A few economic and market snapshots. The deep pessimism in financial and bond markets in October abruptly swung to soaring optimism in November.

Interest rates: the latest weekly average reading fell for the 5th week.

NAR published their "2023 Profile of Home Buyers & Sellers" in November. Some highlights:

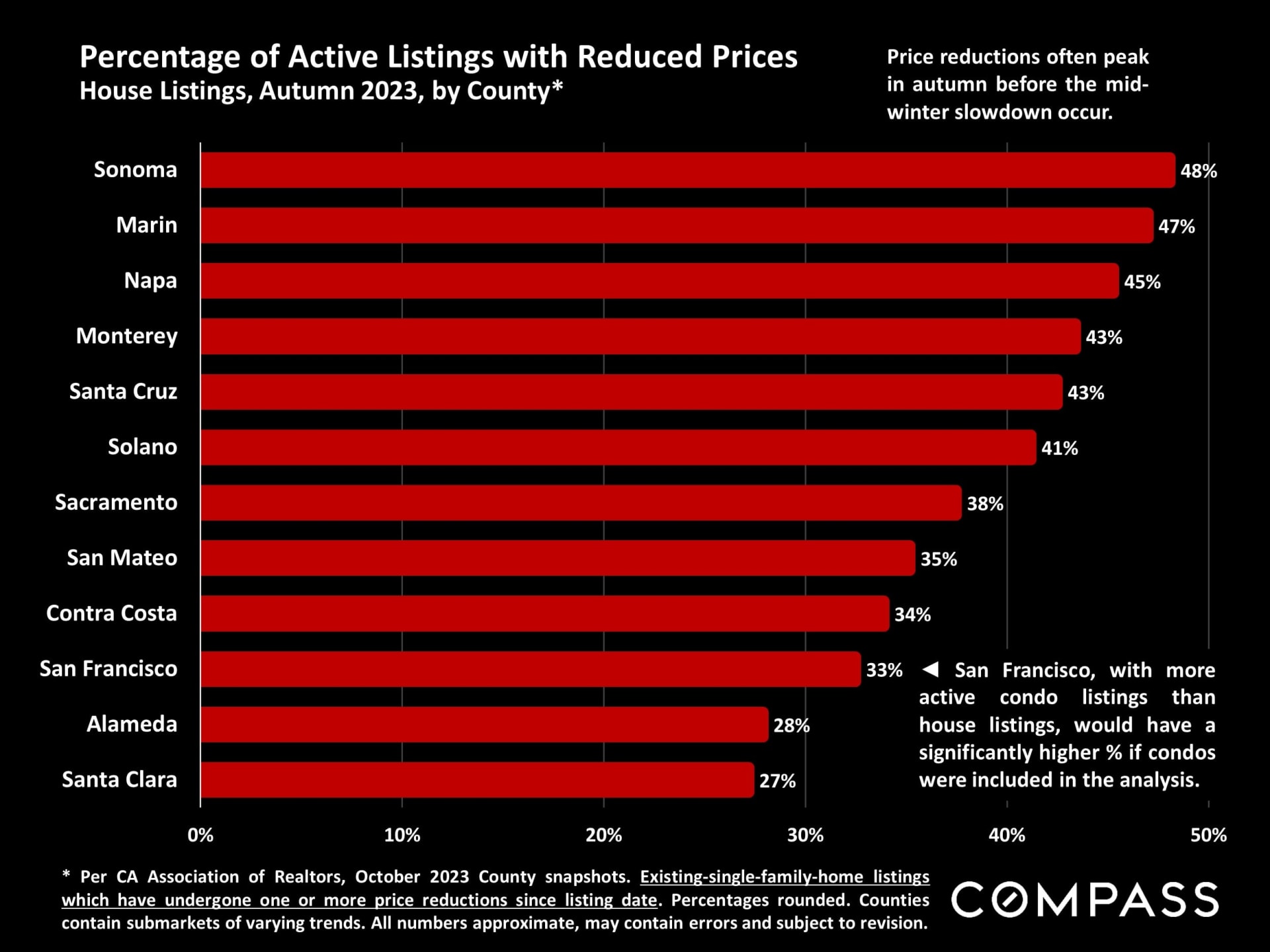

Active house listings that have had one or more price reductions: Per CAR data for October 2023. (November data not yet available.) In many counties, price reductions peak in October, as listing agents and sellers try to sell unsold homes before the mid-winter slowdown. CAR only tracks "existing single family home" listings for this statistic. In most markets, there isn't generally a huge difference between the strength of house, condo and townhouse markets currently, but in SF, the condo market is much softer in comparison (and 70% of SF active listings are now condos or condo-like property types).

Stock markets: A tremendous rebound in November from the late October low.

GDP increase for Q3 jumped. It was the fastest pace of expansion since the fourth quarter of 2021.

NAR has published 2 remodeling reports (interior and outdoor) - which I just discovered - and some of their data is highlighted in this table. (Remodeling is different from staging: See note below table.)

The complete NAR remodeling impact reports can be downloaded from this folder. The folder also includes a selection of links to articles about the value of staging, and some ideas for the discussion with clients regarding "Preparing the Property to Show."

Hanley-Wood also posts cost vs. value estimates for remodeling projects, nationally and by region: https://www.remodeling.hw.net/cost-vs-value/2023/

The Economist Intelligence Unit just released their new "Worldwide Cost of Living" ranking. Below are the 10 cities they rank as the most expensive to live in. It is unclear whether by cities, they mean only the city or the greater metro region.

Bookmark to Patrick's Market Analytics Resources

Weekly Update: Inflation, Interest Rates, Consumer Confidence, Foreclosure Rates

The general inflation reading for November was released and ticked down to 3.1% from 3.2% in October, while the "core inflation" reading was unchanged at 4%. Below are short-term and long-term charts. As of early Tuesday (12/12), stock and bond markets seem bemused by the lack of significant change, and index movements have been slight.

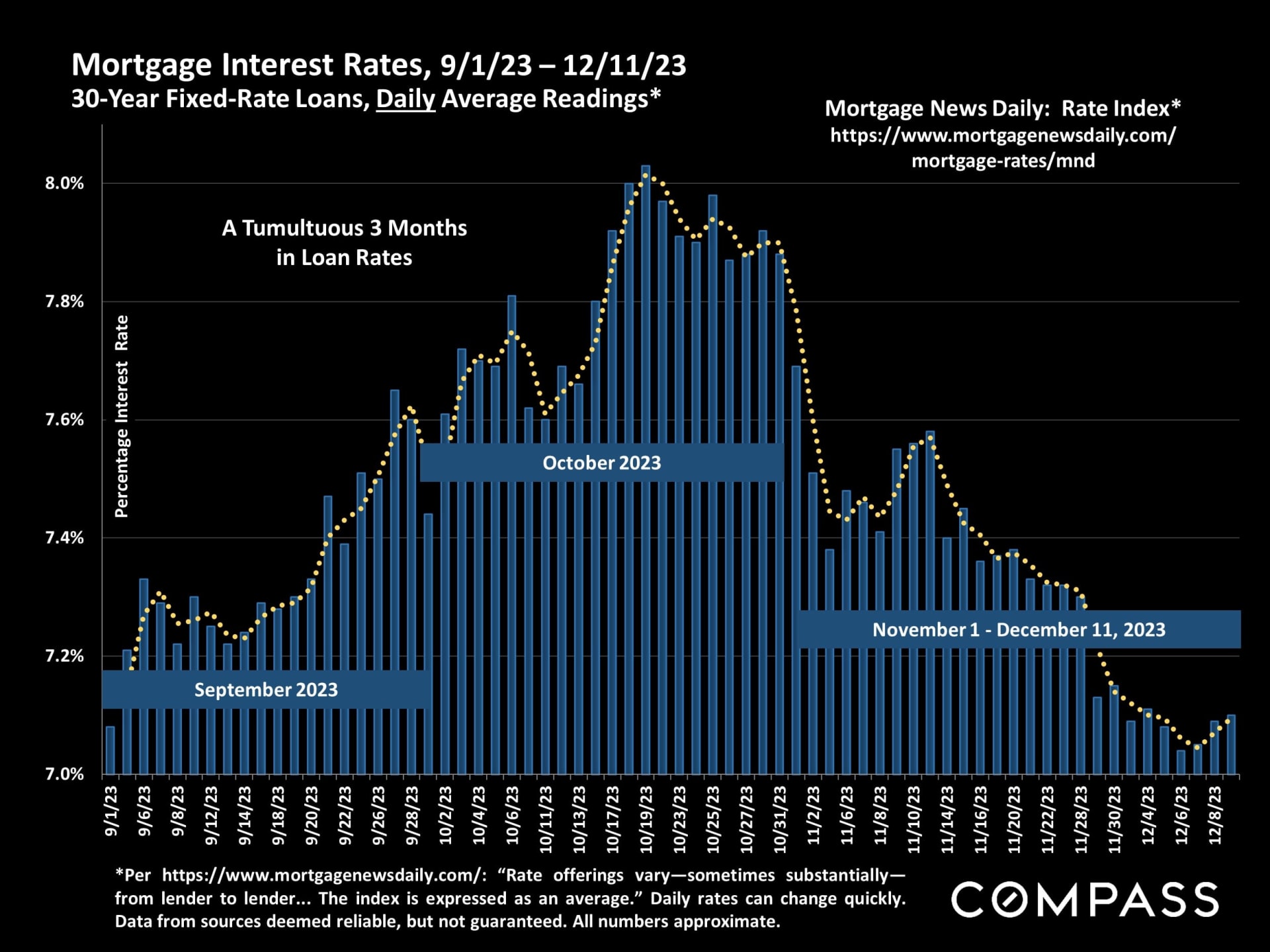

Daily average interest rates through 12/11/23:

Weekly average interest rates through 12/7/23 - the next update is Thursday:

Consumer Confidence jumped in the preliminary December reading, as people projected that inflation will continue to rapidly decline.

The Bay Area foreclosure rate was updated through Q2 - it remains close to zero.