"Following the release of a stronger-than-expected September jobs report, the 30-year fixed rate mortgage saw the largest one-week increase since April. However, the rise in rates is largely due to shifts in expectations and not the underlying economy, which has been strong for most of the year. Although higher rates make affordability more challenging, it shows the economic strength that should continue to support the recovery of the housing market." FHLMC, 10/10/24

Interest rates have continued to tick up slightly in the past weeks. Weekly and daily averages (from sources that use different methodologies):

Latest inflation report released this morning: General CPI declined again, to the lowest reading since February 2021. "Core" CPI was unchanged at 3.3%. So far today, the response in stock and bond markets has been relatively muted.

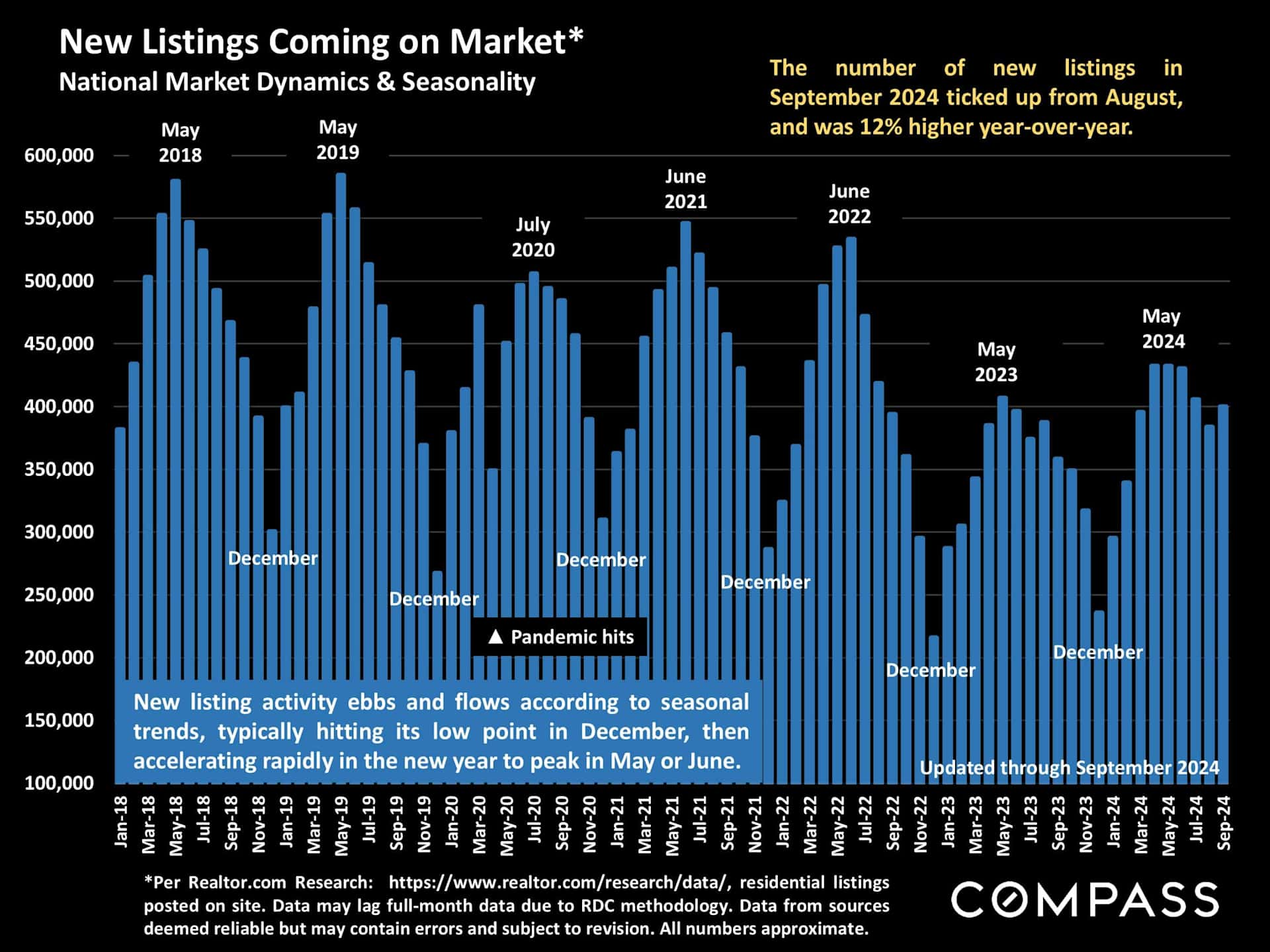

NATIONAL supply and demand indicators: The basic reality since spring is that sales activity has been increasingly outpaced by the increase in active listings for sale, which offers more choice and lessens the competitive environment for buyers. The recent drop in interest rates through very early October - before the latest spike up in rates on 10/4 - did not precipitate the substantial rebound in buyer demand that many had expected in September. It may have been that prior to the jump in rates buyers were holding back in expectation of further declines (as forecast by most analysts). October is typically the last major month of market activity before heading into the big mid-winter holiday slowdown, which usually starts in mid-November and lasts until mid-January.

Generally speaking, the overall national market is seeing similar trends to the general Bay Area market.

The pending-sale ratio - a version of the absorption rate - has been falling as the increase in inventory outpaced sales activity. In September, it was as low as last December, and December typically sees the lowest pending-sale ratio of the year.

Inventory outpacing buyer demand has led to a significant increase in price reductions, comparable to levels seen right after interest rates soared in the first half of 2022.

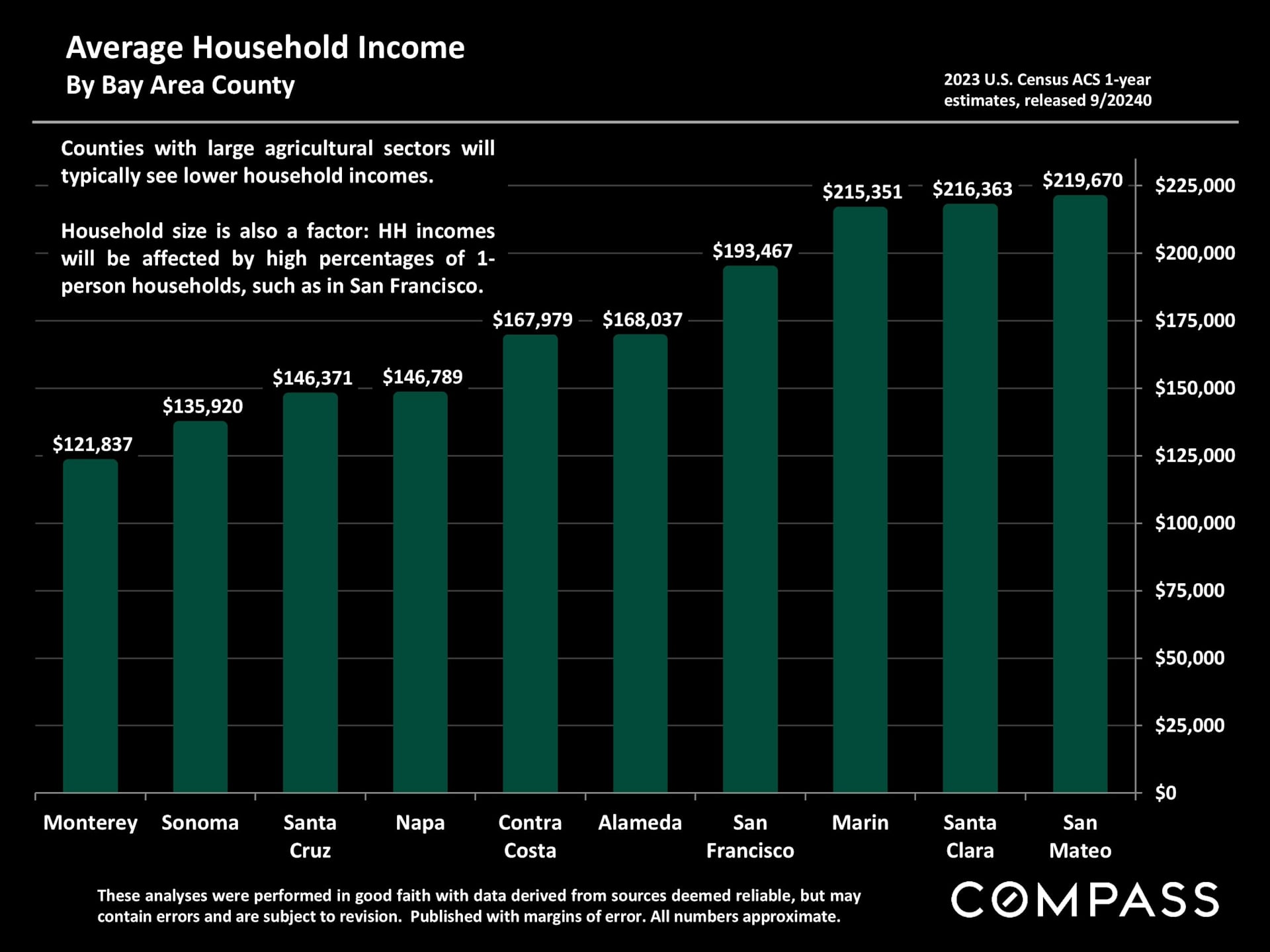

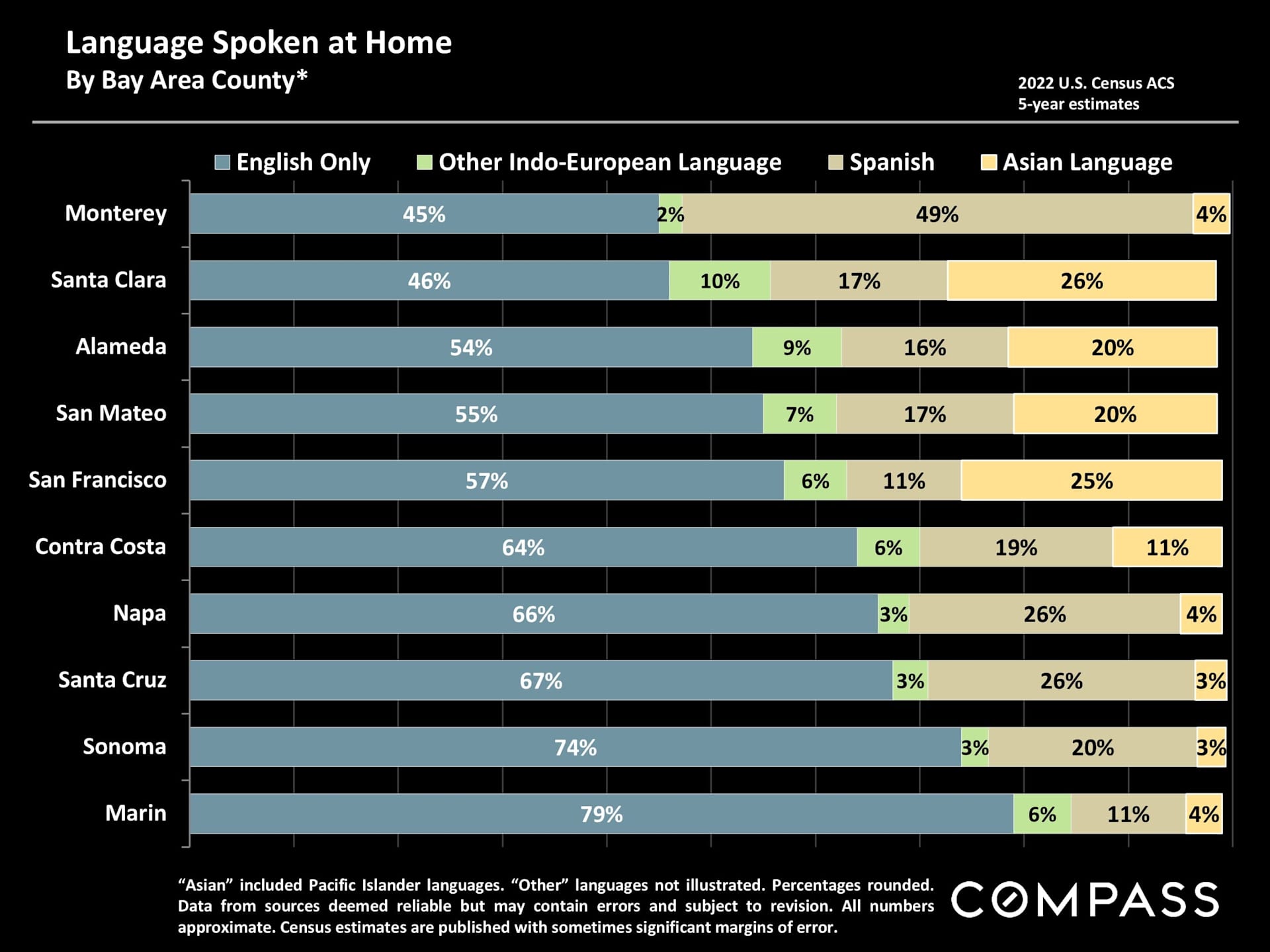

New Census data was recently released, and I created some updated demographic snapshots if you want to post a few or ping your clients with something different.