San Francisco Real Estate

February 2024 Report

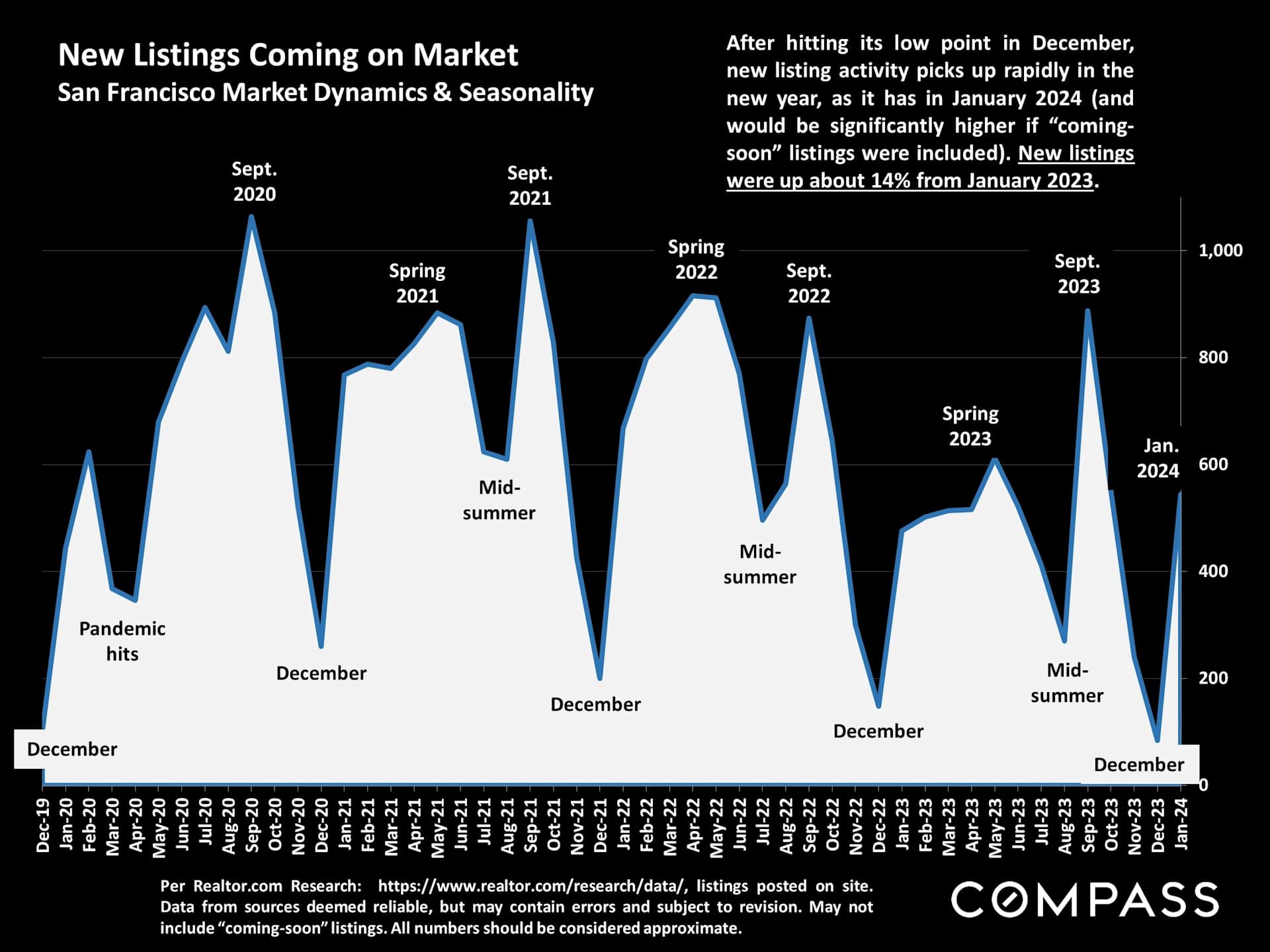

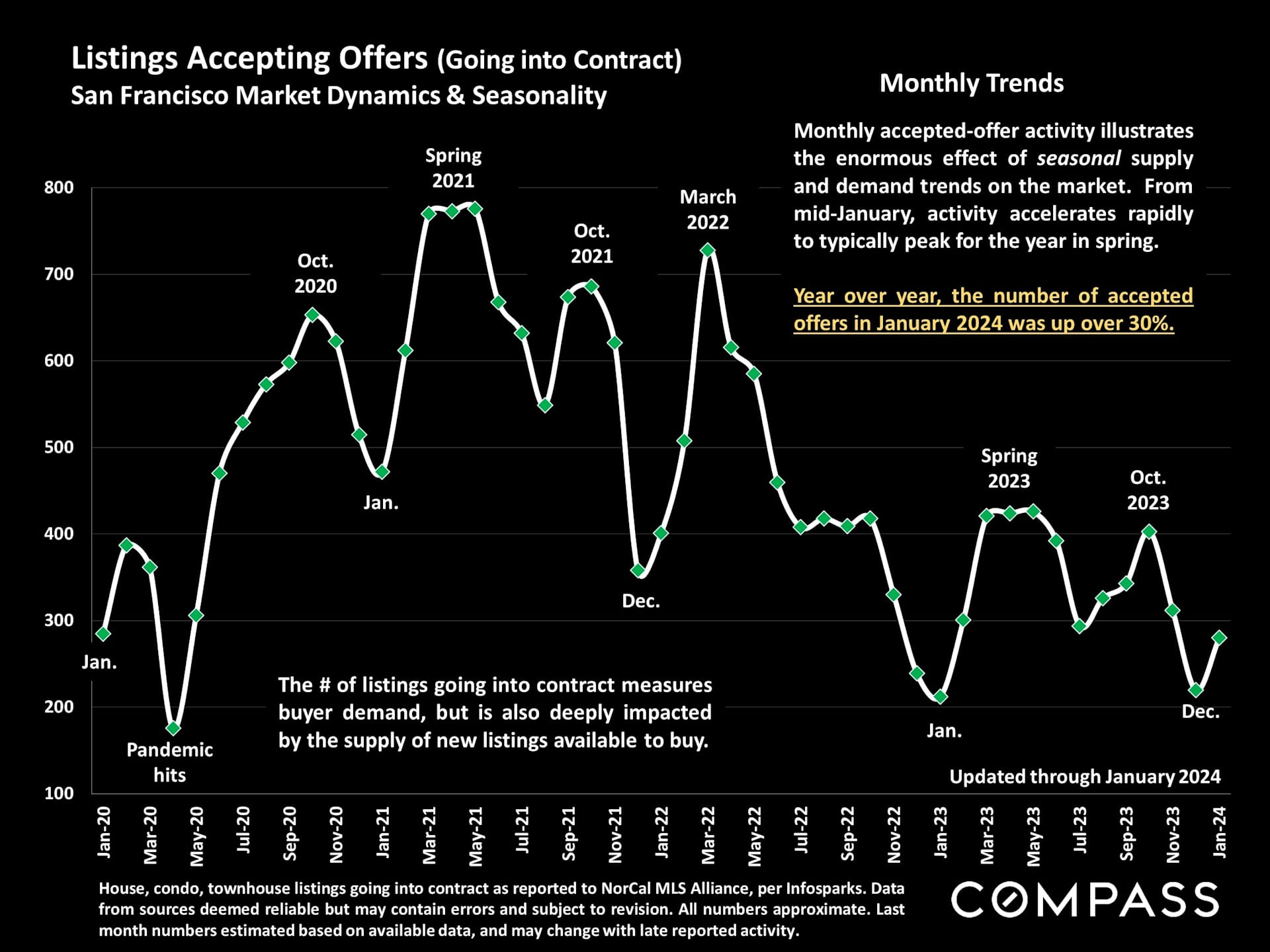

Open house visitor numbers have surged, new listings coming on market have risen, the pipeline

of coming listings is filling up faster than last year, and the number of homes going into contract

is climbing rapidly as the market wakes up. With dramatic improvements since October in

interest rates, stock markets and consumer confidence, both buyers and sellers are re-engaging

to a much greater degree, and the velocity of the market is accelerating.

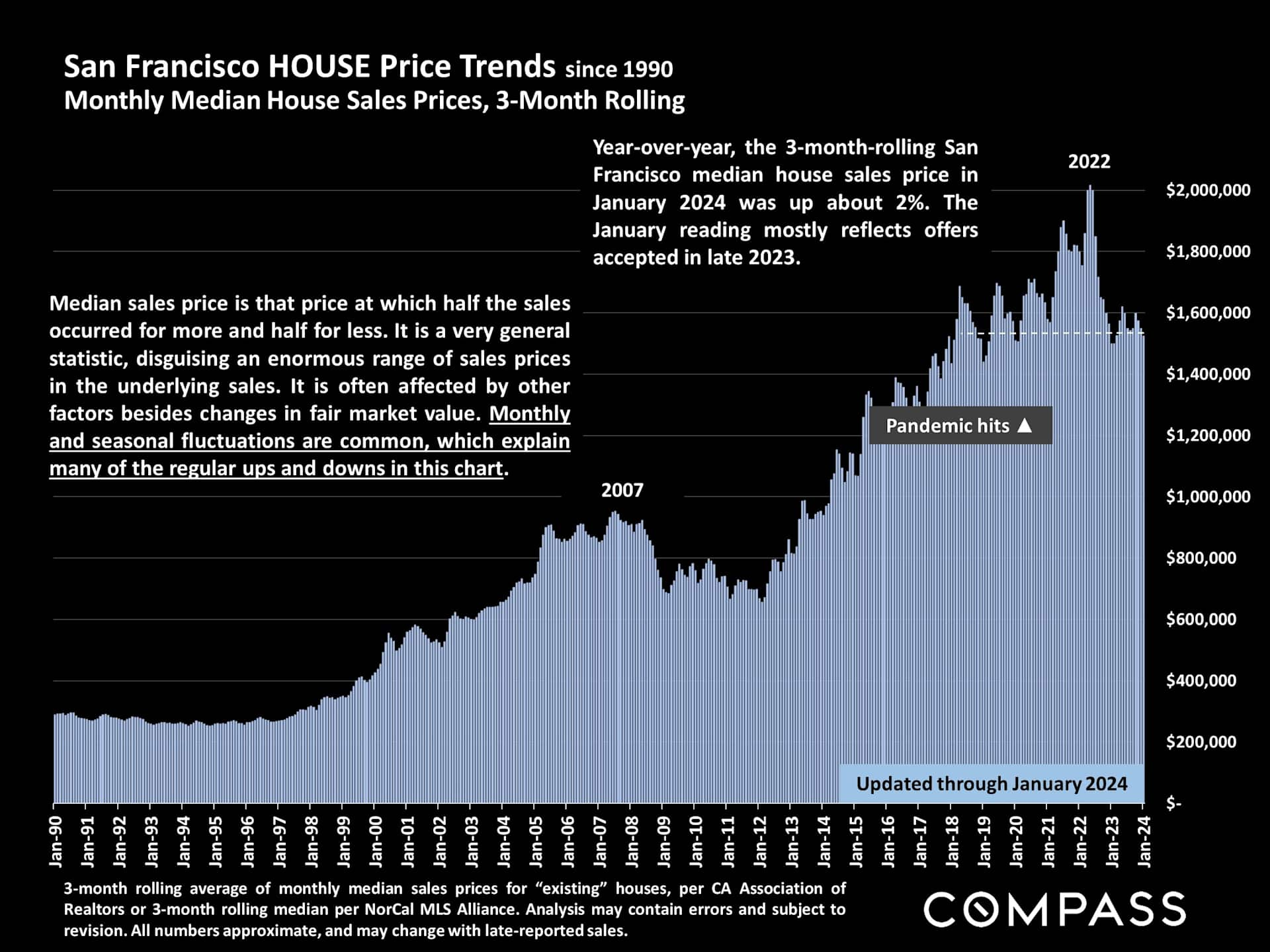

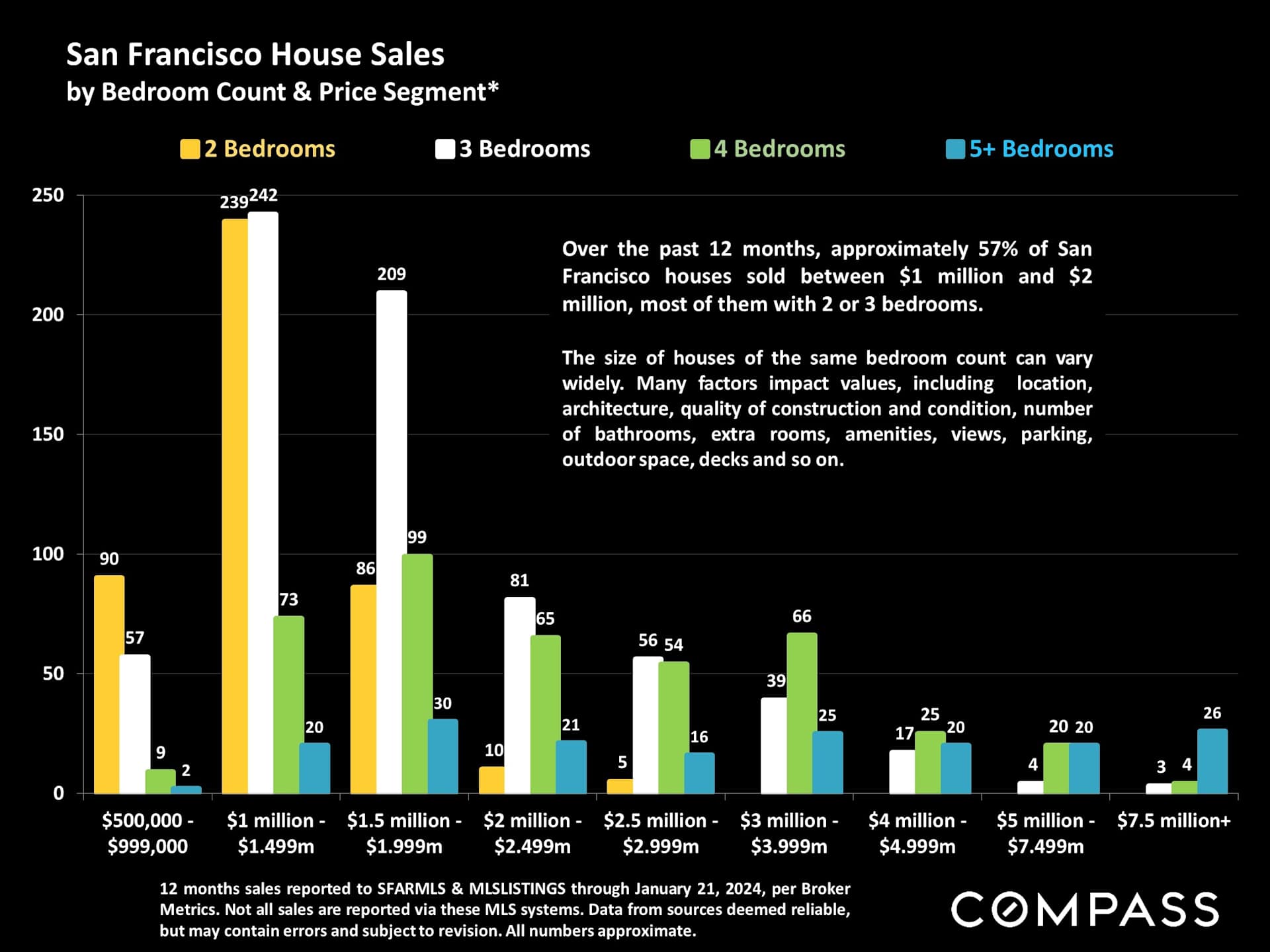

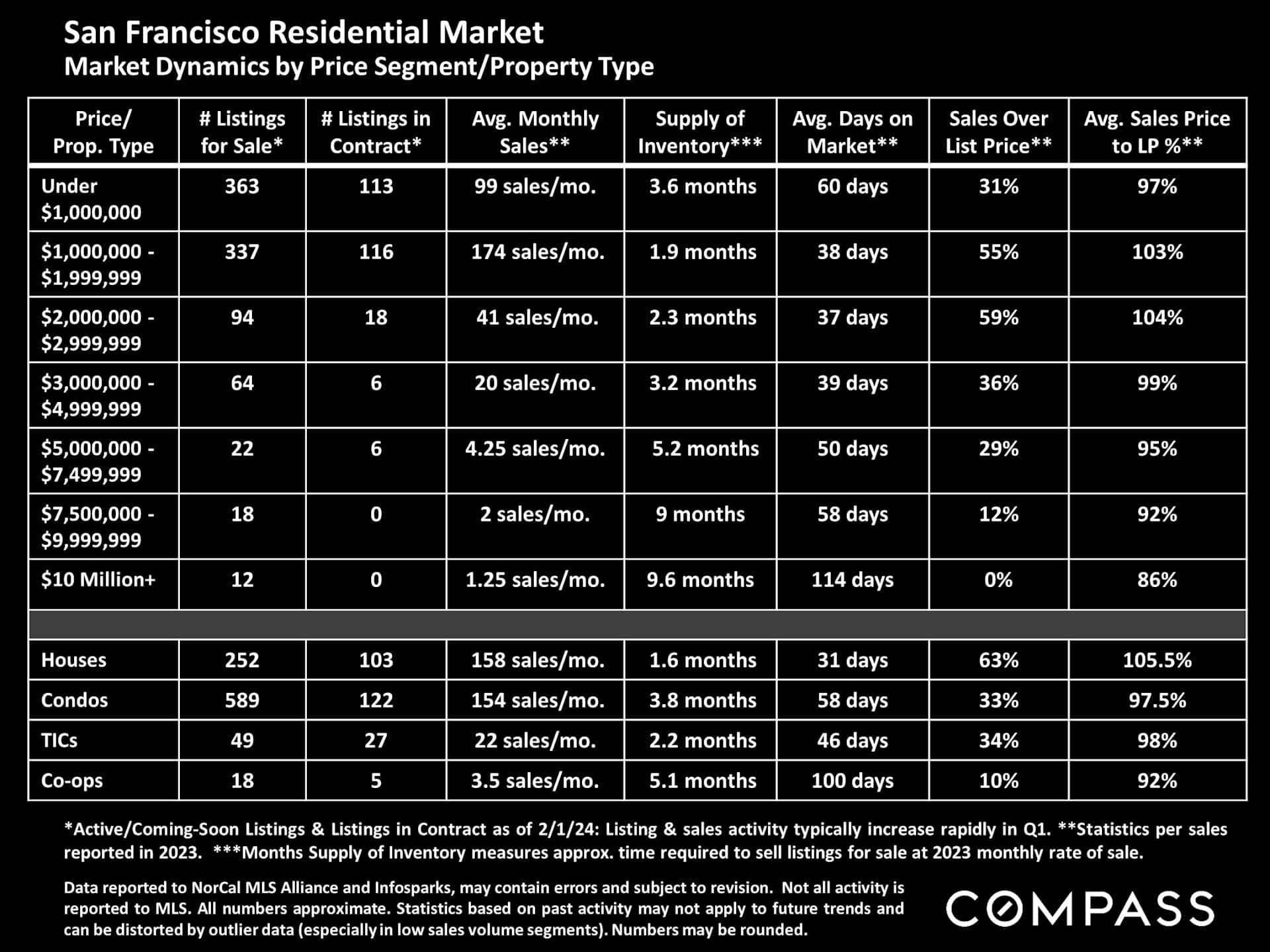

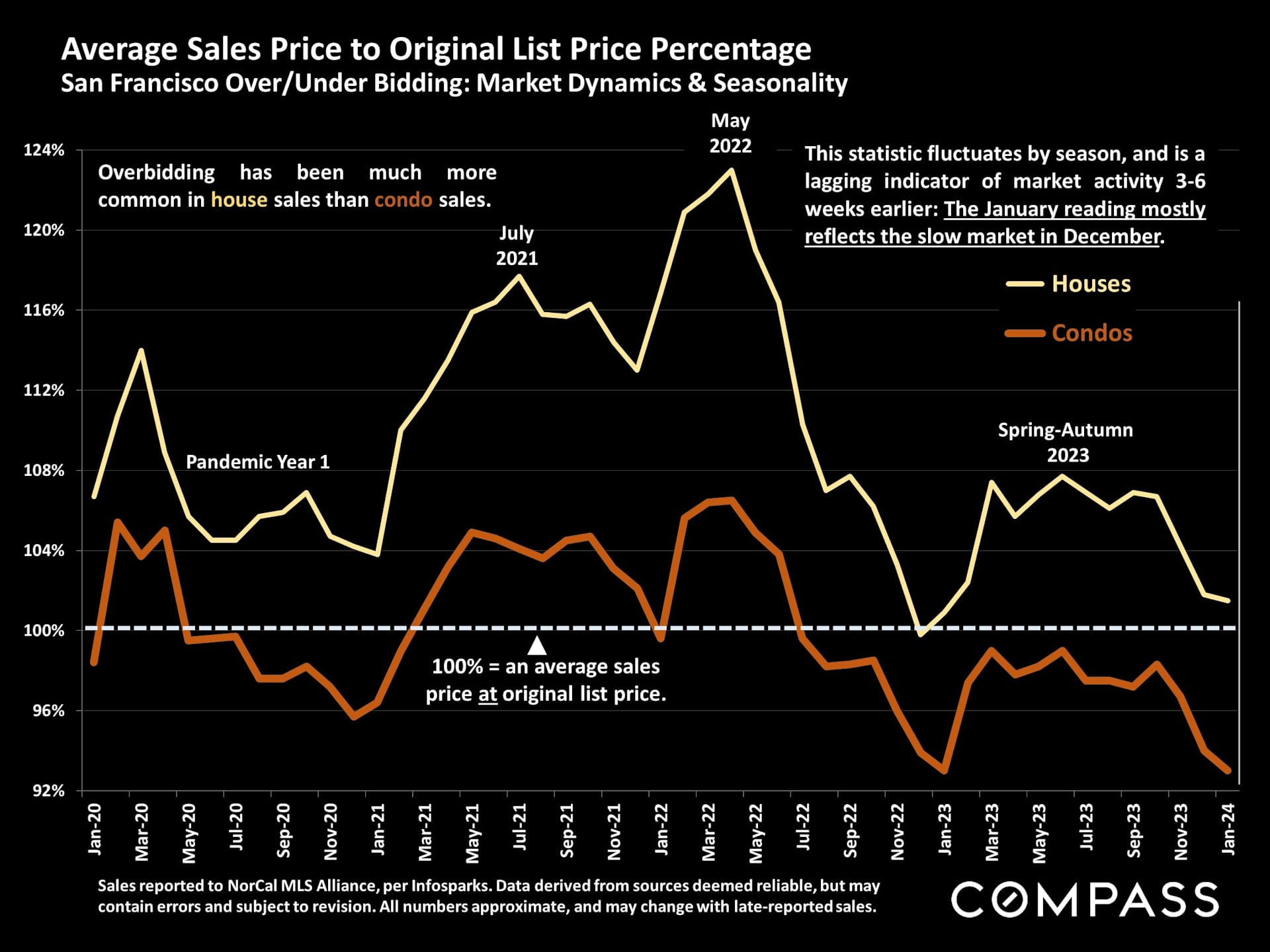

The inventory of house listings remains very low compared to pre-pandemic norms, and the

demand vs. supply dynamic is very tight in that segment: One of the big questions in 2024 is how

many homeowners, having held off listing their houses since mid-2022, move forward with

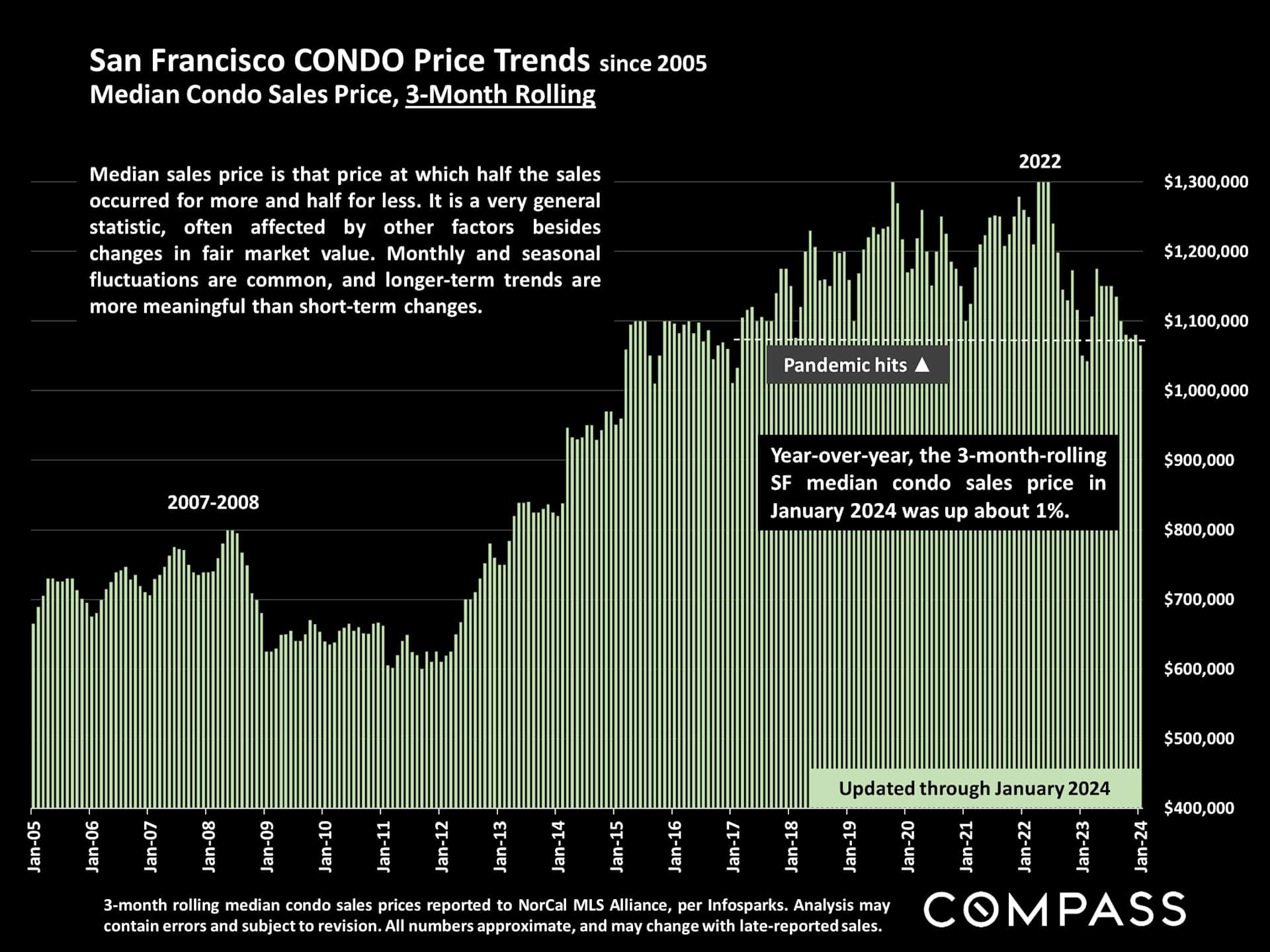

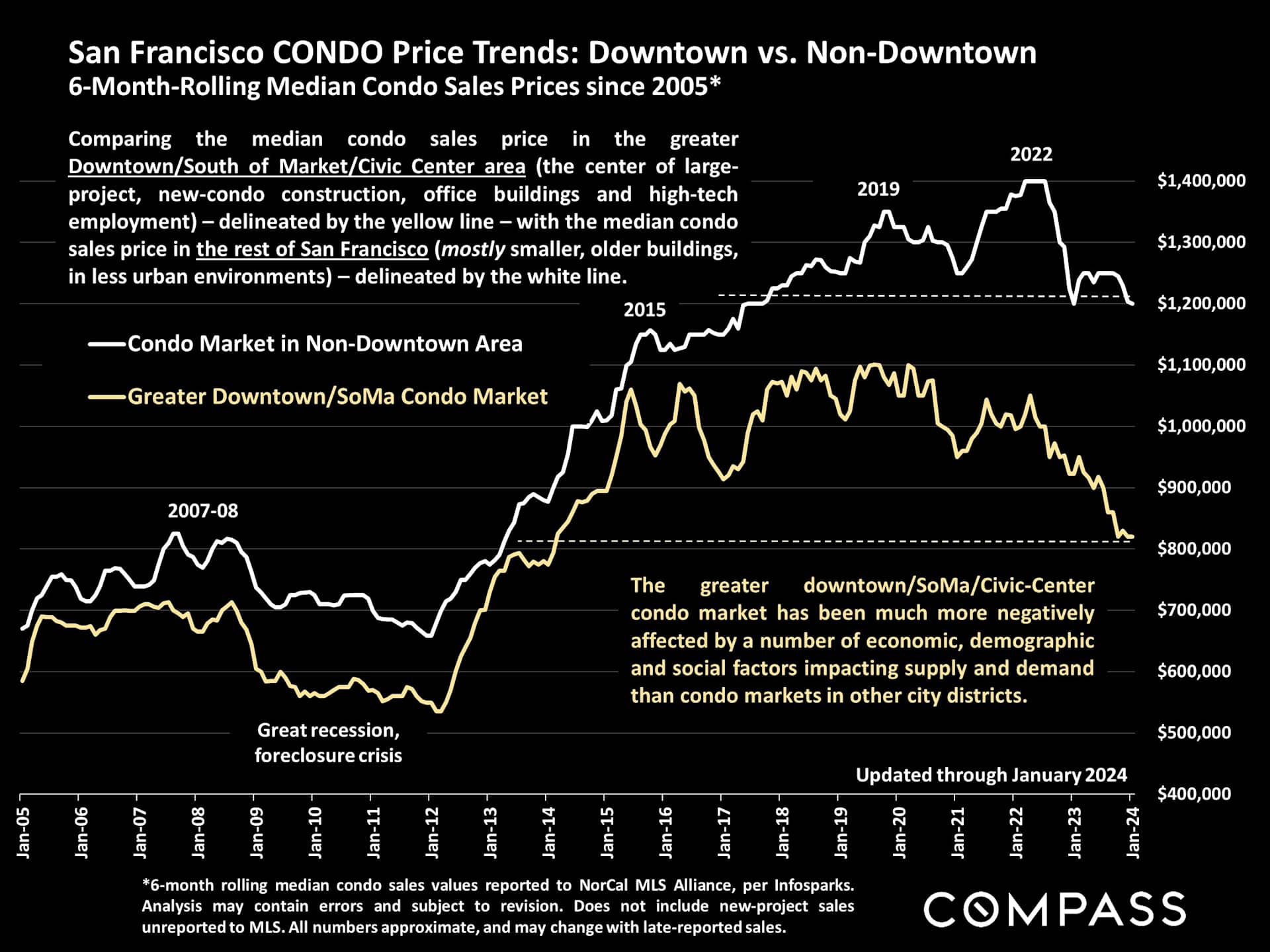

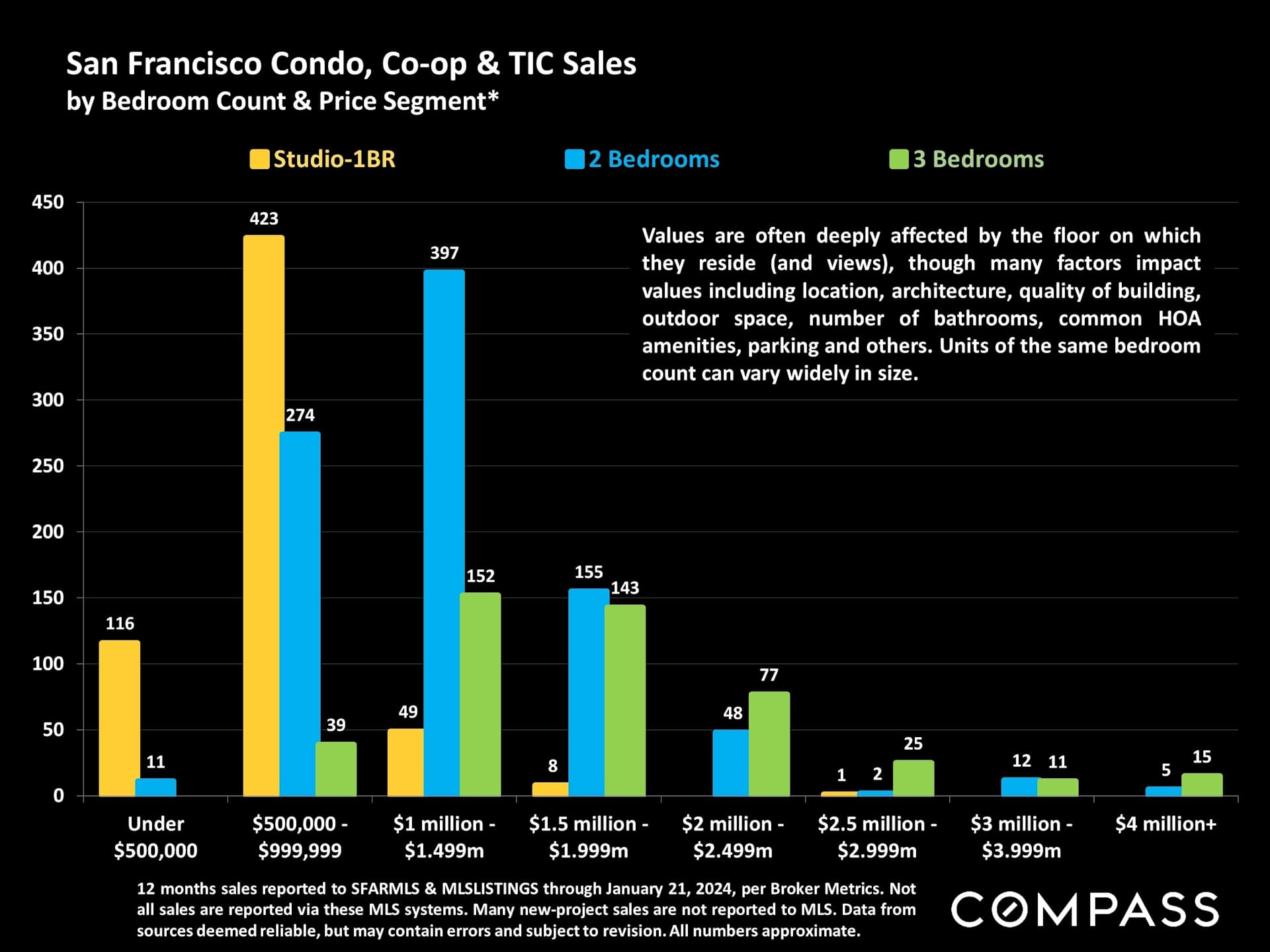

selling. The supply of condo listings is considerably higher, and while condo and house sales

numbers are similar, condo inventory is 130% higher. But condo market conditions also appear to

be heating up in 2024, with market conditions varying significantly between neighborhoods.

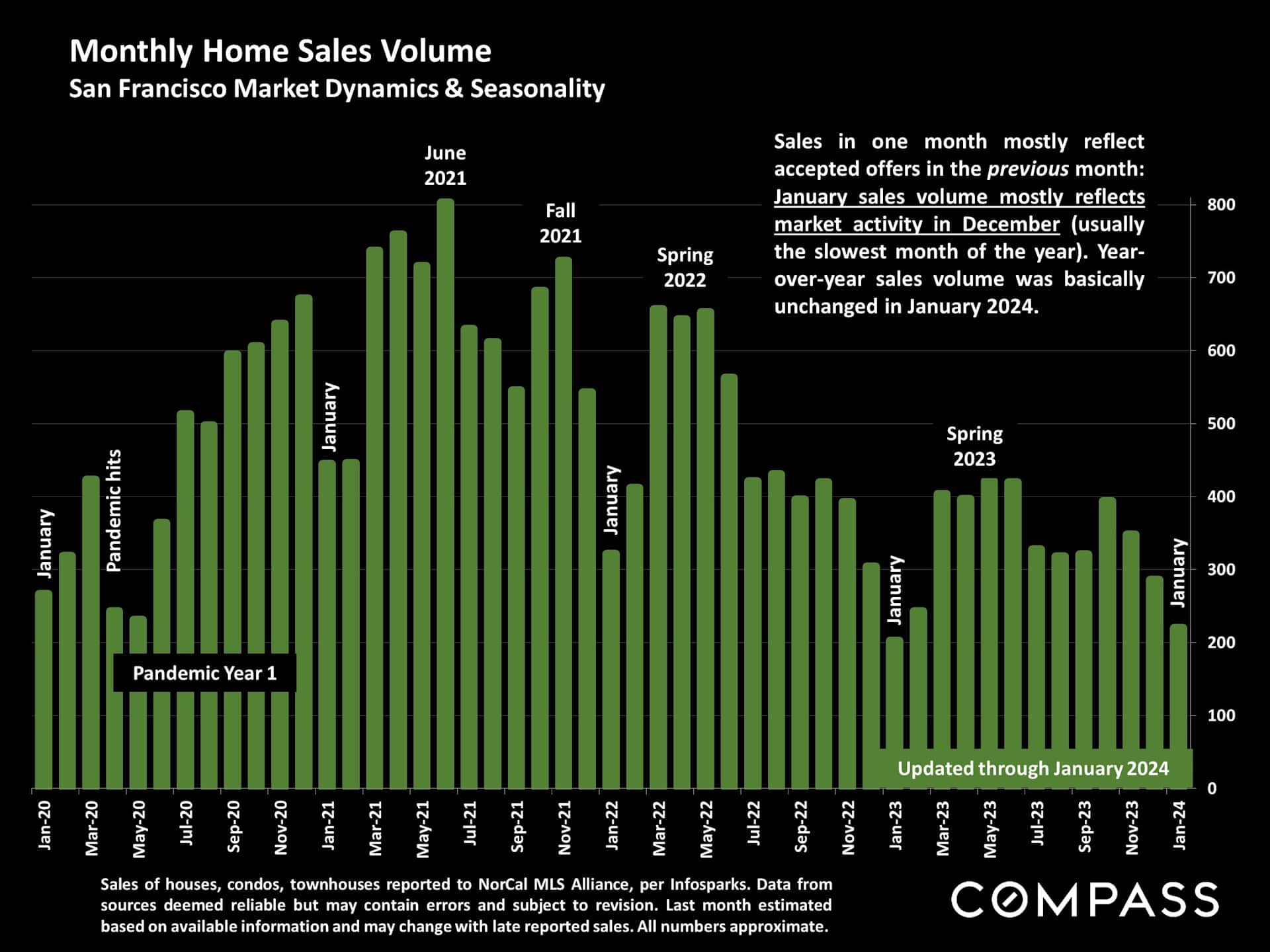

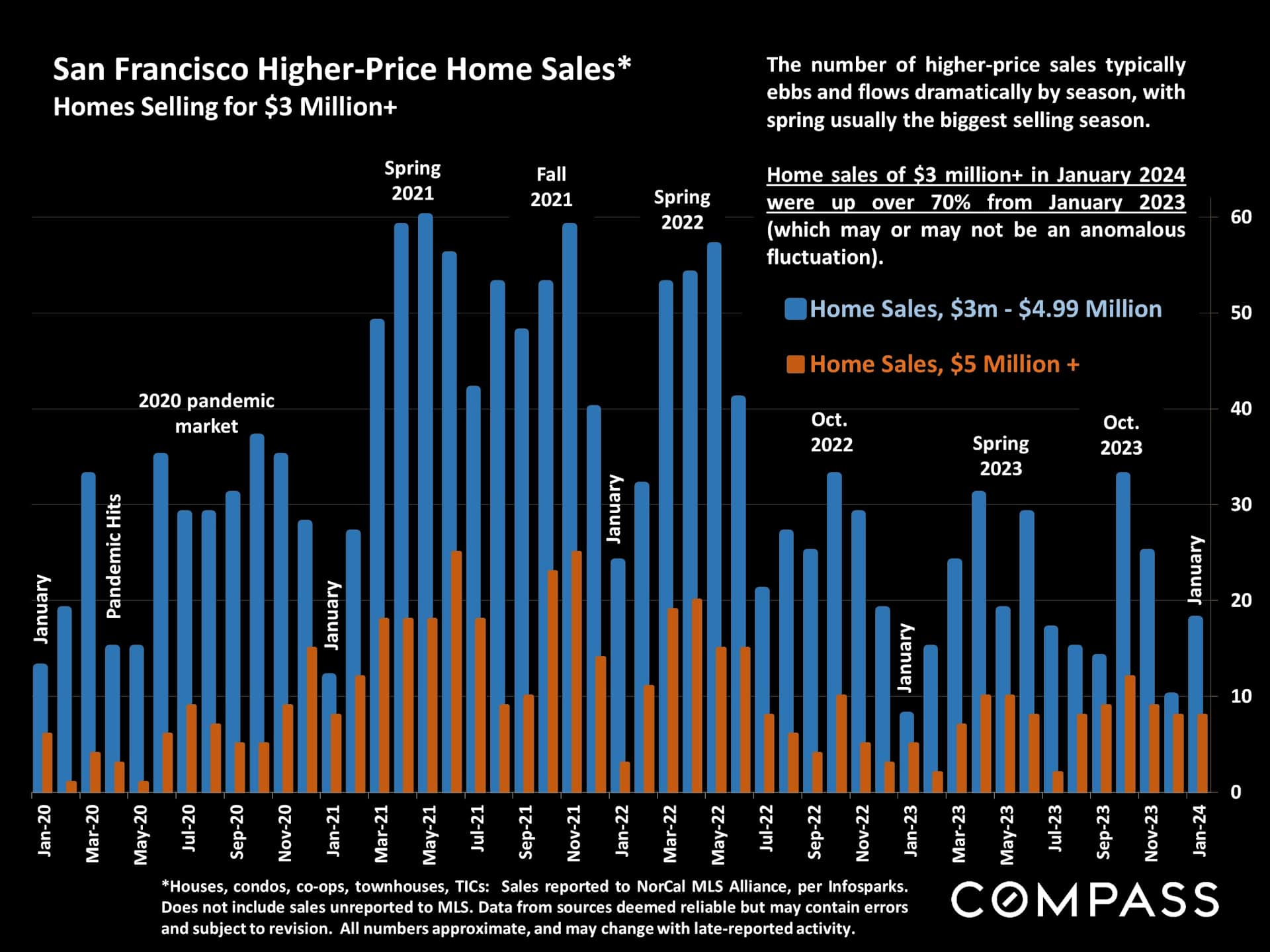

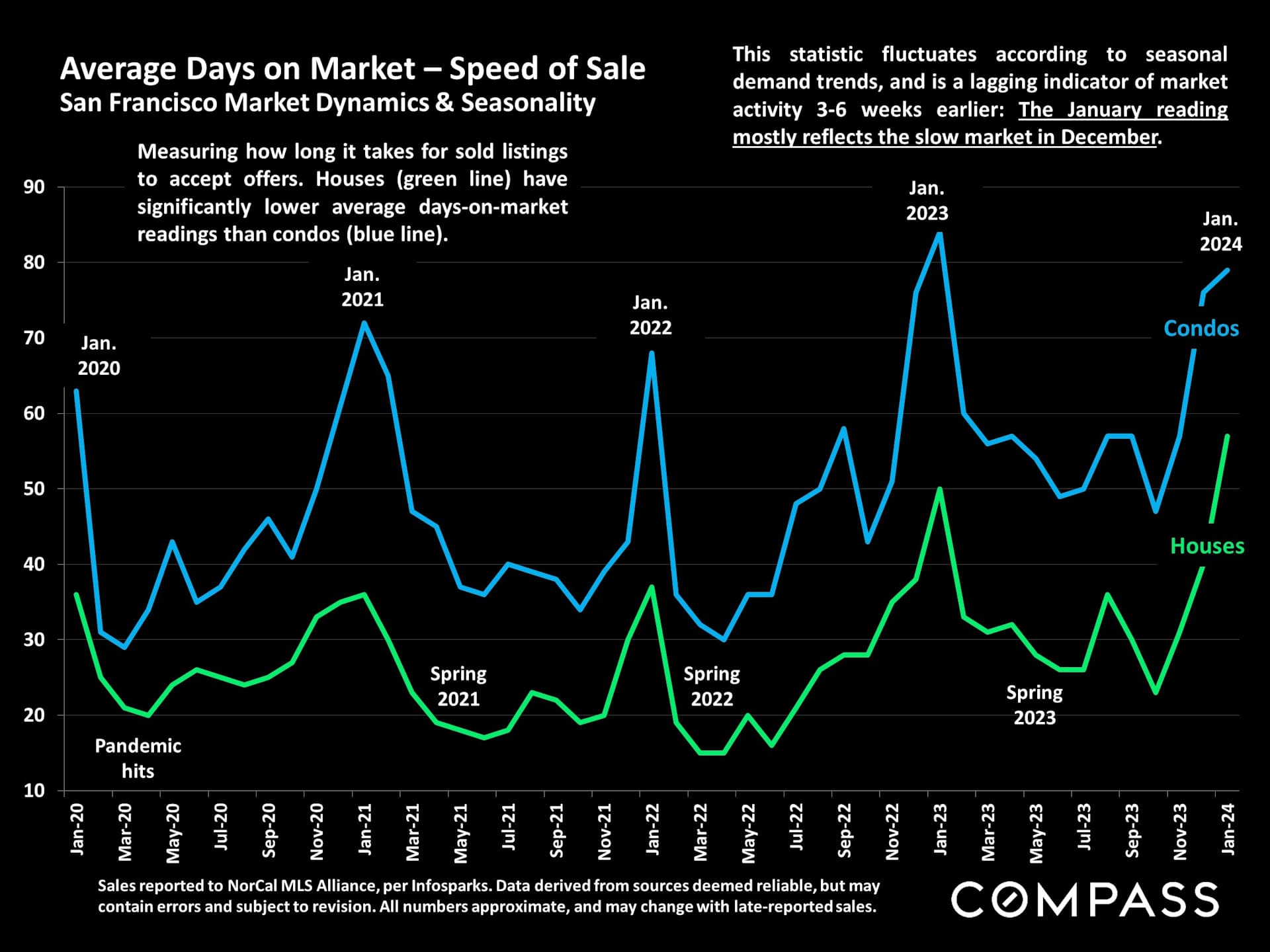

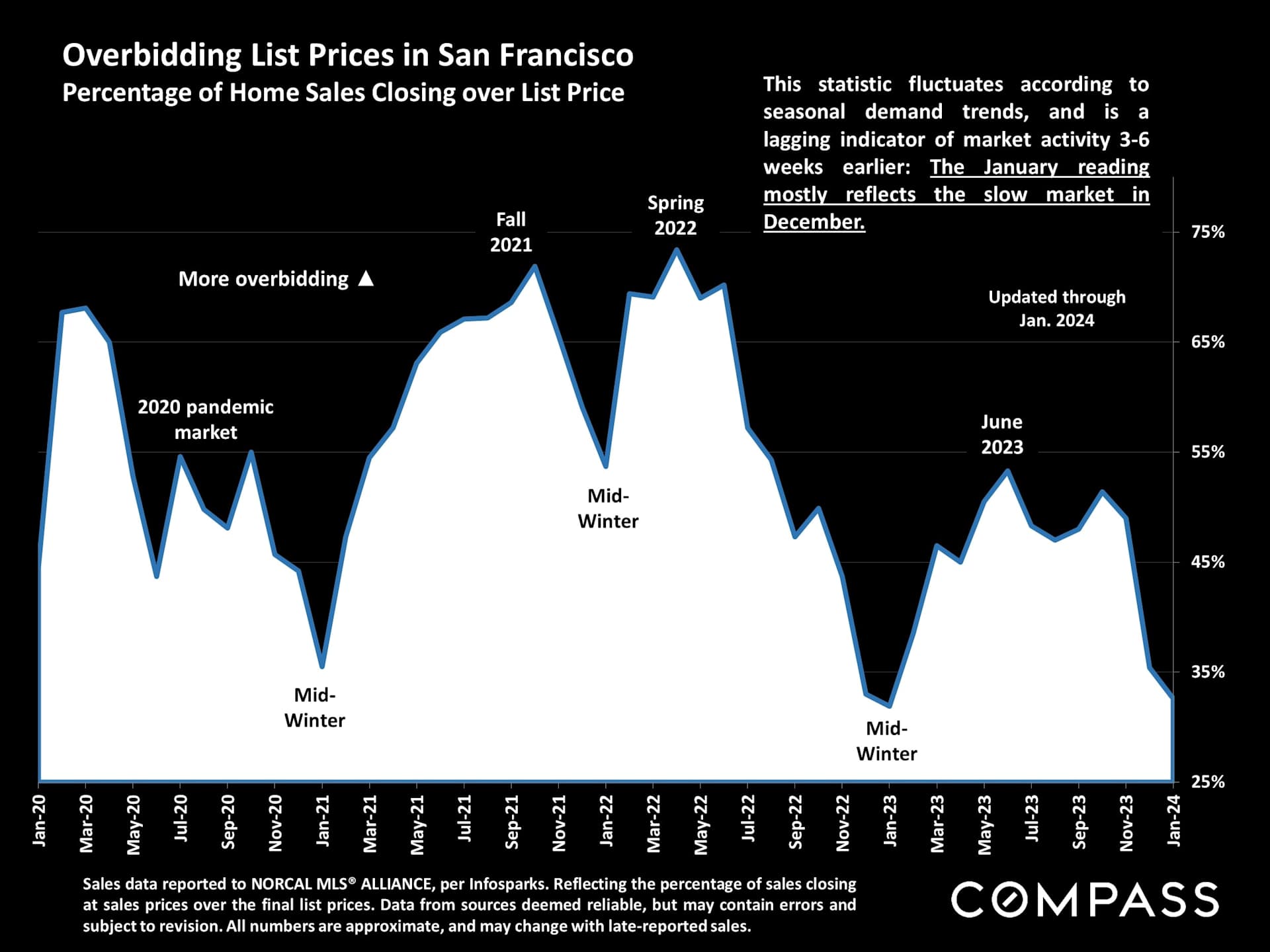

January statistics based on closed sales – sales prices, sales volume, days-on-market, overbidding

percentages – will mostly reflect listings that went into contract in late 2023, the slowest market

of the year. Spring, typically the most active selling season, will probably result in substantial

changes in these indicators. Depending on the weather, “spring” in the Bay Area can begin as

early as February.

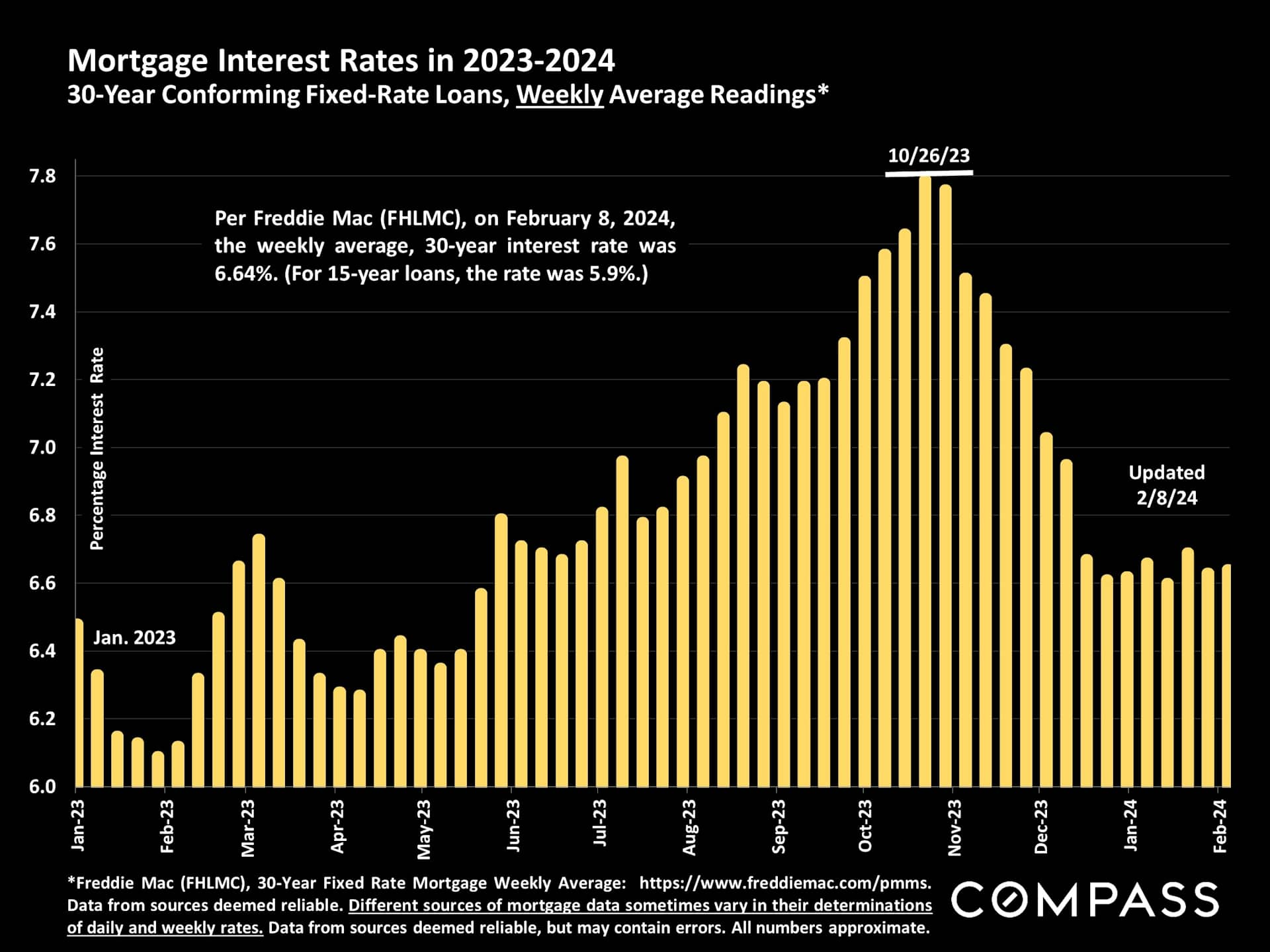

“Although affordability continues to impact homeownership, the combination of a solid economy,

strong demographics and lower mortgage rates are setting the stage for a more robust housing

market. Mortgage rates have been stable for nearly two months, but with continued deceleration

in inflation, rates are expected to decline further. The economy continues to outperform due to

solid job and income growth, while household formation is increasing at rates above pre-pandemic

levels. These favorable factors should provide strong fundamental support to the market in the

months ahead.” FHLMC (Freddie Mac), 2/1/24

“Over the last two months, [consumer] sentiment has climbed a cumulative 29%, the largest two-

month increase since 1991...For the second straight month, all five index components rose... there

was a broad consensus of improved sentiment across age, income, education, and geography.”

University of Michigan, Consumer Sentiment Index, Preliminary January Report, 1/19/24

“The recession America was expecting never showed up...Instead, the economy grew 3.1% last

year, up from less than 1% in 2022, and faster than the average for the 5 years leading up to the

pandemic. Inflation has retreated substantially [and] unemployment remains at historic lows...”

The New York Times, 1/26/24, “Economists Predicted a Recession. So Far They’ve Been Wrong.”

The California Association of Realtors forecasts that compared to 2023, the number of state home

sales in 2024 will increase 23%, the CA median house sales price will rise 6.2%, and the average 30-

year mortgage interest rate will decline to 6.3%. Jordan Levine, CAR chief economist, 1/18/2024

Data from sources deemed reliable but may contain errors and subject to revision. Some January numbers

are estimates based on data available in early February. Economic conditions can be volatile. All numbers

are approximate.

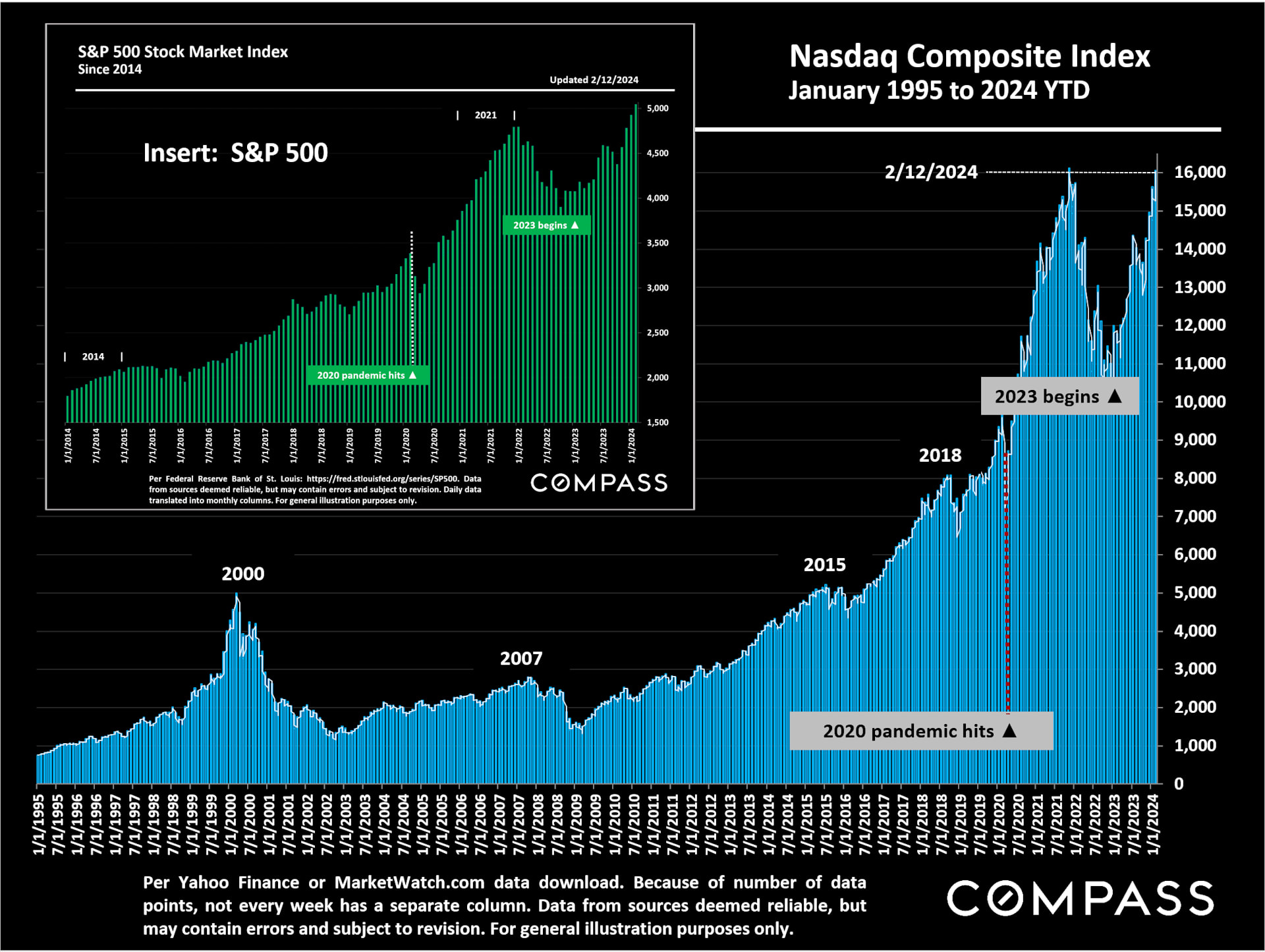

Stock markets continued their staggering rebound through yesterday. The S&P passed 5000 for the first time, but fell back slightly below this morning; the Nasdaq remains within a whisker of its all-time high in 2021.

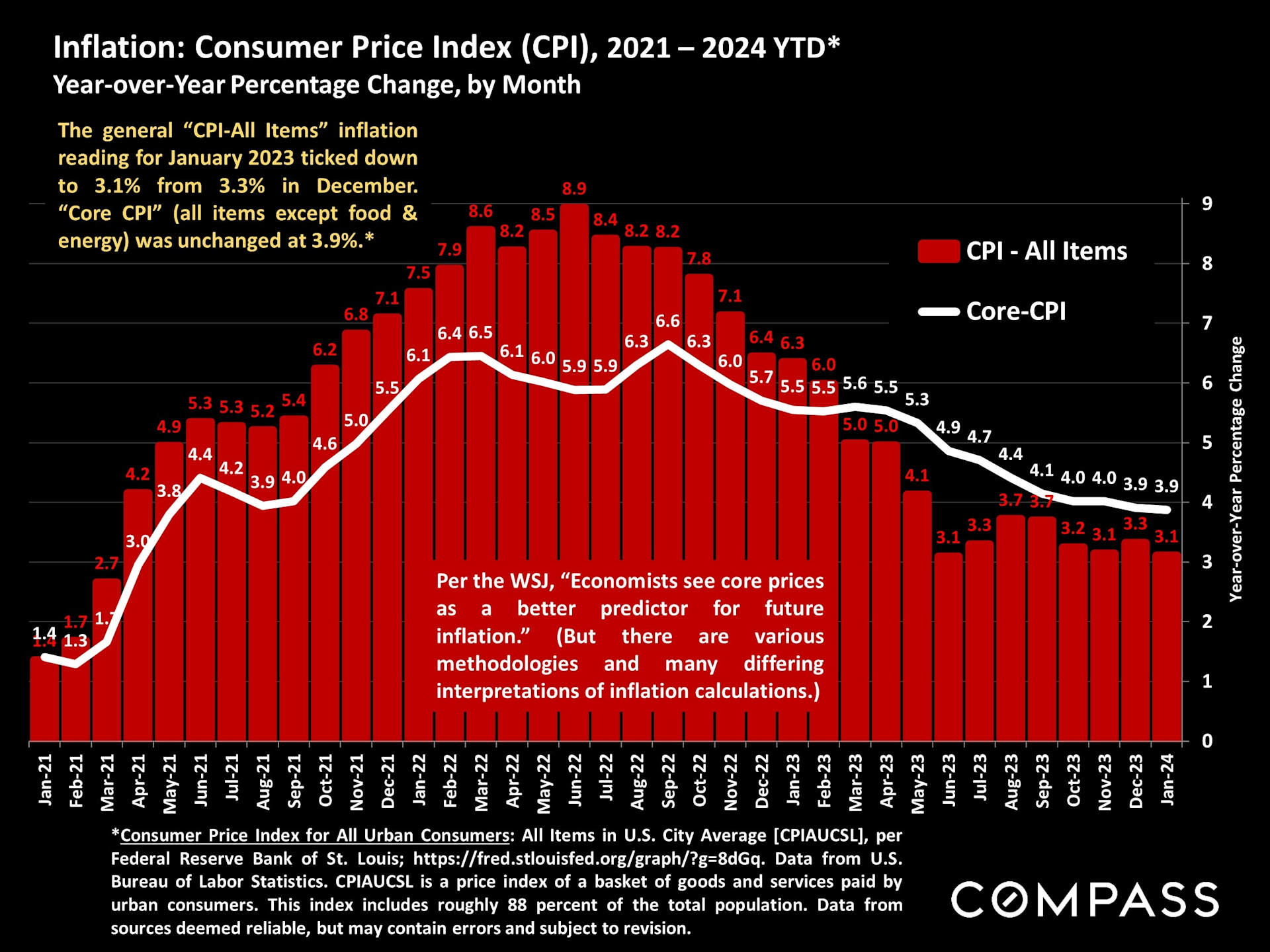

The latest inflation report was just released: Both financial and bond markets were hoping for more significant declines. As of late morning (ET), stock markets were down a little over 1%, and the 10-year Treasury bill yield rate was up. According to the WSJ, the new reading implies that while the Fed had been expected to begin cutting its benchmark rate earlier, now "a June start date is more likely." Of course, guessing what the Fed will do is a very iffy game, to which analysts and economists are addicted.

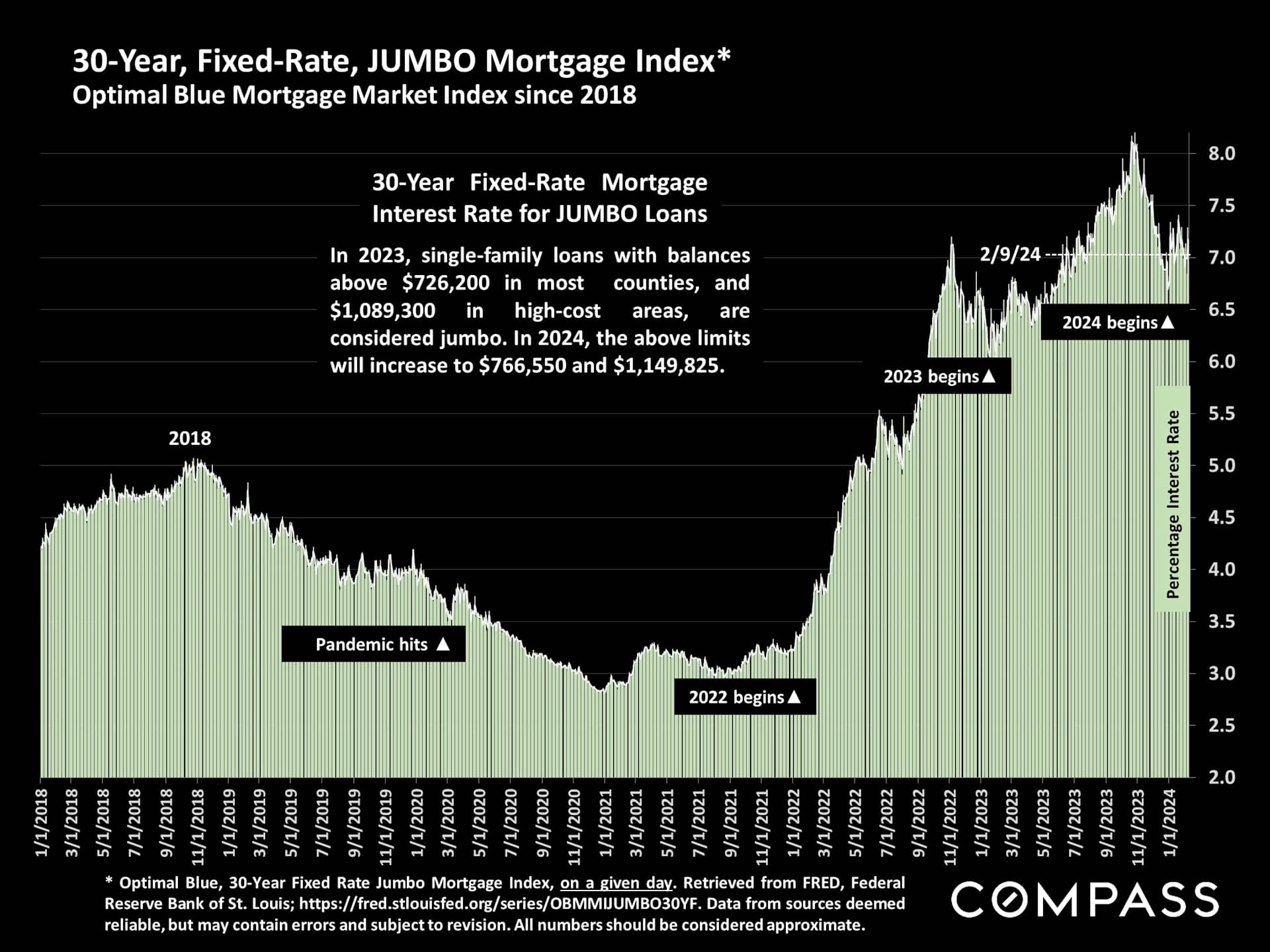

Interest rates, 30-year jumbo Mortgage.

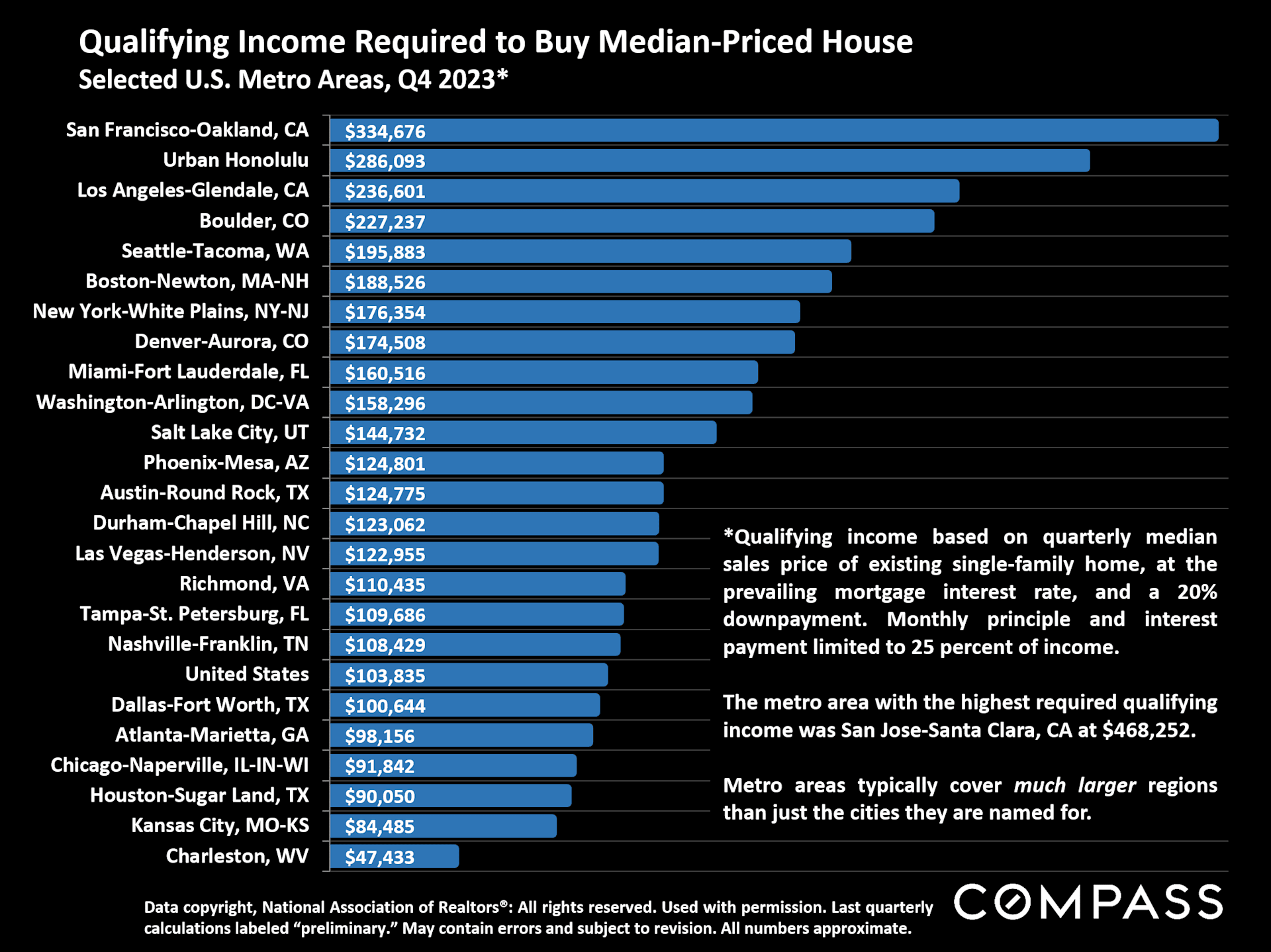

NAR 2023 median house sales prices in selected metro-areas: Metro areas typically cover multi-county and sometimes multi-state regions. The SF metro area includes Marin, Alameda, Contra Costa and San Mateo Counties; The San Jose metro area comprises Santa Clara and San Benito Counties (utterly dominated by the Santa Clara County real estate market).