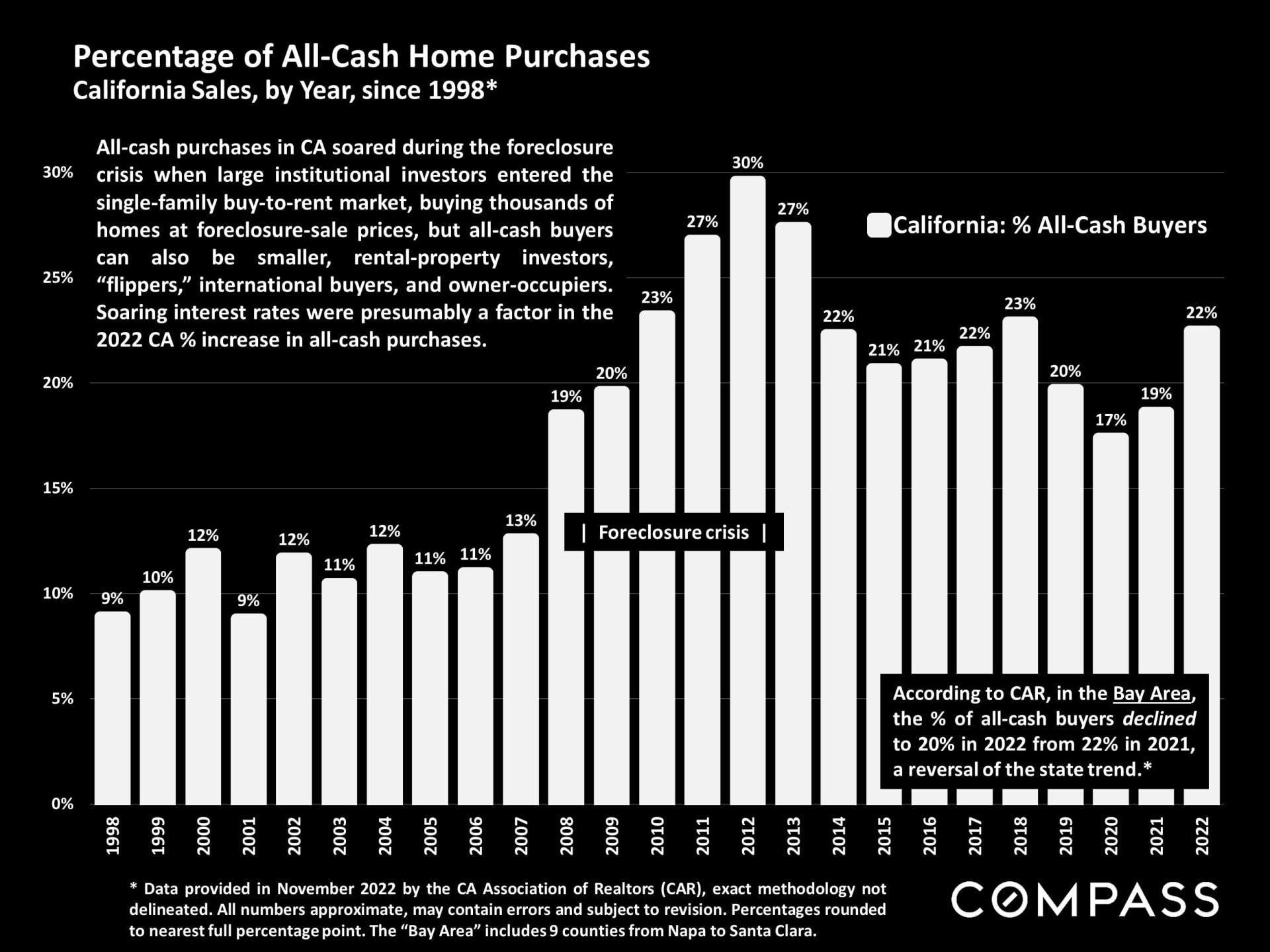

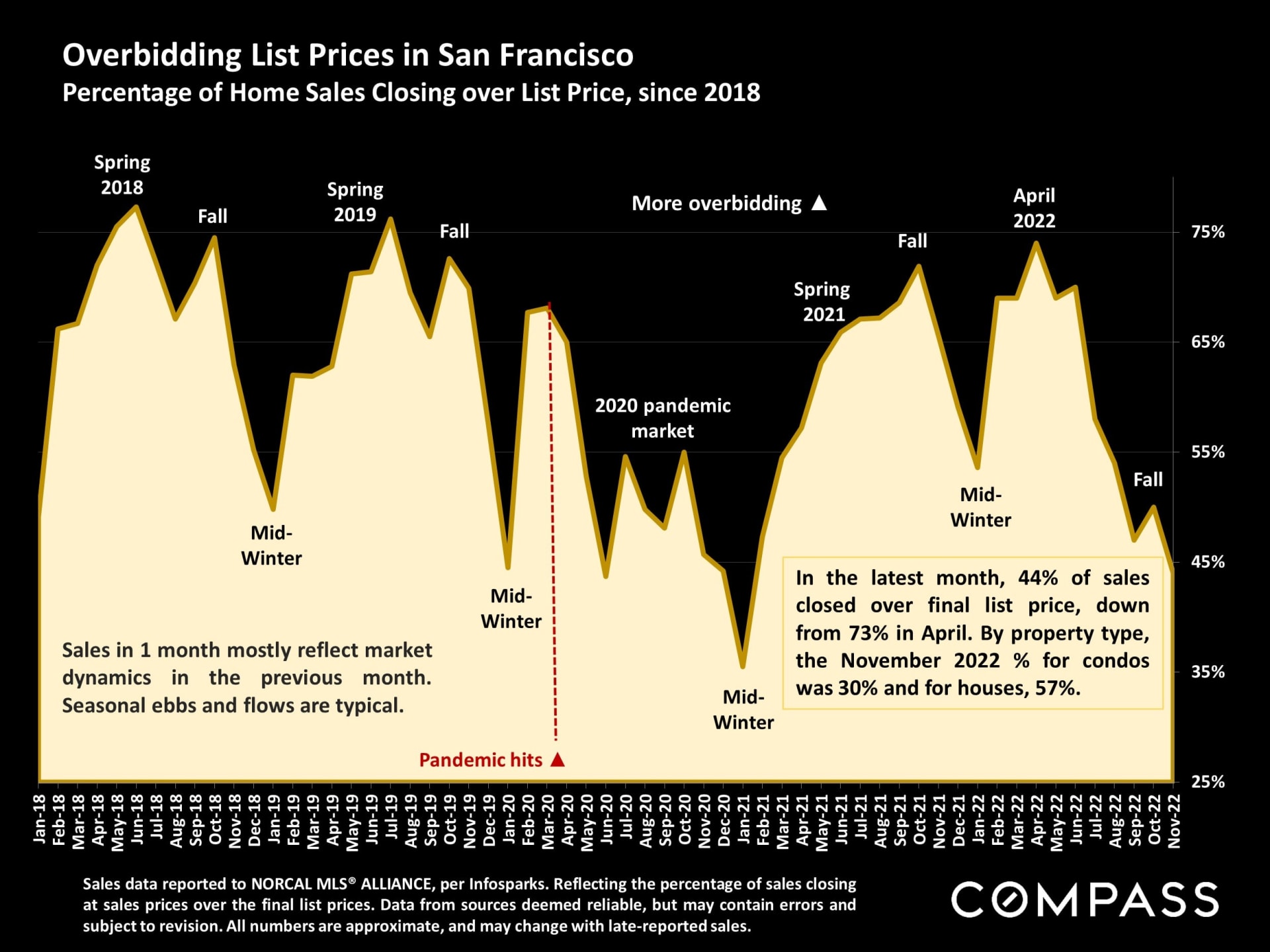

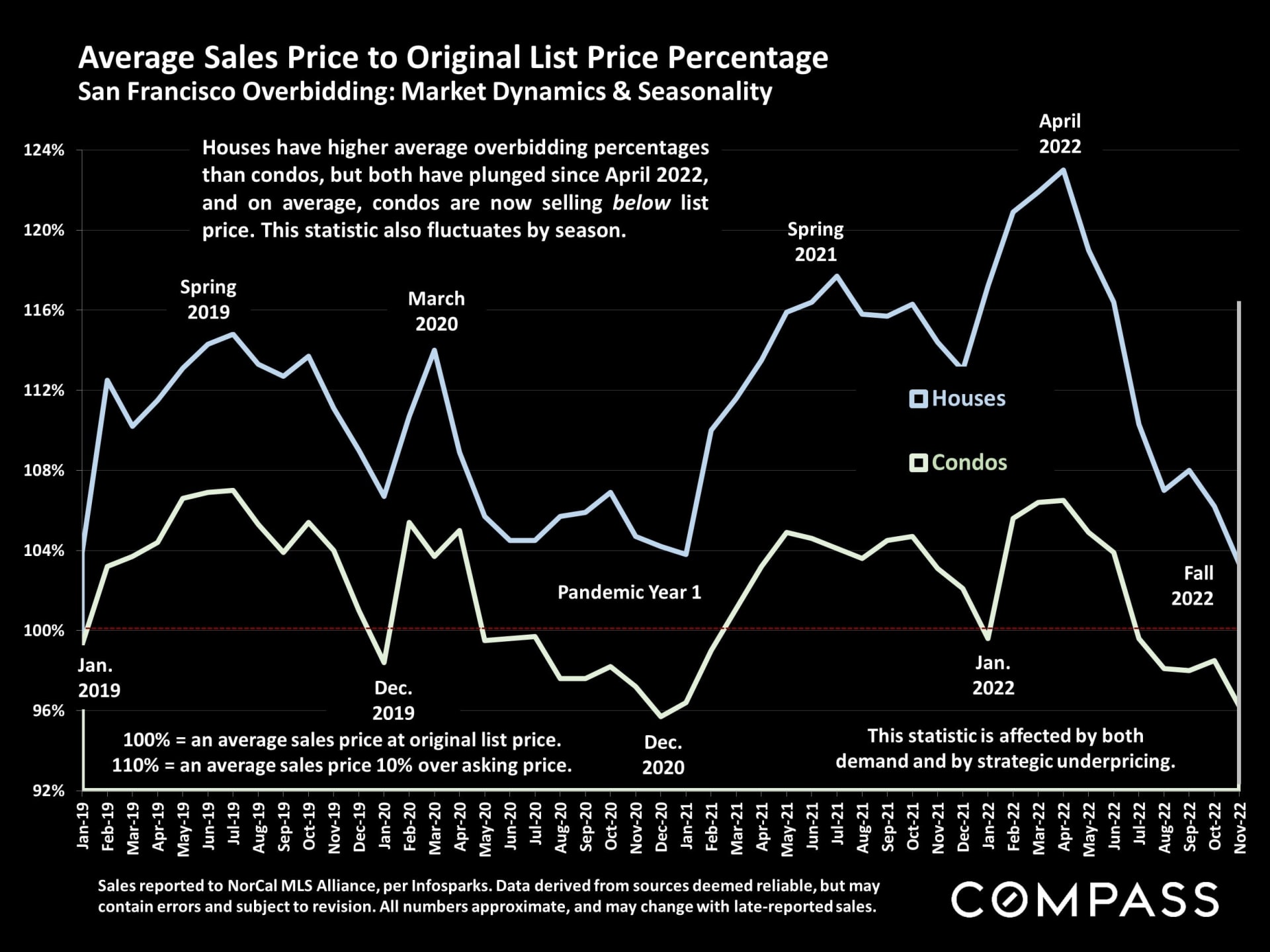

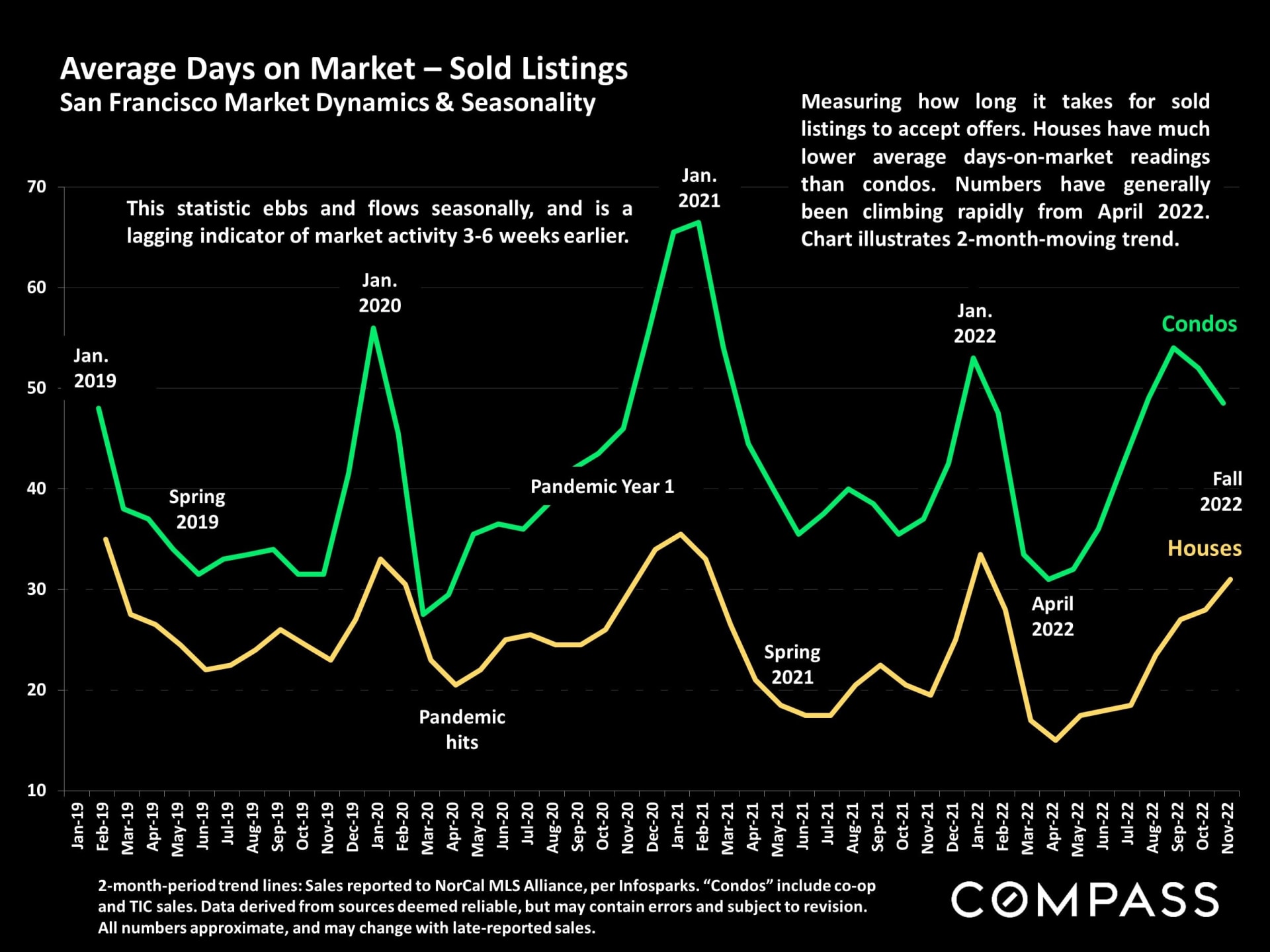

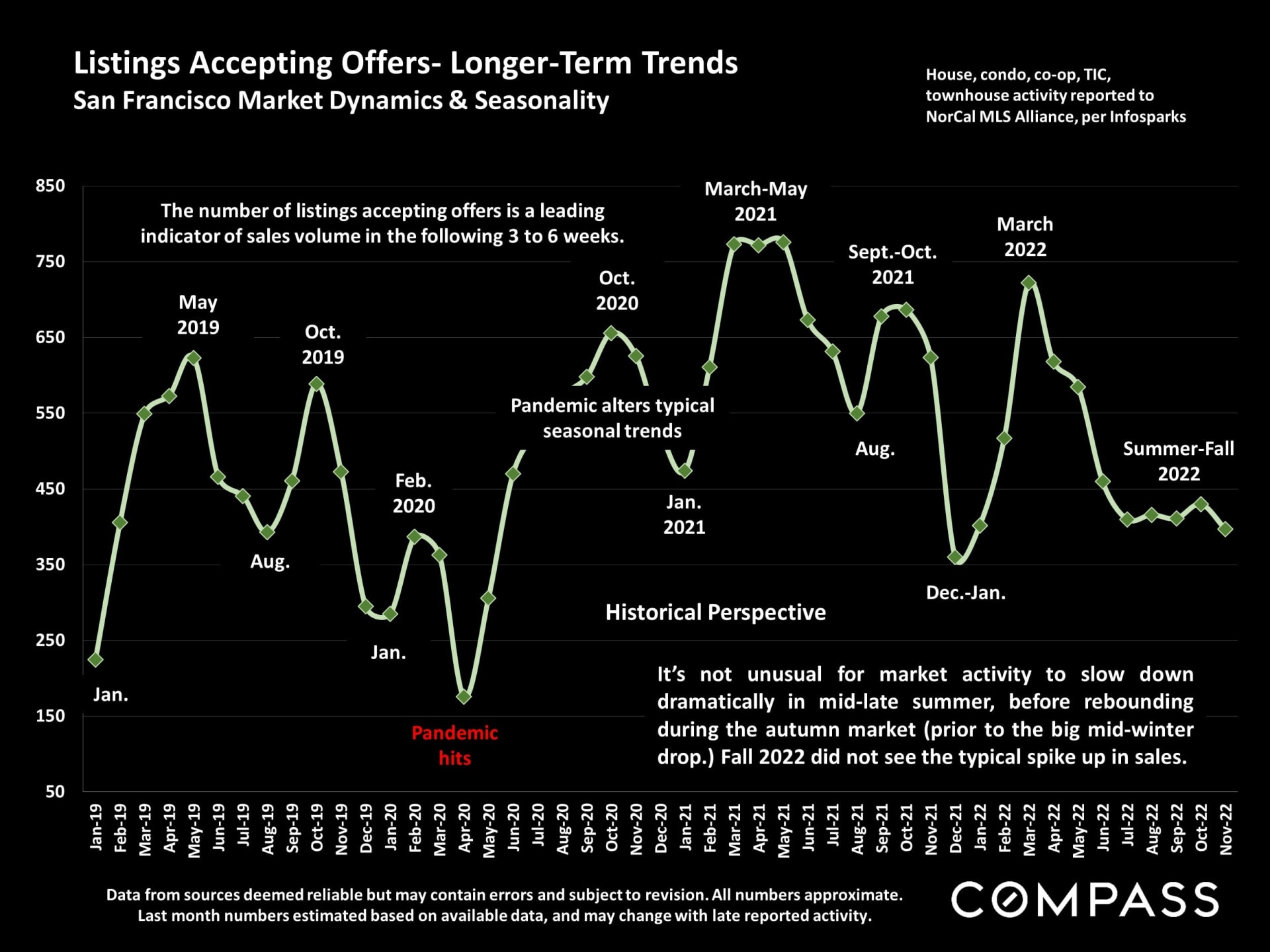

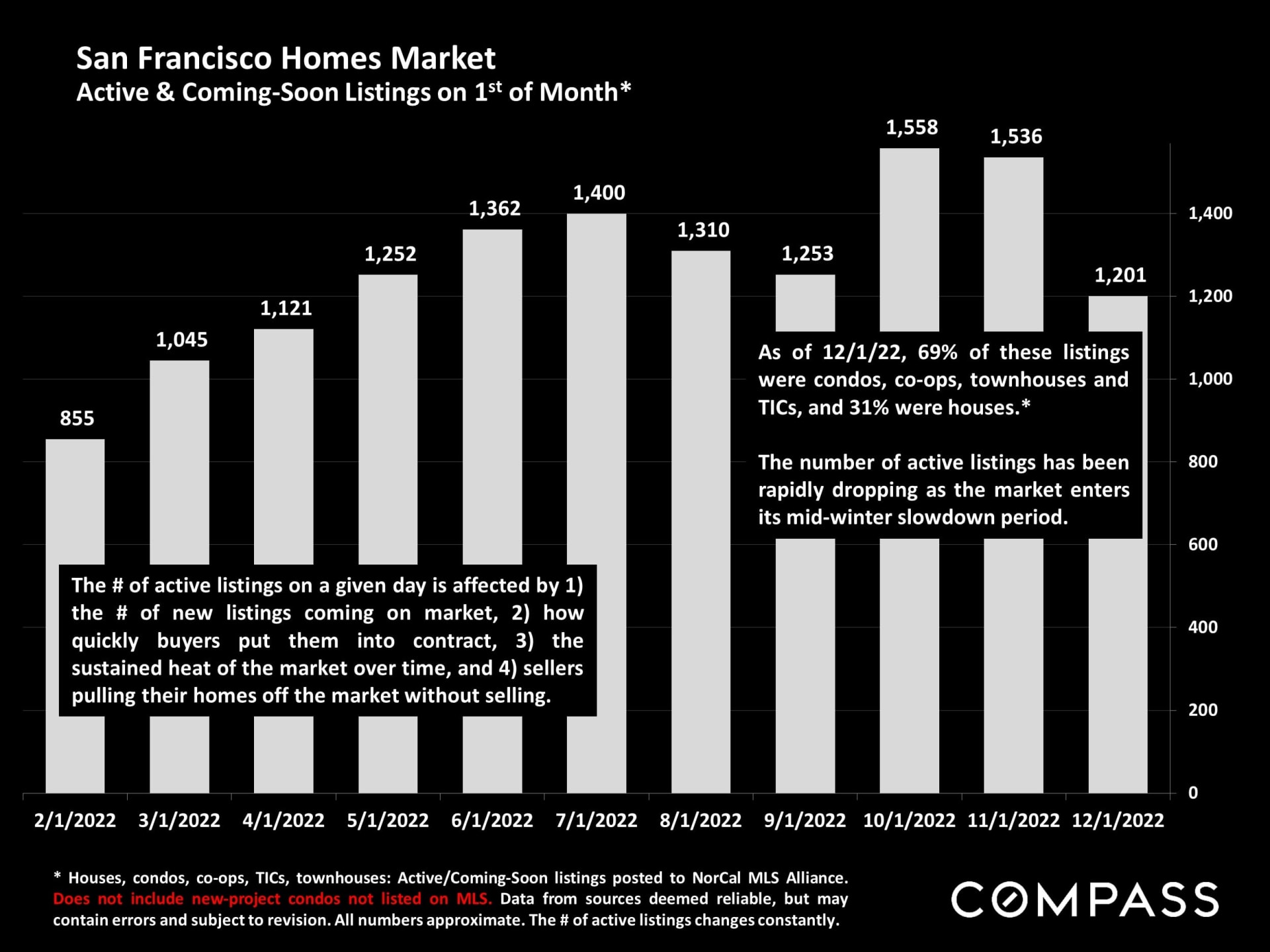

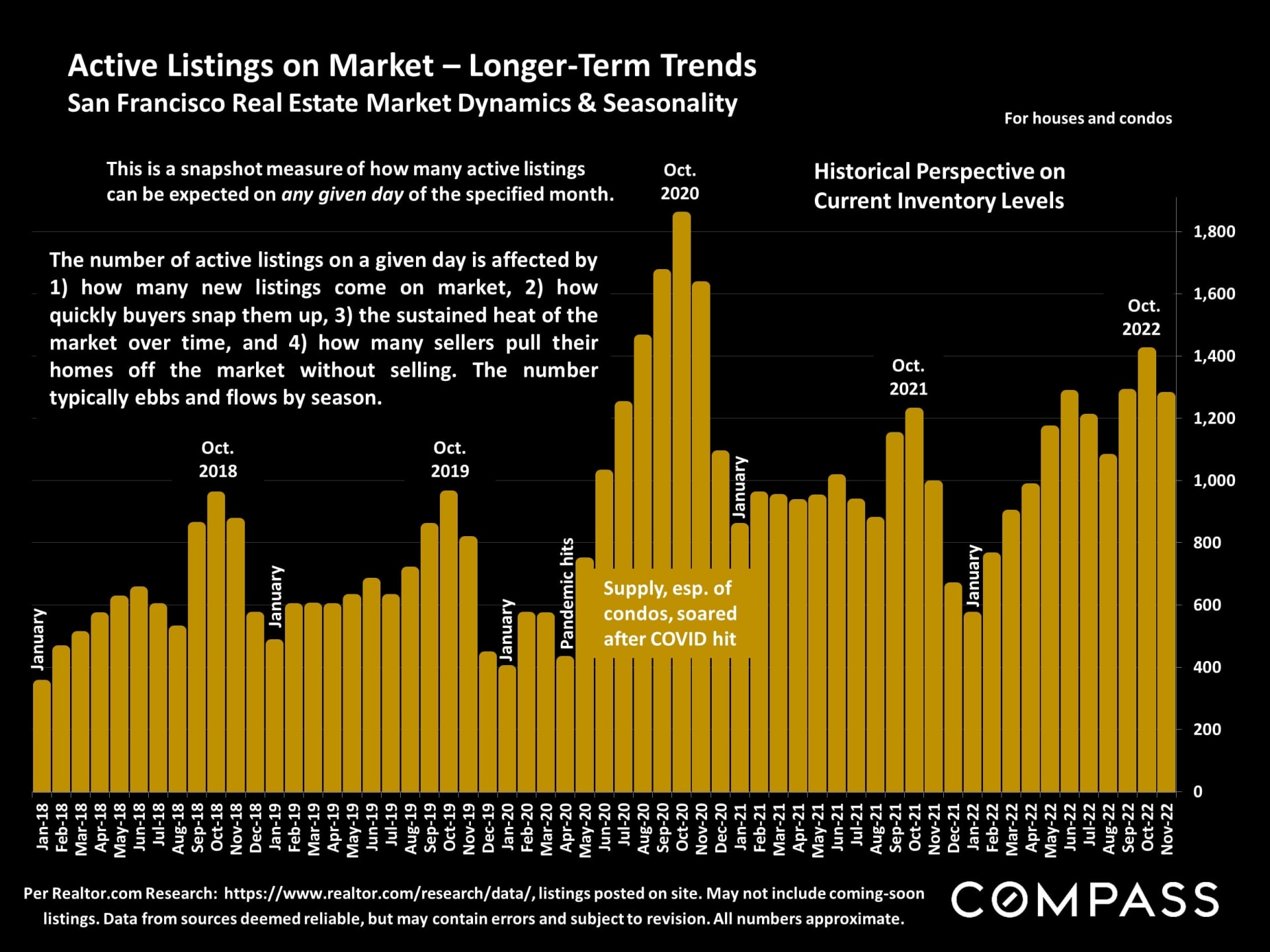

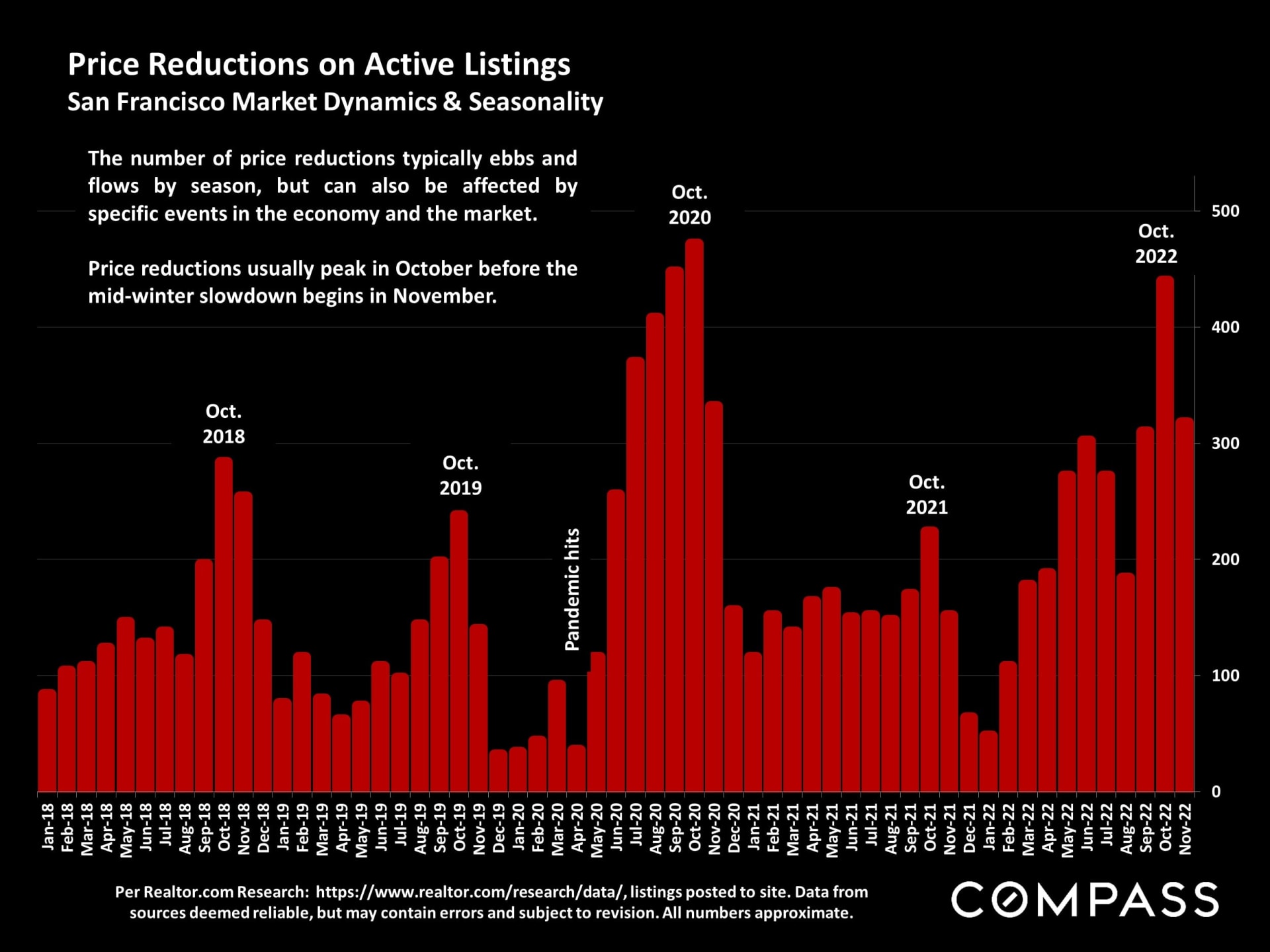

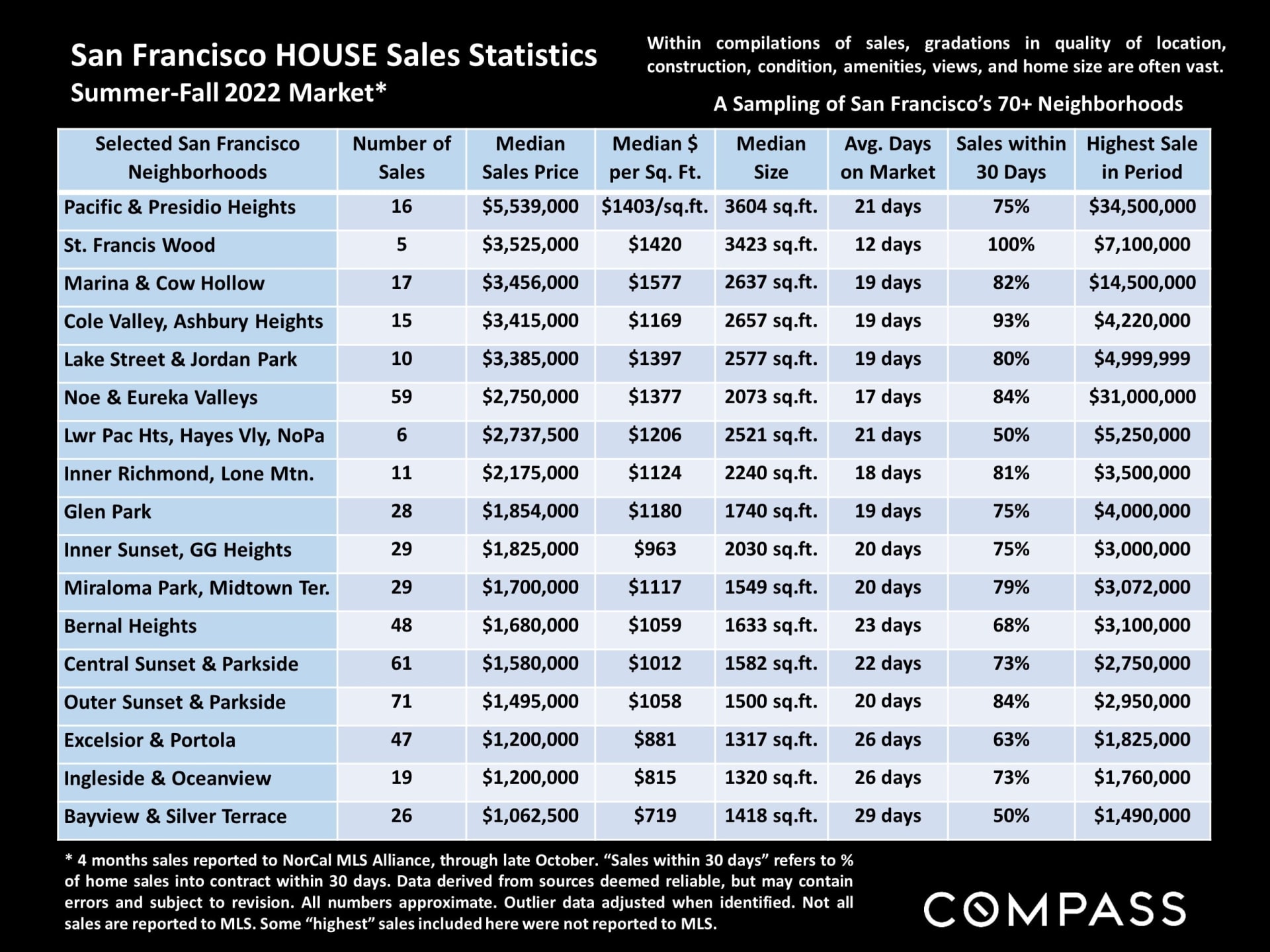

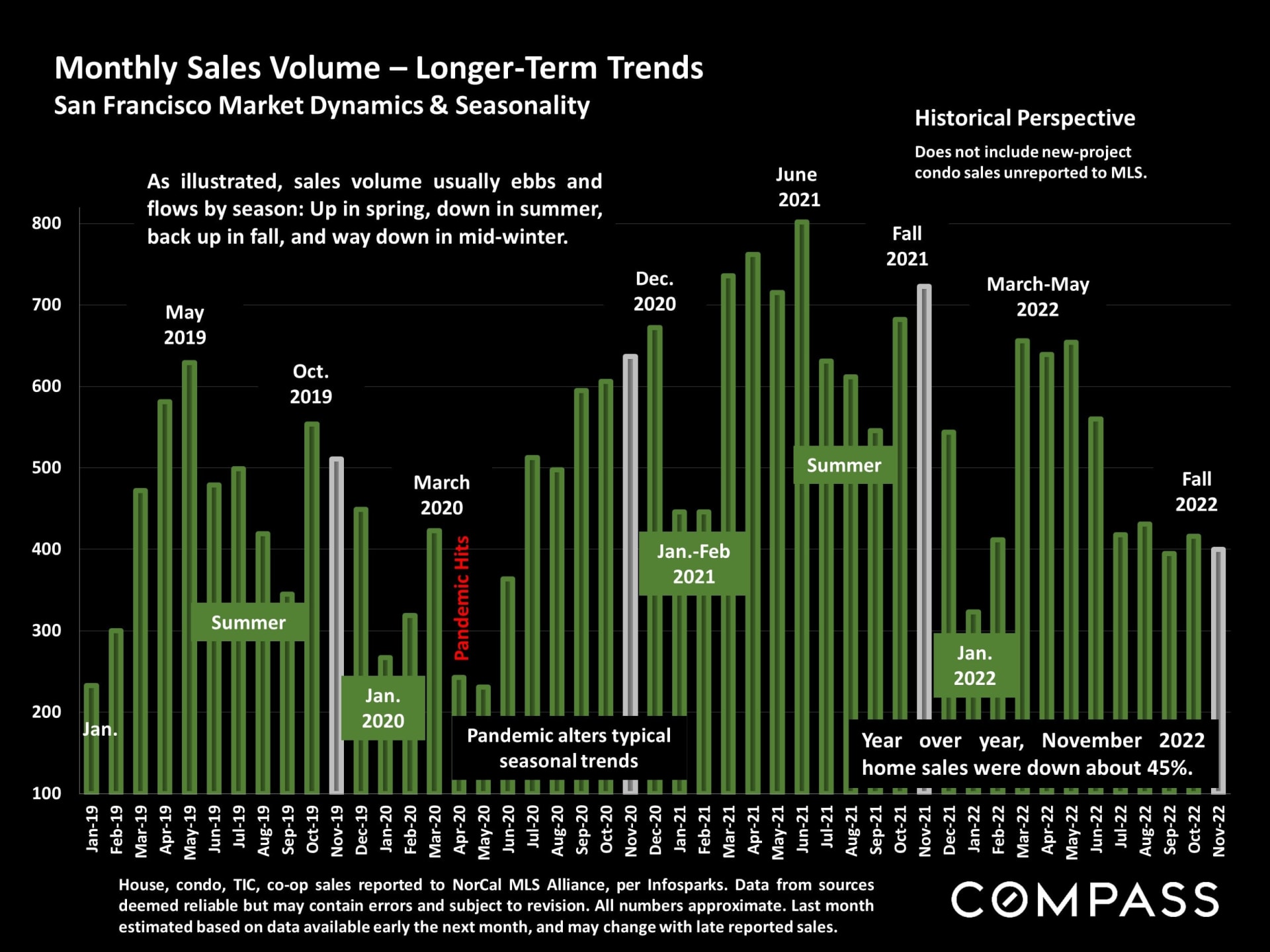

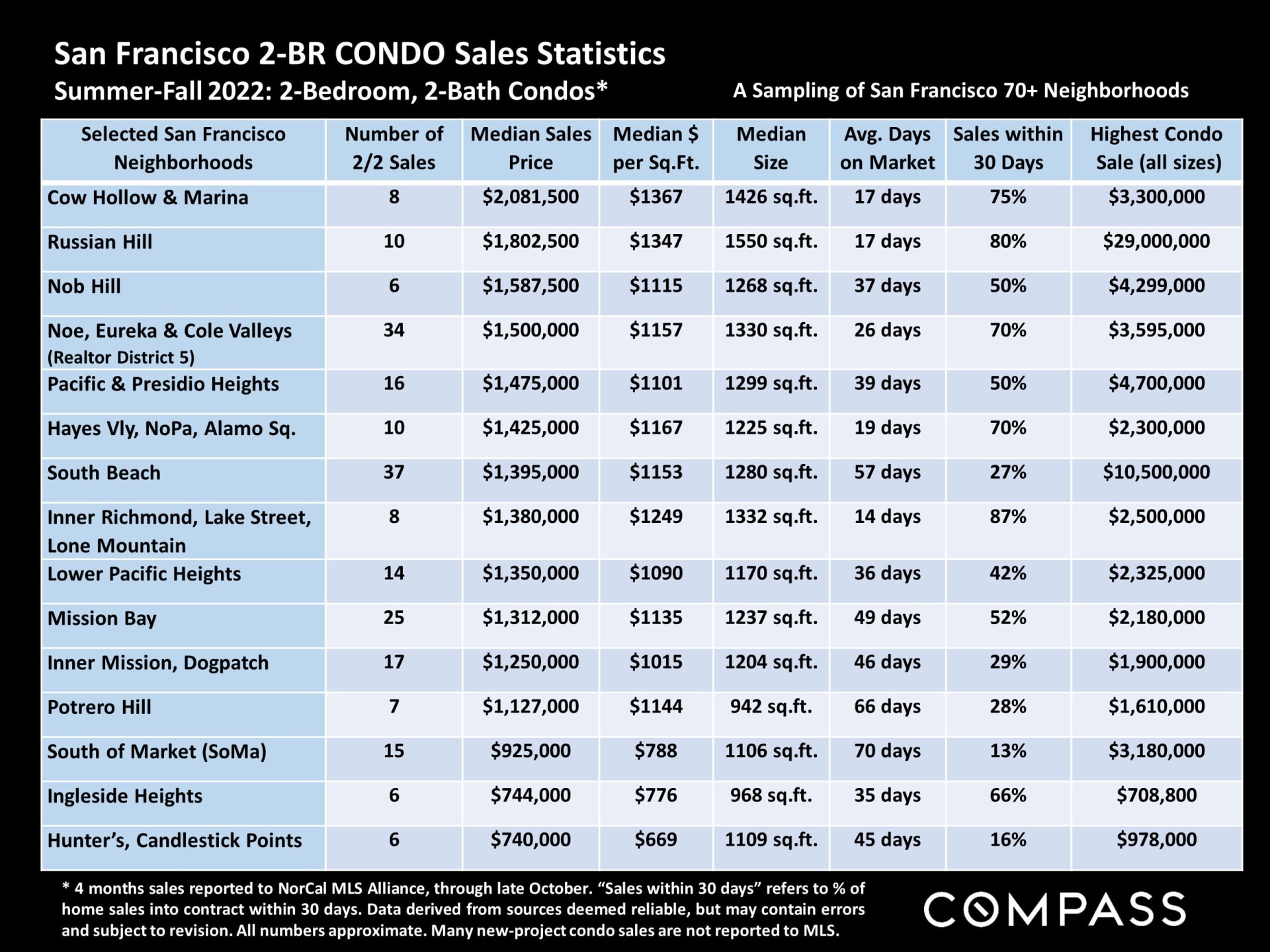

The changes in market dynamics that began in late spring/early summer 2022 generally continued in autumn due to the ongoing economic headwinds, including high inflation and interest rates, reduced consumer confidence, and volatile stock markets, though all have fluctuated significantly over the period, and some readings have recently improved. The great majority of indicators - home prices and appreciation rates, sales volumes, overbidding, days-on-market, months supply of inventory, and so on - continue to describe a market that has substantially cooled and "corrected" since spring 2022, when it appears that a long, dramatic, 10-year market upcycle peaked. The correction in San Francisco has been somewhat larger than in other Bay Area counties. (Note that a "correction" is not remotely similar to a crash, such as was seen during the subprime loan/foreclosure crisis.) In recent months, luxury home sales have seen larger year-over-year percentage declines than the general market. But thousands of Bay Area homes continue to sell, some very quickly at over asking price: With the shifts in market conditions, pricing correctly has become an imperative for sellers.

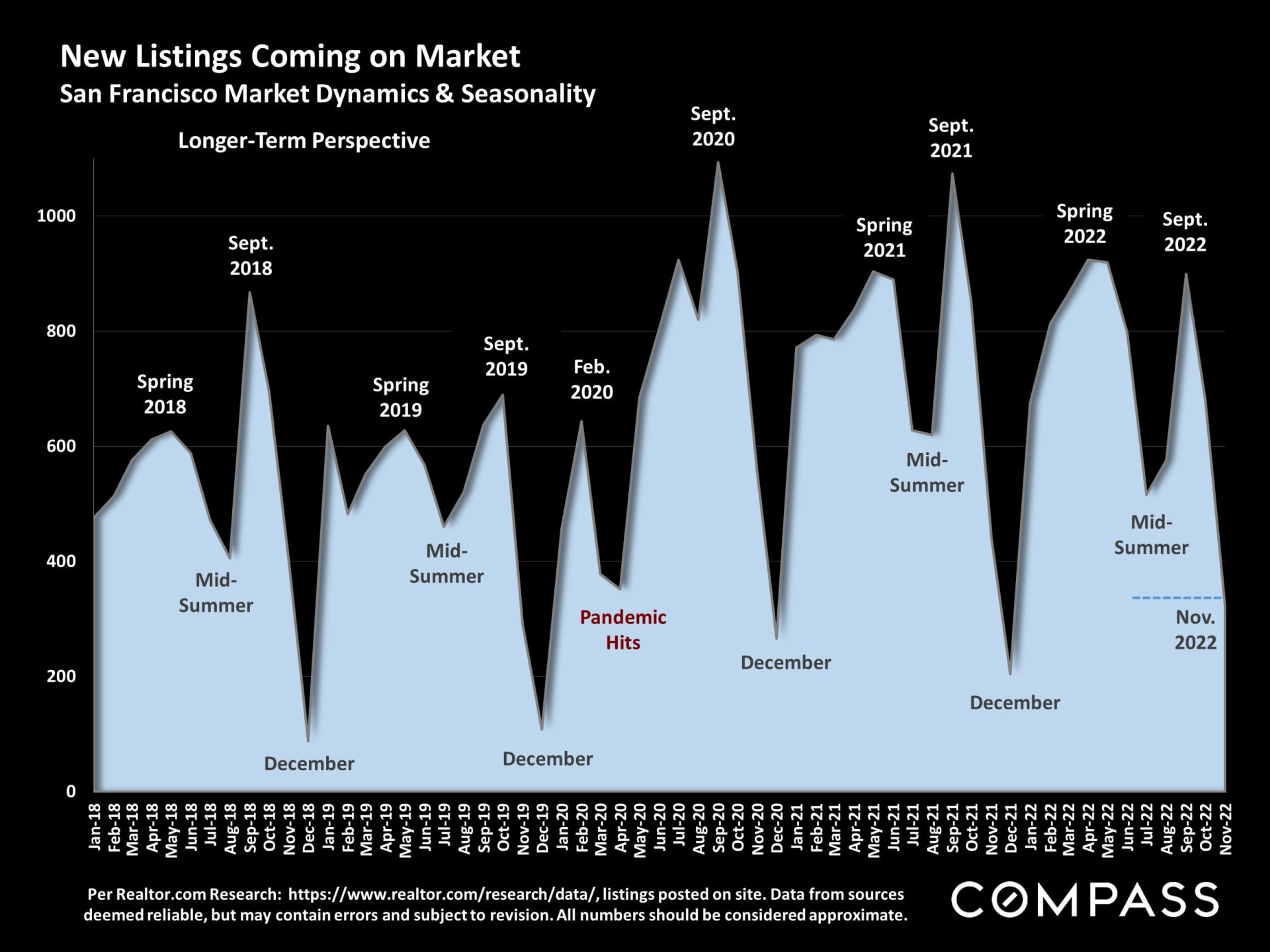

December typically sees the low point of new-listing and sales activity - with an increasing number of homes taken off the market to await the new year - but listing, buying and selling continues. This can be an excellent time for buyers to aggressively negotiate prices, though the supply of listings to choose from declines. The market usually begins to wake up in mid-January and then quickly accelerates in early spring: In the Bay Area, depending on the weather and economic conditions, the "early spring" market can begin as soon as February.

The single, most closely watched factor will be interest rates, since they have such an outsized impact on monthly housing costs and affordability, as well as on stock markets and consumer confidence. At the end of this report is a link to our extended review of macroeconomic issues.

Our reports are not intended to convince you regarding a course of action or to predict the future, but to provide, to the best of our ability, straightforward information and good-faith analysis to assist you in making your own informed decisions. Statistics should be considered very general indicators, and all numbers should be considered approximate. How they apply to any particular property is unknown without a specific comparative market analysis.